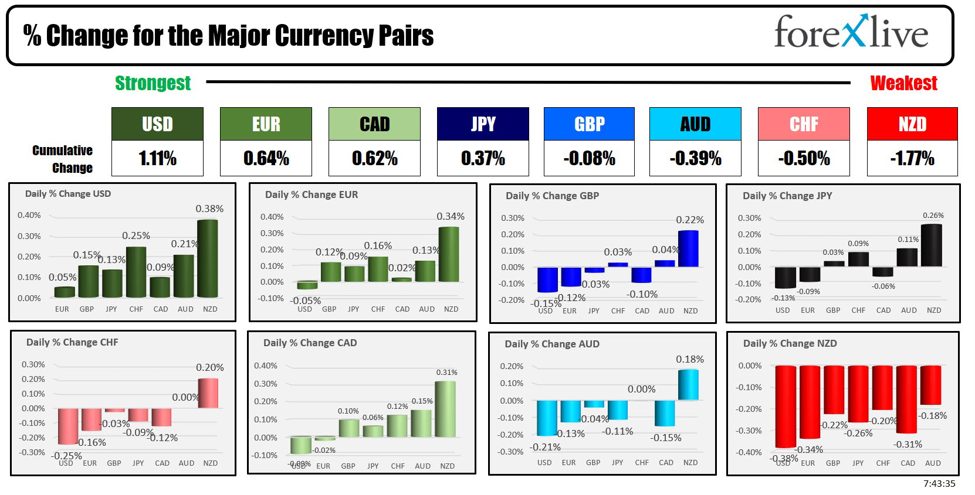

As the North American session begins, the USD is the strongest and the NZD is the weakest.

UK retail sales was weaker overnight (-1.2% versus -0.6% estimate)

The big news is the global downage as a result of a software update at Crowdstrike that then impacted Microsoft (and others) grounded airlines and impacted many businesses globally. The fix has been found, fixed and although there are still some outages, the fix has been deployed. The report is this is not a cyber attack but due to a software update. If you are traveling, expect delays.

ECB comments today a day after the ECB kept rates unchanged and Lagarde kept to the script that rate decisions are data dependent showed:

ECB’s Šimkus:

Gediminas Šimkus agrees with market expectations of two more rate cuts this year. He predicts that interest rates will continue to decrease significantly.

ECB’s Muller:

Madis Muller emphasizes the importance of not pre-committing to decisions for September. He acknowledges market expectations for at least one more rate cut but refrains from commenting personally. Muller notes ongoing fluctuations in inflation and observes that wage growth is not aligning with the 2% target. He projects inflation to decelerate over the next 12 months and expects the Eurozone economy to recover in the coming quarters, despite a slightly deteriorated outlook.

ECB’s Villeroy:

The Bank of France Governor finds market expectations on rates to be reasonable. He confirms that disinflation is occurring as anticipated but predicts a slower decline in inflation. Villeroy monitors services inflation closely and stresses that rate decisions will be data-dependent. He highlights increased uncertainty in economic growth compared to a few months ago.

In Japan, the private sector economic council members expressed concerns about the negative effects of a weak yen, emphasizing that these impacts on households’ purchasing power cannot be overlooked. The Japanese government has downgraded its growth forecast for the current fiscal year ending in March 2025 to a 0.9% expansion, down from the 1.3% gain projected in January. However, the economy is expected to grow by 1.2% in fiscal 2025, with growth projected to accelerate due to robust capital expenditure and consumption. Despite this, consumption has been negatively affected by rising import costs due to the weak yen. The government retains its view that the economy will sustain a domestic demand-led recovery, but some members of the top economic council have voiced concerns about the recent weakness in consumption and the pain inflicted by the yen’s fall on households. They stressed that the government and the Bank of Japan must guide policy with close attention to recent yen declines.

Meanwhile, Japanese Prime Minister Kishida emphasized the need for caution regarding the impact of rising prices driven by a weak yen. He highlighted that the government must remain vigilant about these effects on the economy to achieve a domestic-demand driven recovery.

According to a Reuters poll of economists, only 24% expect the Bank of Japan (BOJ) to implement a rate hike in July, with 76% predicting no change. Instead, 30% foresee a rate hike in September, and 43% anticipate it in October. Additionally, 59% of economists expect the BOJ to taper monthly bond purchases to around ¥5 trillion initially, with 52% predicting a further reduction to about ¥3 trillion by July 2026.

Some earnings released today included AMEX, Travelers and Halliburton.

-

American Express Co (AXP) Q2 2024 (USD):Shares are trading down -1.75%

- EPS: $3.49 (expected: $3.29)

- Revenue: $15.06bn (expected: $15.59bn)

- EPS BEAT, Revenue MISS

- FY EPS view: $13.30-13.80 (expected: $12.65-13.15)

-

Travelers Companies Inc (TRV) Q2 2024 (USD):

- Core EPS: $2.51 (expected: $2.11)

- Revenue: $12.128bn (expected: $11.34bn)

- EPS BEAT, Revenue BEAT

- Very confident in outlook for the business

-

Halliburton Co (HAL) Q2 2024 (USD):

- EPS: $0.80 (expected: $0.80)

- Revenue: $8.53bn (expected: $8.96bn)

- EPS MET, Revenue MISS

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down $0.27 or -0.33% at $81.03. At this time yesterday, the price was at $81.18

- Gold is trading down $36.50 or -1.5% at $2408.47 at this time yesterday, the price was trading at $2466.07.

- Silver is trading down $0.75 or -2.51% at $29.07. At this time yesterday, the price is trading at $30.39

- Bitcoin trading at $64,220. At this time yesterday, the price was trading at $64,852

- Ethereum is also trading at $3426. At this time yesterday, the price was trading at $3465.30

In the premarket, the snapshot of the major indices are trading mixed :

- Dow Industrial Average futures are implying a decline of – 91.08 points. Yesterday, the Dow Industrial Average felt -533.06 points or -1.29% at 40,665.63

- S&P futures are implying a gain of 4.91 points. Yesterday, the S&P index closed down -43.70 points or -0.78% at 5544.55

- Nasdaq futures are implying a gain of 26 points. Yesterday, the index fell -125.70 points or -0.70% at 17871.22

- The Russell 2000 index fell -41.38 points or -1.85% at 2198.28

European stock indices are trading lower across the board:

- German DAX, -0.70%

- France CAC -0.66%

- UK FTSE 100, -0.53%

- Spain’s Ibex, -0.49%

- Italy’s FTSE MIB, -0.70% (delayed 10 minutes).

Shares in the Asian Pacific markets closed mixed.

- Japan’s Nikkei 225, -0.16%

- China’s Shanghai Composite Index, +0.17%

- Hong Kong’s Hang Seng index, -2.03%

- Australia S&P/ASX index, -0.1%

Looking at the US debt market, yields are higher:

- 2-year yield 4.500%, +2.4 basis points. At this time yesterday, the yield was at 4.462%

- 5-year yield 4.152%, +3.1 basis points. At this time yesterday, the yield was at 4.106%

- 10-year yield 4.229%, +2.5 basis points. At this time yesterday, the yield was at 4.182%

- 30-year yield 4.441%, +1.7 basis points at this time yesterday, the yield was at 4.397%

Looking at the treasury yield curve ):

- The 2-10 year spread is at -27.1 basis points. At this time yesterday, the spread was at -27.6 basis points.

- The 2-30 year spread is -5.6 basis points. At this time yesterday, the spread was at -6.4 basis points

This article was written by Greg Michalowski at www.forexlive.com.

Source link