- Record closes for both the NASDAQ and the S&P indices

- Crude oil futures settle at $74.07

- Putin: If Trump is elected, US could put focus on it’s own interest

- Bitcoin tests topside trendline and the May high

- European stocks rebound. Close higher on the day

- Q&A from Bank of Canada Press conference:Interest rate decisions are one meeting at a time

- US ISM May services PMI 53.8 vs 50.8 expected

- Bank of Canada lowers rates to 4.75% from 5.0%. Full statement from the Bank of Canada

- US May final services PMI 54.8 vs 54.8 prelim

- Kickstart the FX trading day for June 5 w/a technical look at the EURUSD, USDJPY & GBPUSD

- Reuters poll: Federal to cut fed funds rate by 25 basis points in Sept. 74 of 116 polled.

- Canada labor productivity rate for Q1 -0.3% versus -0.2% last quarter

- ADP national employment for May 152K versus 175K estimate

- ForexLive European FX news wrap: Dollar holds steady, ADP and BOC up next

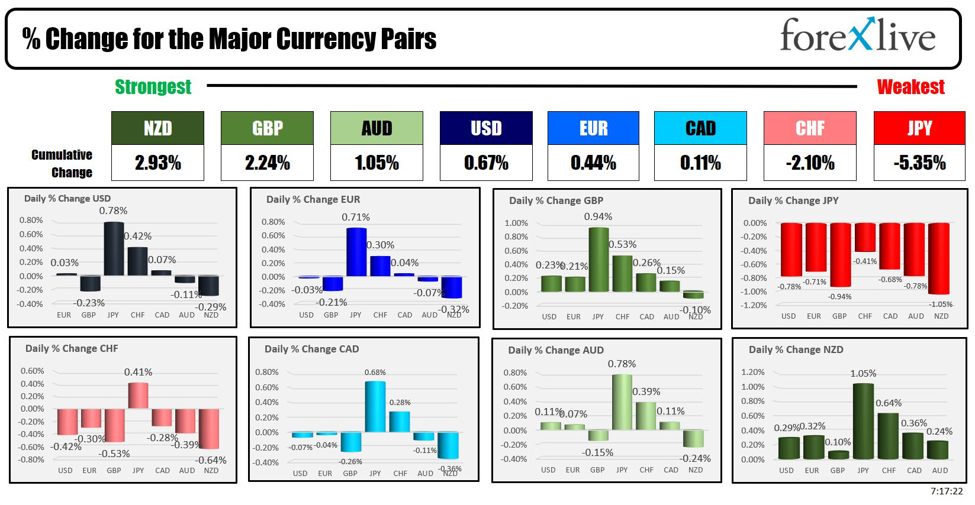

- The NZD is the strongest and the JPY is the weakest as the NA session begins

- US MBA mortgage applications w.e. 31 May -5.2% vs -5.7% prior

- Risk to reward fallacy

The US trading day started with the ADP national employment data for May. It showed a more than expected gain of 152K versus 175K estimate.

Later, the services PMI data in the US came in at 53.8 versus 50.8 expected. However, the employment component remained below 50 at 47.1 (it was up from 45.9 last month – the low for the year). The high for the year was at 50.5 in January. So the level is nearer the low for 2024 vs the high.

With the US jobs data ahead on Friday, weaker employment helped to send yields lower today for the 4th consecutive day. Looking at the 10 year yield, the yield currently is at 4.289%. That is down -4.7 basis points. Five days ago, the yield reached 4.628%. That is down nearly 34 basis points in five trading days.

Looking at the yield curve changes today and over the last week of trading

- 2-year yield 4.726%, -4.4 basis points. That is down from 5.0% or -27.6 basis point

- 5-year yield 4.299%, -5.3 basis points. That is down from 4.656% or -35 basis points

- 10 year yield 4.283%, -5.3 basis points. That is down from 4.628% or -34 basis points.

- 30-year yield 4.433%, -5.1 basis points. That is down from 4.756% or -32 basis points.

While interest rates were moving lower, the stock market was surging to the upside. The broader S&P and NASDAQ indices closed at new record levels (closing near highs for the day). The NASDAQ index led the way with a gain of 1.95%.

Nvidia was the main story with its market capitalization exceeding $3 trillion (3.01T) after a gain of $60 on a day or 5.16% to $1224.40. The company is now the 2nd largest company just ahead of Apple and below Microsoft ($3.15T).

The Dow Industrial Average average lagged on the the day with a modest gain of 0.25%. It still remains below its all-time high level reached last month at 40,003. The final numbers are showing:

- Dow Industrial Average average rose 96.04 points or 0.25% at 38807.34.

- S&P index rose 62.69 points or 1.18% at 5354.04.

- NASDAQ index rose 330.86 points or 1.96% at 17187.90

The small-cap Russell 2000 rose 29.92 points or 1.47% at 2063.67. The Russell 2000 declined over the last two trading days despite lower yields as concerns about growth was the focus. Not today though.

In the forex, the NZD is ending the day as the strongest of the major currencies. The JPY – a day after being the strongest of the major currencies – is the weakest of the majors as the declines from yesterday were fully retraced.

The USD is ending the day mixed.

The CAD is also mixed despite the Bank of Canada cutting rates by 25 basis points – joining the SNB as the 2nd major central bank to cut rates. The ECB is expected to join that club tomorrow when they announce its interest rate decision at 8:15 AM ET. Expectations are for a 25 basis point cut in the main refinancing rate to 4.25% from 4.5%. ECB Lagarde will conduct the press conference starting at 8:45 AM.

Bank of Canada Governor Tiff Macklem emphasized that interest rate decisions will be made on a meeting-by-meeting basis, depending on economic data. If the economy and inflation continue to align with expectations, more rate cuts are likely. While progress has been made in combating inflation, aiming to bring it back to the 2% target, the work is not yet done.

The timing of further cuts will depend on incoming data, acknowledging potential risks and bumps along the way. Despite some limits on diverging from U.S. policy, the BoC forecasts gradual inflation reduction toward the target.

Population growth, which has eased employment pressures but increased housing demand, is expected to slow. The economy appears to be heading for a soft landing, with room for growth beyond potential for a period. Although the BoC is normalizing its balance sheet, the policy remains restrictive as inflation is still above target. Interest rates are not expected to return to pre-pandemic lows, and historically, there have been significant divergences with the Federal Reserve.

In other markets:

- Crude oil rose $0.85 or 1.16% at $74.10

- Gold rose $27.64 or 1.18% at $2353.10.

- Silver rose 47.7 cents or 1.62% at $29.96.

- Bitcoin trades at $71,319 after reaching an intraday high of $71,759.

This article was written by Greg Michalowski at www.forexlive.com.

Source link