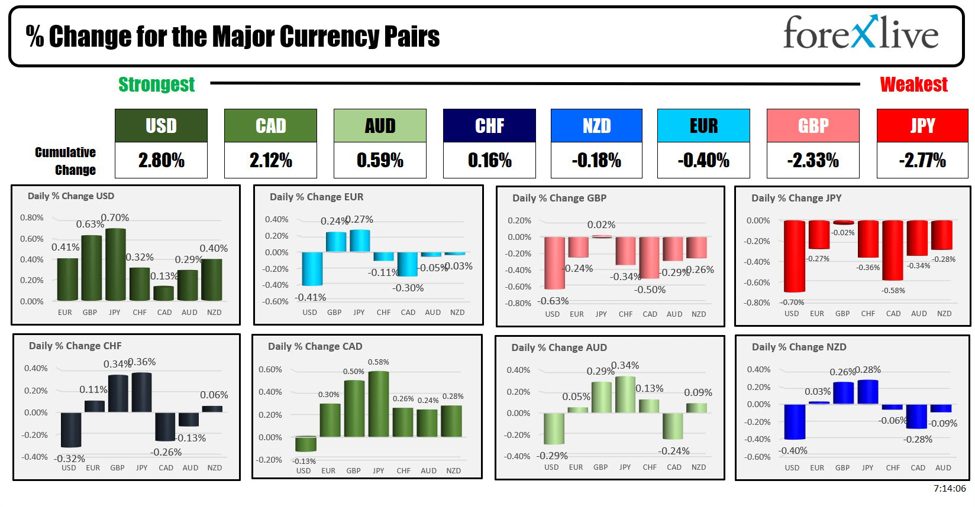

As the North American session begins, the USD is the strongest and the JPY is the weakest. It is a rebound day. Yields have moved higher. Stocks are higher. The USD is higher.

Kickstarting the rebound is the Nikkei rebounded 10.23% its best day since October 2008 which is just a day after plunging 12.4% which was its worse day since 1987. The USDJPY moved to a low yesterday of 141.67 which got within 68 pips of the end of year levels at 140.99. Given the run higher that saw the USDJPY in 2024 to a high of 161.94 on July 3rd, the near complete run lower in 23 trading days is impressive. The catalyst? The BOJ raised rates finally, while the Fed is looking to cut rates. Commentary is also focused on the unwind of the “carry trade” where leveraged investors sold JPY and bought USDs (and other currencies) to fund purchases and investments outside Japan. I don’t know… it hasn’t been a surprise has it?

In central bank news, the Reserve Bank of Australia (RBA) decided to maintain its cash rate at 4.35% in its August 2024 monetary policy announcement, a decision widely anticipated by market analysts. This marks the continuation of the current interest rate level set in previous months as the central bank navigates a challenging economic landscape.

Key Points from the RBA Decision/statement:

Inflation Concerns:

- Inflation remains above the RBA’s target and is proving to be persistent.

- Underlying inflation is still too high, indicating that price pressures are more entrenched than previously anticipated.

- The process of bringing inflation back to target has been slow and uneven.

Labor Market Dynamics:

- High unit labor costs and persistent inflation suggest there are upside risks to prices.

- While wages growth appears to have peaked, it remains higher than the level sustainable with trend productivity growth.

Economic Activity:

- Momentum in economic activity has been weak, as evidenced by slow GDP growth.

- There remains a high level of uncertainty regarding the international economic outlook, which could impact Australia’s economic performance.

Future Policy Considerations:

- The RBA emphasizes that policy will need to be sufficiently restrictive until there is confidence that inflation is moving sustainably towards the target range.

- The central bank is not ruling anything in or out for future policy steps, indicating a flexible and responsive approach to emerging economic data and conditions.

RBA Governor Michele Bullock followed the rate decision by highlighted that inflation progress has been slow over the past year, with a persistent risk that it may take too long to return to the target range. She emphasized that interest rates might need to stay higher for longer to ensure inflation is controlled and that a near-term reduction in the cash rate is not aligned with the current thinking of the RBA Board. She also indicated that the board considered raise rates. Bullock noted that recent market volatility is mostly due to adjustments to financial news and developments, urging caution and calm. The RBA remains vigilant to upside risks to inflation and is prepared to raise rates if necessary. She acknowledged the high degree of economic uncertainty and stressed that market expectations for rate cuts are premature and not in line with the Board’s perspective.

