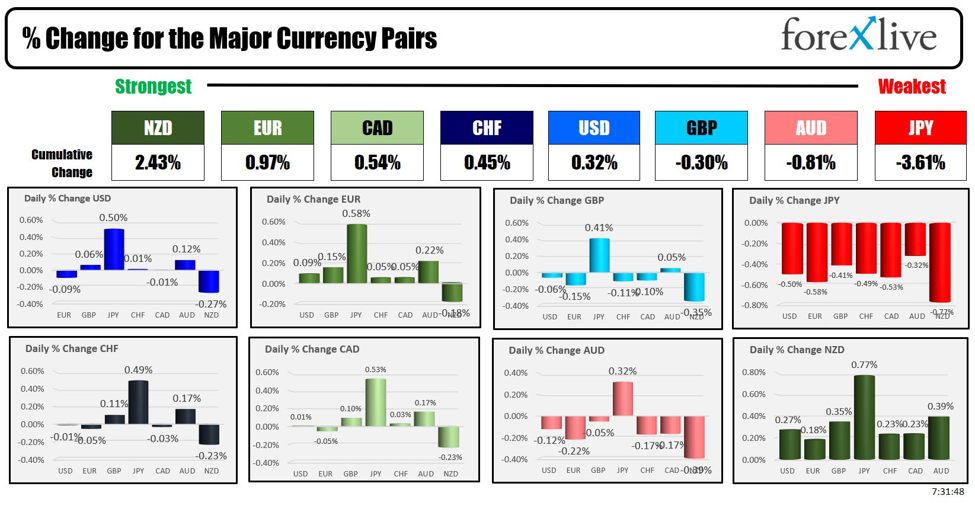

As the North American session begins, the NZD is the strongest and the JPY is the weakest.

We are still a day away from the FOMC rate decision where the Fed is likely to keep rates unchanged with a tilt to an ease in September. The Fed will NOT release the dot-plot of rate forecast or views from all members on growth, employment and inflation. The statement and the comments from Fed Chair Powell will have to do. That will be followed with Fedspeak later this week and next week.

The Bank of England rate decision is on Thursday with market experts split. The Bank of Japan will announce their decision tonight (tomorrow in Japan). While the “Market” is pricing in a 70% chance of a 10 bp hike, economists are less certain (9 of 46 – see post here).

“The case for hiking rests entirely upon gauging the degree of the BoJ’s confidence that it is durably on the path toward achieving 2% inflation over the medium-term horizon while getting further distance away from the distorting near-zero policy rate of 10bps.” (see post here)

Meanwhile, ING’s latest ahead of the Bank of Japan meeting is looking for a hike (and 15 basis points):

- We believe that the recently released inflation and labour data continue to justify the Bank of Japan’s rate normalisation.

- We are expecting a 15bp hike tomorrow, but the decision is still up in the air.

- Currently, the market is pricing in a 60% chance of a hike.

- In our view, the Bank of Japan is convinced that the virtuous cycle between wages and consumption is strengthening.

- However, real wage growth has remained in negative territory, which could lead the BoJ to keep policy rates on hold.

German CPI came in higher at 0.3% this morning versus 0.2% estimate. The YoY went to 2.3% up from 2.2% estimate and last month. The HICP was also higher with MoM at 0.5% vs 0.4% estimate and YoY at 2.6% vs 2.5% est and 2.5% last month. Going the wrong way on inflation.

Earnings will continue to be an important market-moving wave today and going forward this week with Microsoft, Apple, Amazon and Meta all schedule to release this week. For a technical look at Microsoft CLICK HERE.

Looking at the earnings released this morning:

Corning Inc (GLW) Q2 2024 (USD):

- Core EPS: 0.47 (expected: 0.46) – Beat

- Revenue: 3.6 bln (expected: 3.54 bln) – Beat

PayPal Holdings Inc (PYPL) Q2 2024 (USD):

- Adj. EPS: 1.19 (expected: 0.99) – Beat

- Revenue: 7.89 bln (expected: 7.82 bln) – Beat

- Raises FY EPS view

Archer-Daniels-Midland Co (ADM) Q2 2024 (USD):

- EPS: 1.03 (expected: 1.22) – Miss

- Revenue: 22.25 bln (expected: 23.18 bln) – Miss

- Affirms Full-Year EPS Guidance

Phillips 66 (PSX) Q2 2024 (USD):

