UPCOMING EVENTS:

- Monday: BoJ

Summary of Opinions, German IFO. - Tuesday:

Canada CPI, US Consumer Confidence. - Wednesday:

Australia Monthly CPI. - Thursday: Japan

Retail Sales, US Durable Goods Orders, US Final Q1 GDP, US Jobless Claims. - Friday: Tokyo

CPI, UK Final Q1 GDP, Canada GDP, US PCE, University of Michigan Consumer

Sentiment (final).

Tuesday

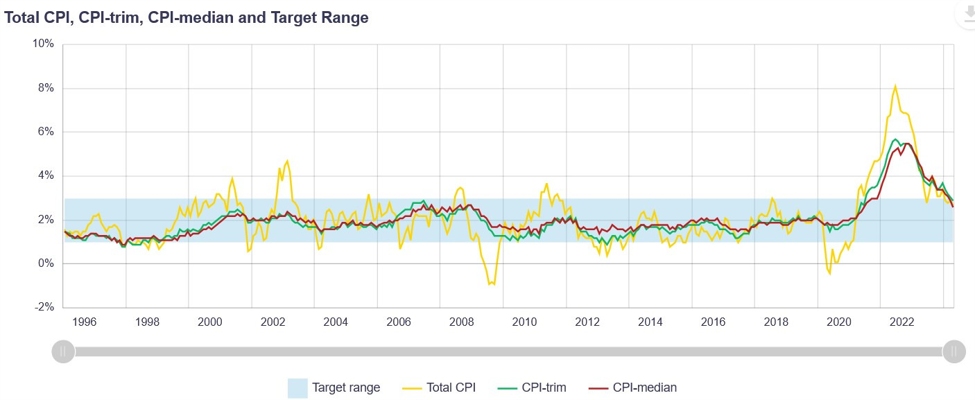

The Canadian CPI Y/Y is expected at 2.6%

vs. 2.7% prior, while the M/M measure is seen at 0.3% vs. 0.5% prior. The

Trimmed Mean CPI Y/Y is expected at 2.8% vs. 2.9% prior, while the Median CPI

Y/Y is seen at 2.6% vs. 2.6% prior.

The last

report showed the underlying inflation

measures falling back inside the BoC’s 1-3% target band which gave the central

bank the green light to deliver the first

rate cut. The market sees a 67% chance of

another rate cut in July but that will depend on the CPI data this week.

The US Consumer Confidence is expected at

100 vs. 102 prior. The last

report showed confidence improving after

three consecutive months of decline. The Chief Economists at The Conference

Board highlighted that “the strong labour market continued to bolster

consumers’ overall assessment of the present situation”.

Moreover, “looking ahead, fewer consumers

expected deterioration in future business conditions, job availability, and

income”. The overall confidence gauge remained within the relatively narrow

range it has been hovering in for more than two years. The Present

Situation Index will be something to watch given the recent misses in the US

Jobless Claims as that’s generally a leading indicator

for the unemployment rate.

Wednesday

The Australian Monthly CPI Y/Y is expected

at 3.8% vs. 3.6% prior. As a reminder, the last

report surprised to the upside with the

underlying inflation measures remaining sticky at higher levels. The RBA kept a

hawkish stance at the latest

policy meeting as it reiterated that

“inflation remains above target and is proving persistent” and added that

“inflation is easing but has been doing so more slowly than previously

expected”.

For this reason, the central bank kept all

options on the table by “not ruling anything in or out”. Some better inflation

data won’t change much for the market, but another disappointment could add some slight chances of a rate hike. The RBA is expected to remain on hold until

mid-2025.

Thursday

The US Jobless Claims

continue to be one of the most important releases to follow every week as it’s

a timelier indicator on the state of the labour market. Initial Claims keep on

hovering around cycle lows, while Continuing Claims remain firm around the

1800K level.

This has led to a weaker

and weaker market reaction as participants become used to these numbers.

Nonetheless, in the last two weeks we started to see the data missing

expectations although it remains below the cycle highs. This is something

to keep an eye on.

This week Initial Claims

are expected at 236K vs. 238K prior, while Continuing Claims are seen at 1820K vs.

1828K prior.

Friday

The Tokyo Core CPI Y/Y is

expected at 2.0% vs. 1.9% prior. Inflation in Japan is basically at target and

there are no strong signals that point to a reacceleration. It’s hard to see a

rate hike given that Japan strived to achieve inflation for decades and it

might ruin this accomplishment by tightening policy. The data shouldn’t change

anything for the BoJ which is expected to trim bond purchases by a

“substantial” amount at the next policy meeting.

The US Headline PCE Y/Y is

expected at 2.6% vs. 2.7% prior, while the M/M measure is seen at 0.0% vs. 0.3%

prior. The Core PCE Y/Y is expected at 2.6% vs. 2.8% prior, while the M/M

reading is seen at 0.1% vs. 0.2% prior. Forecasters can reliably estimate the

PCE once the CPI and PPI are out, so the market already knows what to expect. This report won’t change anything for the Fed as the central bank remains in a “wait and

see” mode until September at very least.

This article was written by Giuseppe Dellamotta at www.forexlive.com.

Source link