The AUDUSD did move above its 200-hour MA after the decision but failed. The 2nd test of the MA then found willing sellers leaning against the level (see green line on the chart below)..

In the US, Federal Reserve Bank of San Francisco President Mary Daly indicated that the Fed is open to cutting rates in the coming meetings. She emphasized the importance of a steady approach and highlighted that risks to the Fed’s mandates are becoming more balanced. Daly expressed concern about potential deterioration in the job market but noted that the July jobs report, influenced by temporary layoffs and a hurricane, showed signs of slowing without indicating a severe downturn. The Fed aims to ensure both employment and inflation goals are met, adopting a proactive policy stance while avoiding overreaction to single data points. She noted that while inflation relief is occurring, it remains above the 2% target, and widespread layoffs are not yet evident. Daly emphasized the need for policy adjustments based on data, with a focus on maintaining economic momentum and avoiding a downturn. She is confident in the Fed’s approach to achieving a sustainable path to 2% inflation, with communication playing a key role in policy adjustment.

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down $0.10 or -0.14% at $72.84. At this time yesterday, the price was at $71.88

- Gold is trading up $2.13 or 0.09% at $2411.30. At this time yesterday, the price was trading at $2391

- Silver is trading down $0.20 or -0.77% at $27.03.. At this time yesterday, the price is trading at $26.84

- Bitcoin is trading at $55,215. At this time yesterday, the price was trading at $51,265. Bitcoin traded at $70,016 on July 29. Yesterday it reached a low of $49,577

- Ethereum is trading at $2459.20. At this time yesterday, the price was trading at $2280.70. Ethereum traded as high as $4092.80 on March 13 and at a high of $3973 on May 27.

In the premarket, the snapshot of the major indices are sharply lower.

- Dow Industrial Average futures are implying a loss of 219 points. Yesterday, the Dow Industrial Average tumbled 1033.99 points or -2.60% at 38,703.28. That was its worst day since March 18.

- S&P futures are implying a gain of 40 points. Yesterday the S&P index felt -160.21 points or -3.00% at 5186.34. There was its worst day since September 2022

- Nasdaq futures are implying a 170 points. Yesterday the index closed lower by -576.08 points or -3.43% at 16200.08.

Looking at some premarket movers:

- Meta Platforms, +1.48%

- Amazon +0.58%

- Apple -1.04%

- Alphabet +0.46%

- Nvidia +2.84%

- Microsoft +1.28%

- Tesla +1.32%

- Caterpillar announced better earnings and is up 3.54%.

- Palentir is up 11.04% after better earnings and raising for guidance

- Uber also announced better earnings and shares are up 7.73%

After the close, Super Micro Computers will announce earnings. For the year, the price is still up 114.18%, but is it down -50.36% from its high at $1229 (current price is at $620 in premarket trading).

European stock indices are trading modestly lower.

- German DAX, -0.05%

- France CAC, -0.51%

- UK FTSE 100, -0.33%

- Spain’s Ibex, -0.56%

- Italy’s FTSE MIB, -0.56% (delayed 10 minutes).

Shares in the Asian Pacific markets closed higher.

- Japan’s Nikkei 225, +10.23%

- China’s Shanghai Composite Index, +0.23%

- Hong Kong’s Hang Seng index, -0.31%

- Australia S&P/ASX index, +0.41%

Looking at the US debt market, yields are moving higher:

- 2-year yield 3.964%, +8.0 basis points. At this time yesterday, the yield was at 3.75%

- 5-year yield 3.695%, +6.8 basis points. At this time yesterday, the yield was at 3.509%

- 10-year yield 3.840%, +5.8 basis points. At this time Friday, the yield was at 3.709%

- 30-year yield 4.110%, +4.0 basis points. At this time Friday, the yield was at 4.045%

Looking at the treasury yield curve, the spreads are showng

- The 2-10 year spread is at -12.2 basis points. At this time yesterday, the spread was at -13.0 basis points.

- The 2-30 year spread is at +15.0 basis points. At this time yesterday, the spread was +32.1 basis points.

In the European debt market, the benchmark 10-year yields are mostly lower:

This article was written by Greg Michalowski at www.forexlive.com.

Source link