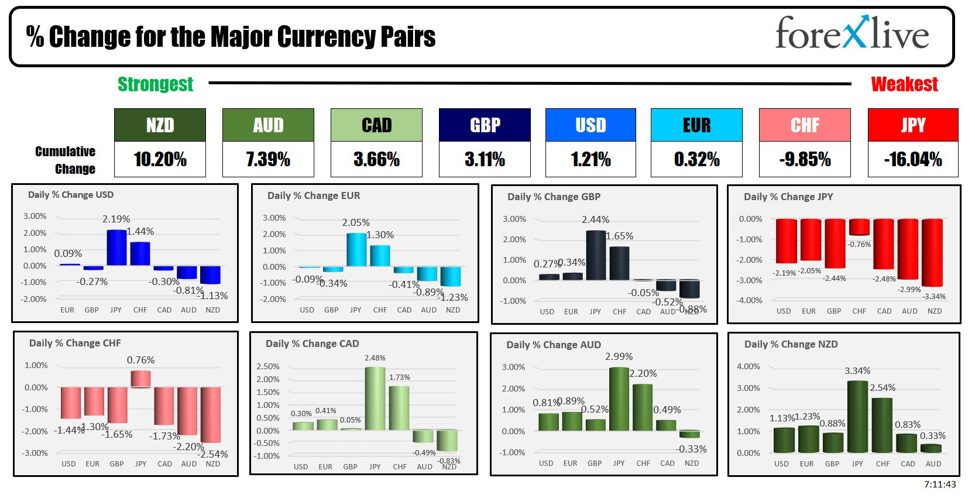

As the North American session begins, the NZD is the strongest and the JPY is the weakest. The USD is mixed to mostly higher thanks to the gains in equities. The NZD and the AUD were supported by a weaker JPY and higher stocks. In New Zealand, employment came in little bit stronger than expectations as well with the unemployment rate lower than expectations..

In Japan, the Nikkei did gain 1.19% helping to reverse the USDJPY back higher as well. The gains in the Nikkei continued its rebound from the -12.4% decline on Monday. From the low on Monday to the high price today, the price has risen 15.20%.

The not-so-good technically is that at the high for the day, sellers leaned against the gap from Friday and Monday (the price got within 30 points short of the Friday close and above the Monday high). The high price today also stayed below the broken 38.2% of the move up from the 2023 low to the 2024 high at 36022 (see chart below). The price high reached 35849.77. So sellers did stall the rally near key resistance.

Overnight, BOJ Deputy Governor Shinichi Uchida eased market concerns by emphasizing that the Bank of Japan’s interest rate path could change if market volatility affects their economic forecasts, risk assessments, and projections. He stated that Japan is not in a situation where they need to hike rates at a set pace and that they will avoid rate hikes during unstable market conditions. Uchida believes the U.S. economy can achieve a soft landing and sees no significant changes in the economic fundamentals of Japan and the U.S., suggesting that market reactions to single U.S. data points are exaggerated. He highlighted the extreme volatility in recent market moves and stressed the importance of monitoring their impact on the economy and prices with vigilance. Uchida also mentioned that there is no difference in views between himself and BOJ Governor Ueda, and that the BOJ has the flexibility to choose when to hike rates in a moderate environment. The comments helped to calm the markets sending the stocks and supporting the USDJPY.

The US stocks are also higher on the day in the premarket with the Dow up over 300 points, the S&P up over 50 points and the Nasdaq up over 220 points currently.

In the US, for the week ending August 2, 2024, the Mortgage Bankers Association reported a significant increase in mortgage applications, rising by 6.9% compared to a 3.9% decline the previous week. The Market Index climbed to 215.1 from 201.2, while the Purchase Index edged up to 133.9 from 132.8. The Refinance Index saw a notable jump to 661.4 from 570.7. The catalyst? The average 30-year mortgage rate dropped to 6.55% from 6.82%, driven by a decline in yields and signals from the Federal Reserve to cut rates. This drop in rates spurred both purchasing and refinancing activities.

