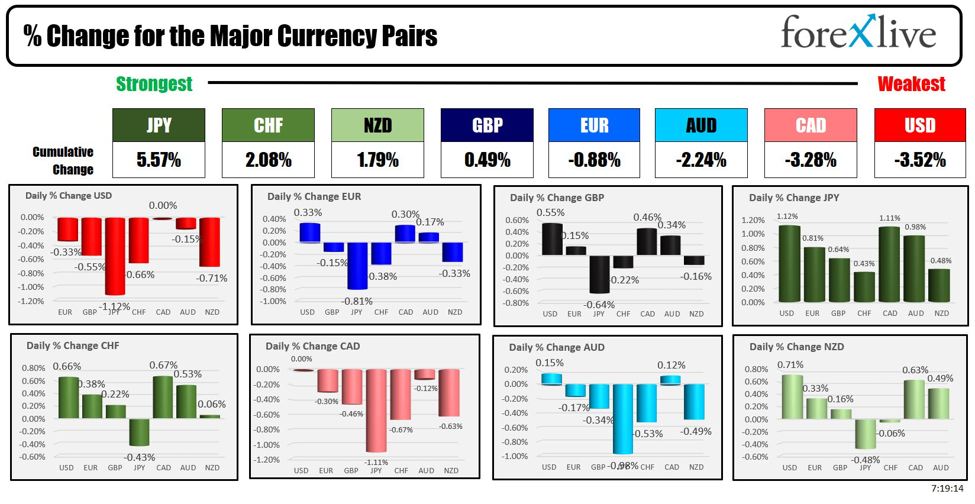

The forex markets has the USD moving higher as the NA sesssion begins. The moves are being led by the USDJPY (and JPY crosses) with a gain of 1.24% after it broke back above its 200-day MA for the first time since July 31.

After moving down from 161.94 to 139.57 from July to September 2024, the USDJPY is now working toward the 61.8% retracement of that move over the last 5 1/2 weeks. That target comes in at 153.39. The high today has reached 152.40.

The USD is also higher vs all the other currencies with the greenback higher by 0.66% vs the AUD and 0.51% vs the NZD

US yields are modestly higher. The 10-year yield moved above its 200-day moving this week and also the 50% midpoint of the 2024 trading range near 4.17%. The 10 yield is now trading at 4.235%.

US stocks are lower in premarket trading with the Dow industrial average down 210 points as McDonalds weighs after announcing an e-coli outbreak in its quarter-pounder (now I crave one). McDonald’s shares are trading down -6.89% in premarket trading.

Starbucks preannounced earnings and they were NOT good after the close. Discretionary spending being felt or is it the “process” at Starbucks that is turning off consumers? I would not know as I have only had Starbucks at an airport. What do you say? Think? Starbucks shares are trading down -3.72%.Crude oil is lower after rising yesterday. Gold is trading modestly higher but once again on pace to another record close. The price is testing a Topside channel trendline on the daily chart.

The Bank of Canada interest-rate decision will be released at 9:45 AM ET and markets expected to cut rates of 50 basis points.

Adam summarized the decision here. Key takeaways:

- Bank of Canada is expected to cut rates by 50 bps on Wednesday, marking the first significant cut in the current cycle.

- OIS market predicts a 90% chance of a 50 bps cut, with a small chance of 25 bps.

- Market expects another 25 bps cut by year-end, with rates declining by 100 bps to 2.50% in 2025.

- Canadian consumer trends are worsening, with CPI at 1.5% y/y, and housing markets, especially in Ontario and British Columbia, struggling.

- There’s potential for rates to drop to 1% if a hard landing scenario occurs.

- Employment remains strong, but public sector layoffs and government changes could impact the economy.

- A dovish 50 bps cut is likely, which may slightly boost USD/CAD, but broader market deterioration would be needed for significant movement.

The press conference will begin at 10:30 AM ET

US existing home sales will be released at 10 AM ET. With estimates of 3.86 million versus 3.86 million last month.

The private weekly oil inventory data was released late yesterday and showed:

Expectations for the EIA data to be released at 10:30 AM ET shows :

- Crude oil +0.270 million

- Gasoline -1.212M.

- Distillates -1.679M

In the forex, a summary with key technical levels shows:

- EURUSD: The EURUSD has continued its downward movement after holding below its 200 day moving average on Monday. Yesterday the price fell below the low from last week at 1.08103, and stayed below that level. As the North American session begins, the price is now breaking below the swing low level from August 1 at 1.0776 which is another bearish tilt, and will have traders looking down toward a swing area at 1.07198 to 1.07346

- GBPUSD: The GBPUSD is breaking below its 100 day moving average again. Yesterday, the price fell below the 100 day moving average at 1.29635 but could not stay momentum to the next target at 1.2938. The low price reached 1.29438. Getting below 1.2938 is the next downside target. Staying below the 100-day moving average at 1.29635 is a close risk and would give the sellers the greatest incentive to push lower if the price remains below that level.

- USDJPY: As mentioned, the USDJPY both above its 200 day moving average at 151.371 like a knife through butter in the Asian session today and has continued the trend like move. The current prices trading at 153.04 as the market stretches toward the 61.8% retracement of the move down from the July high to the September low. The level comes in at 153.397. Close support now is near 151.93 which is a swing level going back to May 2024.

