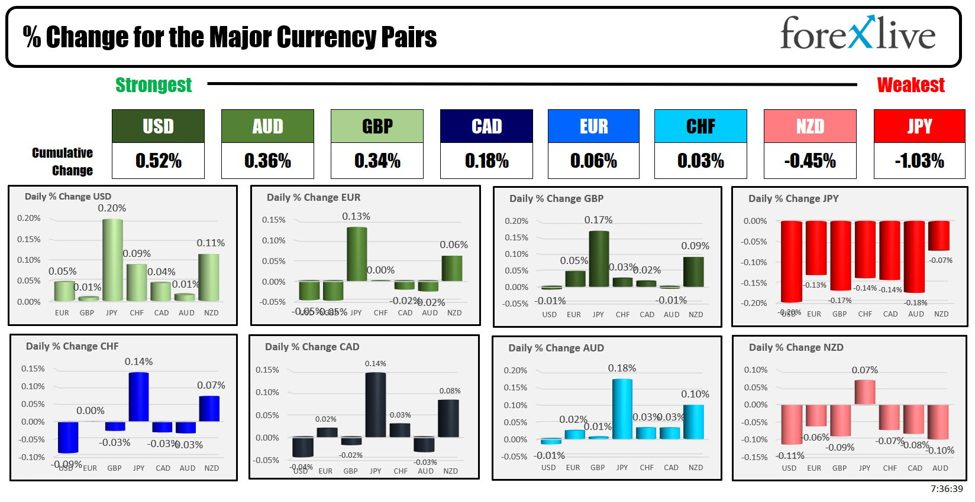

The USD is the strongest and the JPY is the weakest as the North American session begins. Relatively speaking, however, the major currencies are scrunched together to start the new session.

Today, the Fed Chair Powell will give his semi-Annual Monetary Policy Report before the Senate Banking Committee, in Washington DC. The recent data has been slower. As Adam points our in his post, the key question is whether he is ready to signal “greater confidence” that inflation is trending lower. Last week at Sintra, he hinted in this direction, noting that recent data indicates improvements in wages and a significant progress in PCE data at +2.6% year-over-year. He emphasized the need to see more progress on inflation and to ensure that the current data accurately reflects underlying inflation trends. He stressed the importance of taking time to get this right, cautioning that acting too soon could undermine the progress made in controlling inflation. Nevertheless, he is also reluctant to implicitly say a September cut is coming. The Fed does not want to get caught making too many promises. There is CPI and PPI data later in the week. The US stock market continues to hum along, but it is still “the economy” and it seems to be slowing. So hearing his words and dicing and slicing them toward the conclusion that a September cut is still likely, will be the market’s focus. His text release for his testimony is expected at 8:30 AM ET.

In Europe today, ECB executive board member Fabio Panetta stated that the European Central Bank can gradually reduce interest rates in line with the ongoing disinflation process. He emphasized the need for readiness to respond swiftly to any economic shocks, whether upward or downward. Panetta noted that previous rate hikes will continue to suppress demand, output, and inflation for the coming months. Additionally, he expects wage growth to ease as part of this process. The overwhelming consensus is that a July change is off table (it is summer anyway in Europe and they take it easy in the summer). September is still on the table.

The JPY is moving lower which means the USDJPY is moving higher again. Technically as the NA session is beginning, the USDJPY buyers are making a play to the upside by extending above its 100/200 hour MA. Both those MAs are near 161.05 (see blue and green lines on the chart below). The current price has moved above and trades at 161.09. Recall from yesterday, the low price stalled just ahead of the April high at 160.209 and the swing lows from June 27 and June 28. The low reached 160.25 before bouncing.

Today the US treasury will auction off three-year notes to kick off the coupon auctions this week. That will continue tomorrow with the auction of 10-year notes and on Thursday with auction of 30 year bonds.

