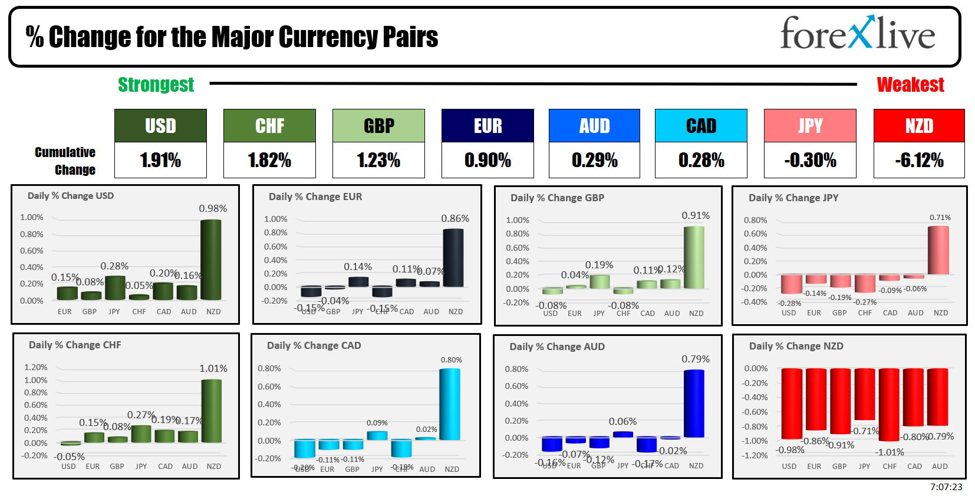

As the North American session is started the USD is the strongest of the major currencies and the NZD is the weakest. Overnight the Reserve Bank of New Zealand (RBNZ) cut its cash rate by 50 basis points, reducing it from 5.25% to 4.75% in a widely expected move.

The decision reflects the current state of excess capacity in New Zealand’s economy, which has helped curb inflationary pressures. The RBNZ cited low import prices and weakening business investment and consumer spending as contributing factors to disinflation.

They said that geopolitical tensions continue to pose challenges to global economic activity and that New Zealand’s inflation is now within the 1-3% target range.

The RBNZ committee agreed that the 50-basis-point cut aligns with their mandate to maintain low and stable inflation. They also noted that labor market conditions are softening, high-frequency indicators point to subdued growth, and financial conditions remain restrictive with low credit demand. Finally, they said that future rate adjustments will depend on the evolving economic environment.

Technically, after breaking below a cluster of technical levels including the 100-day MA at 0.61718, the 50% midpoint of the range since the August low at 0.6113, and the 200-day MA at 0.60966, the price did bounce back into that cluster but found willing sellers against the midpoint level. The price has since moved back below the 200 day MA at 0.60966 and that keeps the sellers in firm control.

Looking ahead as the clock ticks toward the ECB rate decision next week (October 17), ECBs Villeroy spoke and said:

- ECB “very likely” to cut interest rates next week

- Suggested further rate cuts may follow, depending on inflation progress.

- Cited weak economic growth as a key factor for the likely cut.

ECBs Patsalides weighed in and said:

- There seems to be room for a rate cut.

- Data should be discussed as usual

- Middle east implications should be assessed

Finally, Kazimir came in with some dissent warnings saying:

- He is not worried about undershooting the 2% goal, but

- Not as convinced as media reports on an October cut (you are saying there is a chance?)

The ECB has already cut interest rates twice this year from record highs. Markets anticipate further rate cuts in October and December as inflation eases faster than expected.After returing from the Golden Week holiday, the stocks in China remain unstable. Stocks fell sharply, halting the recent rally, as investors grew disappointed over the lack of significant new stimulus measures.Investors had hoped for more concrete details on Beijing’s fiscal stimulus plans, but the lack of new measures dampened market enthusiasm.

Both the Shanghai Composite and the CSI300 indexes saw their largest single-day losses since February 2020, falling 6.6% and 7.1%, respectively.

However, some analysts still feel that expectations remain high for a major fiscal stimulus announcement later this month.