- USDCHF: The USDCHF broke about the highs from last week at 0.86684 reaching a high today of 0.8685. The 100-day moving average of 0.86958 is the next key target. The price last traded above its 100 day moving average back on July 11. Staying above the high from last week at 0.8668 is now close risk for traders looking for more upside momentum. A break below that level could see the price move back toward the broken 38.2% retracement of the move down from the July high at 0.86318.

- USDCAD: Ahead of the Bank of Canada interest-rate decision, the USDCAD is trading back into a Topside swing area between 1.38337 and 1.38475. If the buyers are to continue the trend higher, getting above the 1.38475 and staying above is needed. Yesterday the low came in at 1.3813. Getting below that level would have traders looking toward 1.3788 – 1.37919 area. The USDCAD is overbought signs of consolidation, but if the price breaks above the 1.38475, I would not mess with the trend.

- AUDUSD: The AUDUSD is also breaking and for fell below its 50% midpoint of the move up from the August low to the September high. That midpoint level comes in at 0.66451 and is now close resistance. On the downside the 200 day moving average comes in at 0.66277. Back in September, the price tested that moving average level and found willing buyers. That increases the levels importance. Will buyers come in against that level?. When I know is if it is broken I would expect the technical buyers to turn to sellers.

- NZDUSD: The NZDUSD group below a swing area at 0.6031 to 0.60387. That area will now be upside resistance and a bias changing area in the short term. Move above, and there could be some disappointment on the break with a move back toward 0.60509. On the downside, the natural support at 0.6000 is the next target followed by a swing area between 0.5970 and 0.59836. Yesterday and today, the NZDUSD found willing sellers against its 100 hour moving average currently at 0.60521. The high price today reached 0.60519. Bearish

In earnings released this morning:

- Boeing Co Q3 2024: EPS -10.44 vs estimate -10.34, MISSED. Revenue 17.84 bln vs estimate 17.93 bln, MISSED.

- CME Group Q3 2024: EPS 2.50 vs estimate 2.65, MISSED. Revenue 1.86 bln vs estimate 1.58 bln, BEAT.

- General Dynamics Corp Q3 2024: EPS 3.35 vs estimate 3.47, MISSED. Revenue 11.67 bln vs estimate 11.64 bln, BEAT.

- Coca-Cola Co Q3 2024: EPS 0.77 vs estimate 0.74, BEAT. Revenue 11.9 bln vs estimate 11.6 bln, BEAT.

- AT&T Q3 2024: EPS 0.60 vs estimate 0.57, BEAT. Revenue 30.2 bln vs estimate 30.44 bln, MISSED.

- Boston Scientific Corp Q3 2024: EPS 0.63 vs estimate 0.59, BEAT. Revenue 4.209 bln vs estimate 4.044 bln, BEAT.

- Hilton Worldwide Holdings Q3 2024: EPS 1.92 vs estimate 1.85, BEAT. Revenue 2.86 bln vs estimate 2.85 bln, BEAT.

- Thermo Fisher Scientific Q3 2024: EPS 5.28 vs estimate 5.25, BEAT. Revenue 10.59 bln vs estimate 10.64 bln, MISSED.

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down $1.29 or -1.78% at $70.46. At this time yesterday, the price was at $70.58.

- Gold is trading unchanged at $2749.At this time yesterday, the price was at $2734.11.

- Silver is trading down $0.38 or -1.08% and $34.45. At this time yesterday, the price is at $34.38.

- Bitcoin is trading at $66,256. At this time yesterday, the price was at $67,191

- Ethereum is trading at $2573.90. At this time yesterday, the price was at $2634.90

In the premarket, the snapshot of the major indices are lower after mixed results yesterday.

- Dow Industrial Average futures are implying a decline of -211.12 points. Yesterday, the index fell -6171 points or -0.02% at 42924.89

- S&P futures are implying a loss of – 13.20 points. Yesterday, the index fell -2.78 points or -0.05% at 5851.20

- Nasdaq futures are implying a loss of -67.10 points. Yesterday, the index rose 33.12 points or 0.18% at 18573.13

European stock indices are trading mixed:

- German DAX, -0.13%

- France CAC, -0.57%

- UK FTSE 100, -0.50% %

- Spain’s Ibex, +0.15%

- Italy’s FTSE MIB, unchanged (delayed by 10 minutes)

Shares in Asian Pacific session shares were mostly lower:

- Japan’s Nikkei 225, -0.80%

- China’s Shanghai Composite Index, +0.52%

- Hong Kong’s Hang Seng index, +1.27%

- Australia S&P/ASX index, +0.13%

Looking at the US debt market, yields are trading modestly higher

- 2-year yield 4.050%, +1.3 basis points. At this time yesterday, the yield was at 4.034%

- 5-year yield 4.035%, +3.0 basis points. At this time yesterday, the yield was at 3.98 6%

- 10-year yield 4.235%, +3.0 basis points. At this time yesterday, the yield was at 4.187%

- 30-year yield 4.524%, +3.0 basis points. At this time yesterday, the yield was at 4.488%

Looking at the treasury yield curve close steeper on Friday. At the close

- The 2-10 year spread is at + 18.6 basis points. At this time Friday morning, the yield spread was + 14.5 basis points.

- The 2-30 year spread is at + 47.3 basis points. At this time Friday morning, the yield spread was + 45.3 basis points.

This article was written by Greg Michalowski at www.forexlive.com.

Source link