- Major indices close lower on the day/higher for the week

- Crude oil settles at $75.53

- US consumer credit for April rises by $6.40B versus $11.0B increase estimate

- With the Bank of Canada, ECB and jobs in the rear view mirror, the Fed is ahead

- ECB Pres. Lagarde: Still a long way to go until inflation is defeated

- Baker Hughes oil rigs -4 to 492 rigs

- J.P. Morgan changes first Fed rate cut to November from July

- Major European indices close the week little changed

- Atlanta Fed GDPNow growth estimate for Q2 rises to 3.1% versus 2.8% yesterday

- Nick Timiraos from WSJ: What does jobs report mean to Fed? Not much.

- Lael Brainard (NEC director): US jobs report is good news for American workers

- US wholesale inventories for April 0.1% versus 0.2% estimate

- Kickstart the FX trading day for June 7 w/a technical look at the EURUSD, USDJPY & GBPUSD

- US May non-farm payrolls 272K vs +185K expected

- Canada May employment change 26.7k vs 22.5k expected

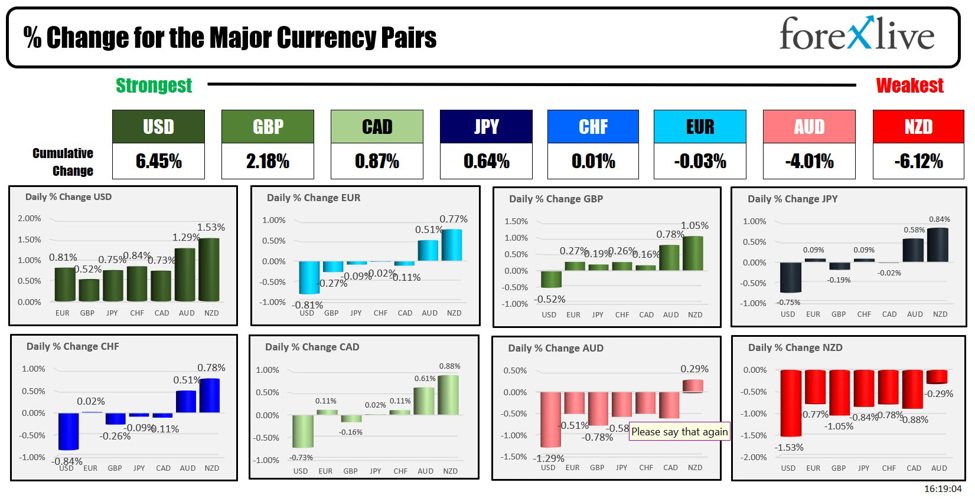

- The JPY is the strongest and the NZD is the weakest as the NA session begins

- ForexLive European FX news wrap: ECB tries to justify rate cut, gold dips on China

- ECB’s Centeno: The message is one of confidence in the disinflation process

- ECB’s Villeroy: We will move at appropriate pace on rate cuts

- ECB’s Holzmann: I was the only one against a rate cut

- ECB’s Schnabel: We cannot pre-commit to a particular rate path

- ECB’s Rehn: Inflation will continue to decline

- ECB’s de Guindos: Inflation is to be around 2% next year

- ECB’s Nagel: The decision to cut rates was not premature

The US jobs report came in stronger, but then again there was some ambiguous/less strong components.

- Non-farm payroll rose 272K vs 185K estimate.

- Private payrolls rose 229K vs 170K estimate

- Average hourly earnings rose 0.4% vs 0.3% expected

- Average earnings YoY rose 4.1% vs 3.9% expected

Those were the stronger-than-expected pieces of the report.

The not so strong parts were:

- Unemployment rate rising to 4.0% from 3.9%.

- The survey of households used to compute the unemployment rate showed that the level of people who reported holding jobs fell by -408,000.

- The household survey also showed that full-time workers declined by -625,000, while those holding part-time positions increased by 286,000.

The household survey is typically more volatile than the establishment survey, which showed the significant payroll gains.

Liz Ann Sonders of Schwab to CNBC said that,

“On the surface, [the report] was hot, but you’ve also got a bigger drop in household employment. For what it’s worth, that tends to be a more accurate signal when you’re at an inflection point in the economy. You can find weakness in the underlying numbers.”Next week, the markets will get the Fed’s take on the report when they announce its interest rate decision on Wednesday. The Fed is expected to keep rates unchanged. The market will be focused on the Fed’s expectations for the end of year rate. At the March meeting, they still saw 3 cuts. That is likely to be lowered to 1-2 (the market about 40 pips of cuts between now and the end of the year).

The markets reaction today saw the USD move higher by 0.52% to 1.53% vs the major currencies. The NZD and the AUD were sold as commodities were sold. China gold purchases were lower last month and the higher dollar and higher yields gave sellers another reason to sell commodities. That tends to weaken the NZD and the AUD whose economies are more commodity-dependent.

- Gold prices today tumbled -$82 or -3.45% to $2293.49. The % decline was the steepest since November 6, 2020.

- Silver prices felt $-2.14 or -6.88% to $29.14 which was its worst % decline since February 2021.

- Copper prices also fell sharply with a -4.82% decline.

The price of Bitcoin reached high of $71949 intraday, but is trading at $69,156 currently. Ethereum is trading at $3684.80 after reaching a high of $3839.70.

Yields moved higher, erasing some of the declines seen this week

- 2 year yield 4.888%, +15.9 basis points. The 2-year yield is near unchanged for the week

- 5-year yield 4.462%, +17.1 basis points. The yield is down -4.6 basis points for the week.

- 10 year yield 4.435%, +15.5 basis points. The yield is down -6.7 basis points for the week.

- 30-year yield 4.554%, was 12.5 basis points. The yield is down -9.6 basis points for the week.

Next week in addition to the FOMC rate decision, the U.S. Treasury will auction off 3, 10, 30-year coupon issues on Monday, Tuesday, and Thursday respectively. It will be tricky with the Fed rate decision between the 10 in 30-year auctions scheduled for Tuesday and Thursday. The Fed decision will be announced on Wednesday.

In the US stock market today, the S&P and NASDAQ indices backed off their record closing levels with modest declines, but still closed higher for the week.

- Dow industrial average fell -0.22% on the day but rose 0.29% for the week.

- S&P index fell -0.11% on the day, but rose 1.32% for the week

- NASDAQ index fell -0.23% on the day, but rose 2.3% for the week

Thank you for your patience and support this week. Adam is hoping to be back in the 1st half of next week. I am hope that all have a happy and safe weekend.

This article was written by Greg Michalowski at www.forexlive.com.

Source link