The other worry is the potential response from Isreal to the Iran missile attach last week. Israel’s Netanyhu met for over 5-hours with a group of senior ministers and other officials in an attempt to come to a decision on the Israel response against Iran. Time will tell, but Isreal did cancel the trip to Washington of their Defense Minister Gallant which keeps the door open for a response at any time.

The western coast of Florida (and the whole state) is preparing for Hurricane Milton. Milton weakened slightly Wednesday morning over the Gulf of Mexico and now has winds of 155 mph, according to the National Hurricane Center but that is only 2 MPH below a Cat 5 storm. Milton will continue to lose some strength today but will remain a strong and damaging storm when it makes landfall in Florida overnight tonight.

The US weekly mortgage applications found -5.1% after a decline of -1.3% last week. The 30-year mortgage rate rose to 6.36% from 6.14%.

US wholesale image twice will be released at 10 AM with expectations up 0.2%..

Fedspeak today includes:

- Atlanta Fed Pres. Bostick at 8 AM

- Dallas Fed Pres. Logan at 9:15 AM

- Congo Fed Pres. Goolsby at 10:30 AM

- Richmond Fed Pres. Barkin at 12:15 PM

The Federal Reserve meeting minutes from the last meeting were the Fed cut rates by 50 basis points will be released at 2 PM ET

Looking ahead to tomorrow, US CPI data will be released at 8:30 AM with expectations for a headline rise of +0.1% and core reading of +0.2%. PPI data will be released on Friday along with the monthly Canada employment data.

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down down -$0.39 or -0.54% at $73.17. At this time yesterday, the price was at $75.40

- Gold is trading down -$2.00 or -0.09% at $2618.20. At this time yesterday, the price was $2649.79

- Silver is trading up $0.05 or 0.18% at $30.66 . At this time yesterday, the price is at $31.33

- Bitcoin is trading lower than this time yesterday at $62,145. At this time yesterday, the price was at $62,583

- Ethereum is trading marginally higher than this time yesterday at $2438.70. At this time yesterday, the price was at $2437.00

In the premarket, the snapshot of the major indices trading higher after yesterday’s declines.

- Dow Industrial Average futures are implying loss of -13.67 points. Yesterday, the index rose 126.13 points or 0.20% at 42,080.37

- S&P futures are implying a decline of -0.88 points. Yesterday, the index rose 58.19 points or 0.97% at 5,751.13

- Nasdaq futures are implying a decline of -24.08 points. Yesterday, the index rose 259.01 or 1.45% at 18,182.92

Yesterday, the small-cap Russell 2000 rose 1.89 points or 0.09% at 2,194.98

European stock indices are trading mixed:

- German DAX, +0.29%

- France CAC, +0.22%

- UK FTSE 100, +0.29%

- Spain’s Ibex, -0.17%

- Italy’s FTSE MIB, unchanged (delayed by 10 minutes)

Shares in Asian Pacific session China shares fell. Japan’s shares rose

- Japan’s Nikkei 225, +0.87%

- China’s Shanghai Composite Index, -6.62%

- Hong Kong’s Hang Seng index, -1.38%

- Australia S&P/ASX index, +0.13%

Looking at the US debt market, yields are higher in the yield curve is little changed

- 2-year yield 3.965%, -1.2 basis points. At this time yesterday, the yield was at 3.972%

- 5-year yield 3.863%, -0.1 basis points. At this time yesterday, the yield was at 3.865%

- 10-year yield 4.037%, +0.2 basis points. At this time yesterday, the yield was at 4.035%

- 30-year yield 4.322%, -0.2 basis points. At this time yesterday, the yield was at 4.321%

Looking at the treasury yield curve it is steeper:

- The 2-10 year spread is at +7.2 basis points. At this time yesterday, the yield spread was +5.8 basis points.

- The 2-30 year spread is at +35.7 basis points. At this time yesterday, the yield spread was +34.5 basis points.

In the European debt market, the 10 year yields are down modestly

This article was written by Greg Michalowski at www.forexlive.com.

Source link