(

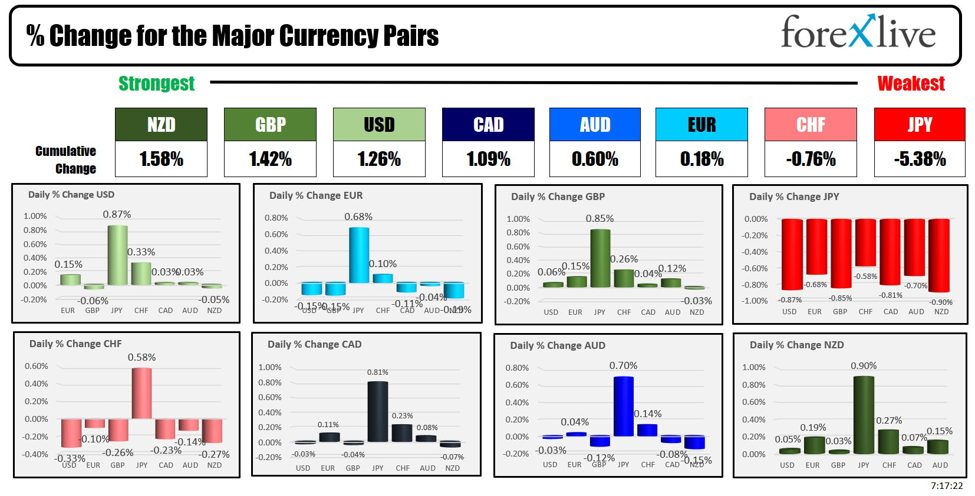

As the North American session begins the NZD is the strongest and the JPY (which was the strongest currency yesterday) is the weakest. The USD is mixed/stronger thanks to the 0.87% gain vs the JPY and a 0.33% gain vs the CHF.

The US ADP employment report (released at 8:15 AM ET) will continue the progression to the key BLS jobs data on Friday where the expectation is for 185K gain in non-farm payroll (with unemployment rate at 3.9%). The expectation for the ADP is for a gain of 175K vs 192K last month.

Also on tap today will be the Services PMI and ISM data (estimate 50.8 vs 49.4 last month). Last month, the employment component from the PMI came in at 45.9 (lowest level since January at 43.3). FYI, new orders last month were at 52.2 and prices paid was at 59.2.

Some weaker data of late and subsequent decline in yields has the market pricing in a roughly 65% chance the Fed will cut by 25 basis-point in September. Last week, the probability was below 50%.

EIA weekly oil inventory data will be released at 10:30 AM ET with expectations of -2.311M drawdown. Gasoline is expected to show a buildup 1.964M. Late yesterday the crude oil inventories showed a surprise buildup of 4.052 million. The gasoline inventories showed a build of 4.026 million.

In Canada today, the Bank of Canada rate decision will take place at 9:45 AM ET with the expectations of a cut of 25 basis points to 4.75% from 5.0%. A total of 22 of 29 economists surveyed by Reuters expect the cut. The market is pricing in an 80% chance. So there is some question whether it is this month or will they wait a month? The USDCAD, like the USD, is mixed to higher with most of the gains vs the JPY.BOC Macklem will have a press conference starting at 10:30 AM ET.

In Australia overnight, Reserve Bank of Australia Governor Bullock indicated that Q1 GDP growth is expected to be low, citing weak economic conditions reflected in reduced consumption. Bullock, along with Assistant Governor (Financial Markets) Kent, presented these insights before the Senate Economics Legislation Committee. Despite the slow reduction in underlying inflation, the core inflation measure is rising, with the latest trimmed mean at 4.1% y/y, up from 4.0%. The persistent demand exceeding supply capacity continues to exert inflationary pressures. Bullock emphasized the flexibility in policy, stating that if inflation remains persistent, the RBA will not hesitate to hike rates, but if the economy weakens significantly, easing measures will be considered. Additionally, the labor market is showing signs of easing, and the board currently views monetary policy as restrictive.

The move higher today in the USDJPY is a bit of a mystery with little in the way of a fundamental catalyst. Nevertheless, the pair is stepping/trending higher with little in the way of corrective price action. Technically, the price yesterday bottomed near a swing area between 154.59 and 154.87. The high price reached 156.294. That is just short of the point 100-day moving average at 156.352. There is a stall against that moving average level. Watching close support at 155.954 now (see chart below).

A snapshot of the other markets as the North American session begins shows

- Crude oil is trading up $0.33 or 0.44% at $73.58. At this time yesterday, the price was at $72.85

- Gold is trading up $7.60 or 0.33% at $2333.64. At this time yesterday, the price was higher at $2327.50

- Silver is trading up eight cents or 0.28% at $29.56. At this time yesterday, the price was at $29.77

- Bitcoin currently trades at $70,956. At this time yesterday, the price was trading at $68,945

- Ethereum is trading at $3805.10. At this time yesterday, the price trading at $3759.40

In the premarket, the snapshot of the major indices are higher. Yesterday the major indices closed higher as well:

- Dow Industrial Average futures are implying a gain of 70.71 points. Yesterday, Dow Industrial Average rose 140.26 points or 0.36% at 38711.30

- S&P futures are implying a gain of 17.91 points. Yesterday, the S&P index rose 7.94 points or 0.15% at 5291.35

- Nasdaq futures are implying a gain of 112.91 points. Yesterday, NASDAQ index rose 28.38 points or 0.17% at 16857.05.

European stock indices are trading higher today in the US morning snapshot:

- German DAX, +1.08%

- France CAC , +0.98%

- UK FTSE 100, +0.35%

- Spain’s Ibex, +0.95%

- Italy’s FTSE MIB, +1.18% (delayed 10 minutes).

Shares in the Asian Pacific markets were mostly lower:

- Japan’s Nikkei 225, -0.89%

- China’s Shanghai Composite Index, -0.83%

- Hong Kong’s Hang Seng index, -0.10%

- Australia S&P/ASX index, +0.41%

Looking at the US debt market, yields are trading mostly lower after yesterday’s declines. Yields have declined for 4 consecutive days. The 10 year yield has moved from a May 29 high at 4.63%. The low yield yesterday reached 4.314%.

- 2-year yield 4.774%, +0.4 basis points. At this time yesterday, the yield was at 4.805%

- 5-year yield 4.348%, -0.4 basis points. At this time yesterday, the yield was at 4.401%

- 10-year yield 4.324%, -1.2 basis points. At this time yesterday, the yield was at 4.386%

- 30-year yield 4.466%, -1.8 basements. At this time yesterday, the yield was at 4.536%

Looking at the treasury yield curve the spreads are more negative versus yesterday at this time:

- The 2-10 year spread is at -45.0 basis points. At this time yesterday, the spread was at -41.8 basis points.

- The 2-30 year spread is at -31.0 basis points. At this time yesterday, the spread was at -26.6 basis points.

In the European debt market yields in the benchmark 10-year yields are trading lower:

This article was written by Greg Michalowski at www.forexlive.com.

Source link