Today the weekly oil inventory data will be released. The estimates are for crude stocks to show a drawdown of -0.700M barrels and gasoline to show a drawdown of -0.986M. The price of crude is currently at $74.72 up $1.50 on the day. Late yesterday, the private data showed:

- Crude Oil: Increased by 180,000 barrels

- Gasoline: Increased by 3.31 million barrels

- Distillates: Increased by 1.22 million barrels

- Cushing: Increased by 1.07 million barrels

- Strategic Petroleum Reserve (SPR): Increased by 700,000 barrels

As mentioned the NZDUSD is higher as employment data was better than expectations (but weaker than prior quarter). Higher stocks also helped to support the currency. .

- Labour Cost Index (YoY): Increased by 3.6%, slightly above the expected 3.5% but below the prior 3.8%.

- Labour Cost Index (QoQ): Rose by 0.9%, higher than the 0.8 expected

- Participation Rate: increased to 71.7%, versus 71.5% last month and 71.3% expected

- Employment Change: Improved by 0.4%, significantly better than the expected -0.2% and the prior -0.2%.

- Unemployment Rate: Came in at 4.6%, slightly below the expected 4.7% but higher than the prior 4.3%.

Looking at the NZDUSD, the price is approaching key resistance between 0.6032 and 0.6036 where both the 200 bar MA on the 4-hour chart and the 100-day moving average are located (see chart below). I would expect sellers against that area if approached. The price broke above its 100 bar moving average and 38.2% retracement earlier in the day and also above the 50% midpoint the of the natural support at 0.6000. That level is now close support – and did hold support on a corrective move today (see the 50% level on the chart below).

Today the economic calendar in light in the US with consumer credit the only release at 3 PM ET. The U.S. Treasury will auction 10 year notes at 1 PM:

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading up $1.65 or 2.24% at $74.84. At this time yesterday, the price was at $72.84

- Gold is trading up $13.80 or 0.58% at $2402. At this time yesterday, the price was trading at $2411.30

- Silver is trading up $0.15 or 0.55% or $27.11.. At this time yesterday, the price is trading at $27.03

- Bitcoin is trading at $56,929. At this time yesterday, the price was trading at $55,215.

- Ethereum is trading at $2469.70. At this time yesterday, the price was trading at $2459.20.

In the premarket, the snapshot of the major indices are higher.

- Dow Industrial Average futures are implying a gain of 290 points. Yesterday, the Dow Industrial Average gained 294.39 points or 0.76% at 38997.67

- S&P futures are implying a gain of 52 points. Yesterday the S&P index gained 53.70 points or 1.04% at 5240.04

- Nasdaq futures are implying gain of 217 points. Yesterday the index gained 166.77 points or 1.03% at 16366.85

The small-cap Russell 2000 rose 25.14 points or 1.23% at 2064.30 yesterday.

European stock indices are trading higher

- German DAX, +1.10%

- France CAC, +1.40%

- UK FTSE 100, +1.12%

- Spain’s Ibex, +1.61%

- Italy’s FTSE MIB, +1.85% (delayed 10 minutes).

Shares in the Asian Pacific markets closed higher helped by comments from BOJ Uchida. Other indices in the Far East were higher:

- Japan’s Nikkei 225, +1.19%

- China’s Shanghai Composite Index, +0.09%

- Hong Kong’s Hang Seng index, +1.38%

- Australia S&P/ASX index, +0.25%

Looking at the US debt market, yields are moving higher:

- 2-year yield 4.005%, +2.0 basis points. At this time yesterday, the yield was at 3.964%

- 5-year yield 3.767%, +3.8 basis points at this time yesterday, the yield was at 3.695%

- 10-year yield 3.931%, +4.4 basis points. At this time Friday, the yield was at 3.840%

- 30-year yield 4.227%, +5.1 basis points. At this time Friday, the yield was at 4.11%

Looking at the treasury yield curve, the spreads are steepening with the 2– 10 year spread only negative by -7.1 basis points

- The 2-10 year spread is at -7.1 basis points. At this time yesterday, the spread was at -12.2 basis points.

- The 2-30 year spread is at +22.5 basis points. At this time yesterday, the spread was was 15.0 basis points.

In the European debt market, the benchmark 10-year yields are moving higher:

This article was written by Greg Michalowski at www.forexlive.com.

Source link