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down -$0.28 or -0.34% at $82.05. At this time yesterday, the price was at $82.50

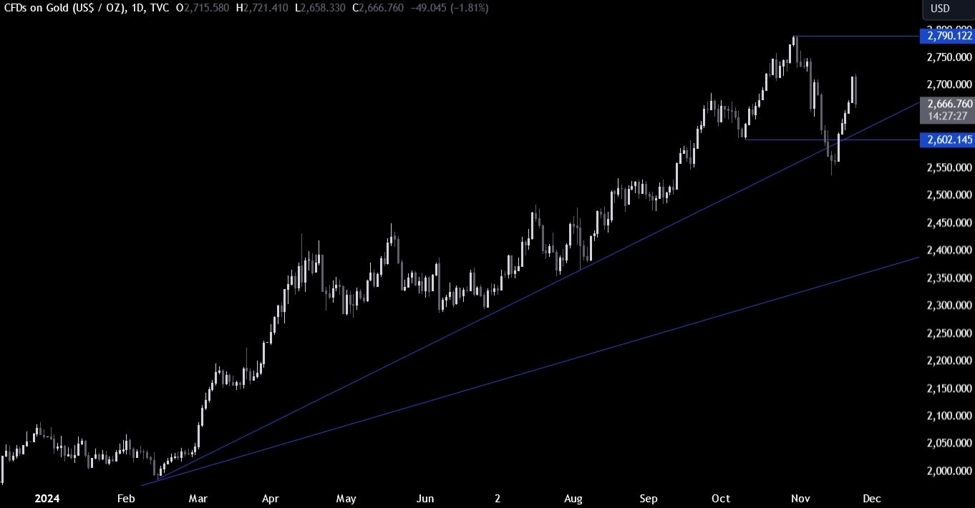

- Gold is trading up $2.25 or 0.10% at $2360.64. At this time yesterday, the price was trading at $2375.41

- Silver is trading up $0.26 or 0.86% at $31.05. At this time on yesterday, the price is trading at $31.08

- Bitcoin trading steady at $57,439. At this time yesterday, the price was trading up at $57,109

- Ethereum is also trading little higher at $3081.80. At this time yesterday, the price was trading at $3048.90

In the premarket, the snapshot of the major indices are trading higher. The S&P and NASDAQ continue their strength of record high closing levels. The S&P has closed higher for four consecutive days. The NASDAQ index has closed higher for five consecutive days.

- Dow Industrial Average futures are implying a gain of 25.81 points. Yesterday, the Dow Industrial Average fell -31.08 points or -0.08% at 39344.80

- S&P futures are implying a gain of 11.40 points. Yesterday, the S&P index rose 5.66 points or 0.10% at 5572.86 (a new record close).

- Nasdaq futures are implying a gain of 64 points. Yesterday, the index rose 50.98 points or 0.28% at 18403.74 (a new record)

European stock indices are trading lower as the market continues to digest political changes:

- German DAX, -0.55%

- France CAC -0.87%

- UK FTSE 100, -0.27%

- Spain’s Ibex, -0.82%

- Italy’s FTSE MIB, -0.08% (delayed 10 minutes).

Shares in the Asian Pacific markets were mostly higher

- Japan’s Nikkei 225, +1.96%

- China’s Shanghai Composite Index, +1.26%

- Hong Kong’s Hang Seng index, unchanged

- Australia S&P/ASX index, +0.86%

Looking at the US debt market, yields are higher

- 2-year yield 4.641%, +2.3 basis points. At this time yesterday, the yield was at 4.636%

- 5-year yield 4.255%, +3.0 basis points.. At this time yesterday, the yield was at 4.258%

- 10-year yield 4.295%, +2.7 basis points. At this time yesterday, the yield was at 4.309%

- 30-year yield 4.478%, +2.1 basis points. At this time yesterday, the yield was at 4.504%

Looking at the treasury yield curve the spreads became more negative from yesterday’s levels at this time:

- The 2-10 year spread is at -34.5 basis points. At this time yesterday, the spread was at -32.7 basis points.

- The 2-30 year spread is at -16.4 basis points. At this time yesterday, the spread was at -13.6 basis points.

In the European debt market, yields are higher in the benchmark 10 year note sector:

This article was written by Greg Michalowski at www.forexlive.com.

Source link