- Adj. EPS: 2.31 (expected: 1.98) – Beat

Procter & Gamble Co (PG) Q2 2024 (USD):

- Adj. EPS: 1.40 (expected: 1.37) – Beat

- Revenue: 20.532 bln (expected: 20.74 bln) – Miss

Pfizer Inc (PFE) Q2 2024 (USD):

- Adj. EPS: 0.60 (expected: 0.46) – Beat

- Revenue: 13.28 bln (expected: 12.96 bln) – Beat

- Raises 2024 guidance

Merck & Co Inc (MRK) Q2 2024 (USD):

- EPS: 2.28 (expected: 2.15) – Beat

- Revenue: 16.1 bln (expected: 15.84 bln) – Beat

JetBlue Airways Corp (JBLU) Q2 2024 (USD):

- Adj. EPS: 0.08 (expected: -0.13) – Beat

- Revenue: 2.428 bln (expected: 2.4 bln) – Beat

Looking ahead, AMD, MIcrosoft, Starbucks and Pinterest all report after the close today. On Wednesday, Meta Platforms reports, and on Thursday Amazon and Apple report. Other big earnings come from Boeing, Intel, Exxon Mobil, Chevron:

- After close: AMD, Microsoft, Starbucks, Pinterest

Wednesday

- Before the open: Boeing, Kraft Heinz, Altria

- After close: Meta (Facebook), Qualcomm, Carvana, Lam Research, Western Digital

Thursday

- Before the open: Moderna, ConocoPhillips, Wayfair, SiriusXM

- After close: Amazon, Apple, Intel, Coinbase, DraftKings

Friday

- Before the open: ExxonMobil, Chevron, Frontier Communications

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down $0.43 or -0.57% at $75.37. At this time yesterday, the price was at $76.83

- Gold is trading up $4.30 or 0.18% at $2388.29 . At this time yesterday, the price was trading at $2387.90

- Silver is trading down four cents or -0.15% at $27.79. At this time yesterday, the price is trading at $28.01

- Bitcoin trading at $66,658 little change from yesterdays close but lower from this time yesterday. At this time yesterday, the price was trading at $69,435

- Ethereum is trading at $3338.60. At this time yesterday, the price was trading at $3373.30

In the premarket, the snapshot of the major indices is to the upside ahead of more of the earnings tidal wave this week:

- Dow Industrial Average futures are implying a gain of 19.07 points . Yesterday, the Dow Industrial Average fell -49.41 points or -0.12% at 40539.94

- S&P futures are implying a gain of 14.46 points . Yesterday the S&P index closed higher by 4.46 points or 0.08% at 5463.55

- Nasdaq futures are implying a gain of 70 points . Yesterday the index closed higher by 12.32 points or 0.07% at 17370.20

- Yesterday, the Russell 2000 index fell -24.73 points or -1.09% at 2235.33

European stock indices are trading.

- German DAX, +0.44%

- France CAC, +0.39%

- UK FTSE 100, -0.15%

- Spain’s Ibex, +0.44%

- Italy’s FTSE MIB, +0.66% (delayed 10 minutes).

Shares in the Asian Pacific markets closed higher:.

- Japan’s Nikkei 225, +0.15%

- China’s Shanghai Composite Index, -0.43%

- Hong Kong’s Hang Seng index, -1.37%

- Australia S&P/ASX index, -0.46%

Looking at the US debt market, yields are trading lower:

- 2-year yield 4.389%, +0.2 basis points. At this time yesterday, the yield was at 4.3709%

- 5-year yield 4.066%, -0.4 basis points. At this time yesterday, the yield was at the 4.048%

- 10-year yield 4.170%, -0.8 basis points. At this time Friday, the yield was at 4.160%

- 30-year yield 4.423%, -1.0 basis points. At this time Friday, the yield was at 4.414%

Looking at the treasury yield curve, the spreads are mixed compared to this time yesterday

- The 2-10 year spread is at -21.9 basis points. At this time yesterday, the spread was at -21.2 basis points.

- The 2-30 year spread is at 3.5 basis points. At this time yesterday, the spread was -2.1 basis points.

In the European debt market, the benchmark 10-year yields are lower:

This article was written by Greg Michalowski at www.forexlive.com.

Source link