On Monday, the most significant event will be the release of the ISM manufacturing PMI and ISM manufacturing prices for the U.S.

On Tuesday, the eurozone will publish the core CPI flash estimate y/y and the CPI flash estimate y/y. Additionally, ECB President Lagarde and Fed Chair Powell will participate in a panel discussion titled “Policy Panel” at the ECB Forum on Central Banking in Sintra. The U.S. will also release the JOLTS job openings data.

On Wednesday, the U.S. will publish several key indicators, including the ADP nonfarm employment change, unemployment claims, ISM services PMI, and the FOMC meeting minutes.

Thursday will see the release of CPI data for Switzerland, while in the U.S., markets will be closed in observance of Independence Day.

Finally, on Friday, Canada will publish the employment change and the unemployment rate. In the U.S., the focus will be on the average hourly earnings, nonfarm employment change, and the unemployment rate.

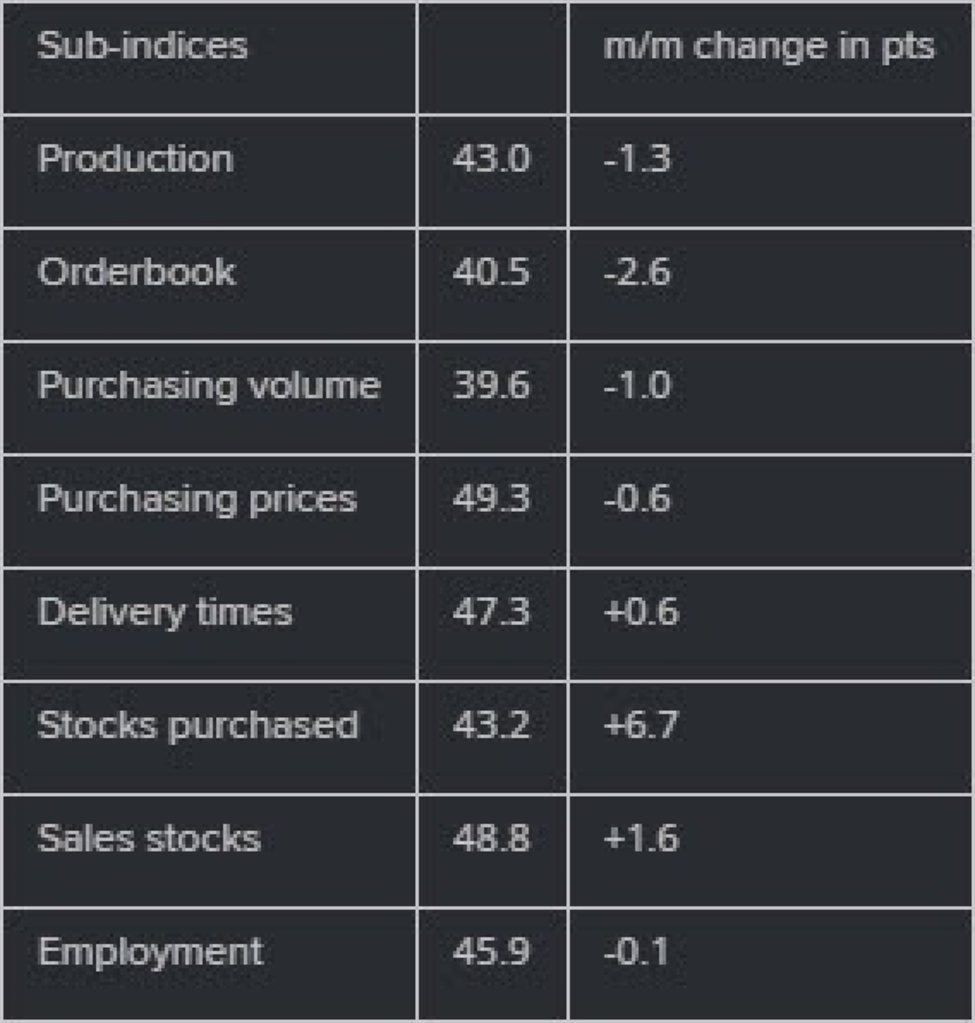

The consensus for the U.S. ISM manufacturing PMI is an increase from 48.7 to 49.2. After rising above 50 in April, the manufacturing index has declined for two consecutive months, and this week’s expectations are for this trend to continue. Wells Fargo analysts believe that potential reasons for this include economic uncertainty, tight credit conditions, and elevated borrowing costs. As long as these conditions persist, the prospects don’t look very promising for the manufacturing sector or for industrial production.

The eurozone flash CPI is likely to cool a bit, although there are some upside risks. Overall, the inflation in countries like France and Spain did not look very promising, as the data was somewhat mixed.

The consensus for the ISM services PMI is a slight decrease from 53.8 to 52.5. The services sector performed better than manufacturing due to sustained high consumer demand for services for many months. However, this does not help with price stability which is what the Fed would like to see.

The Swiss CPI m/m is likely to continue to decline. As a reminder, the SNB cut rates in June and maintains its Q2 2024 inflation forecast for y/y data at 1.4%. However, analysts have stressed that in May, rising prices for housing rentals and petrol put pressure on inflation. If this week’s data prints in line with expectations, it will not have a significant impact on the SNB’s decisions. The Bank predicts Q3 average at 1.5%, so unless this average is significantly exceeded, the Bank might deliver another rate cut at the September meeting.

The BoC will monitor this week’s labor market data to see if there are continued signs of softening. Inflation in Canada rose in May after declining since the beginning of the year so the Bank will look at labor market data for reassurance that the downward trend will continue.

The consensus for the employment change is a drop from 26.7K to 24.5K, with the unemployment rate expected to rise from 6.2% to 6.3%. Continued deterioration in the labor market will help alleviate some of the upward pressure on inflation. The market anticipates that the BoC will deliver another rate cut at its next meeting in July.

In the U.S., the consensus for average hourly earnings m/m is 0.3% vs 0.4% prior. For nonfarm employment change, it is expected to drop from 272K to 189K, while the unemployment rate is likely to remain unchanged at 4.0%.

Despite robust job gains last month, there are signs that the labor market in the U.S. is cooling. This is reflected in the decline of job openings and is also shown in the unemployment rate, which has risen to 4.0%, the highest since 2022.

Wells Fargo analysts note that two-thirds of nonfarm payroll gains over the past year have originated from just three industries: government and healthcare, which are less affected by economic cycles, and leisure and hospitality, which are still recovering from the pandemic. These sectors are expected to continue being major contributors in the short term, but diminishing supportive factors are likely to slow overall job growth in the coming months.

This article was written by Gina Constantin at www.forexlive.com.

Source link