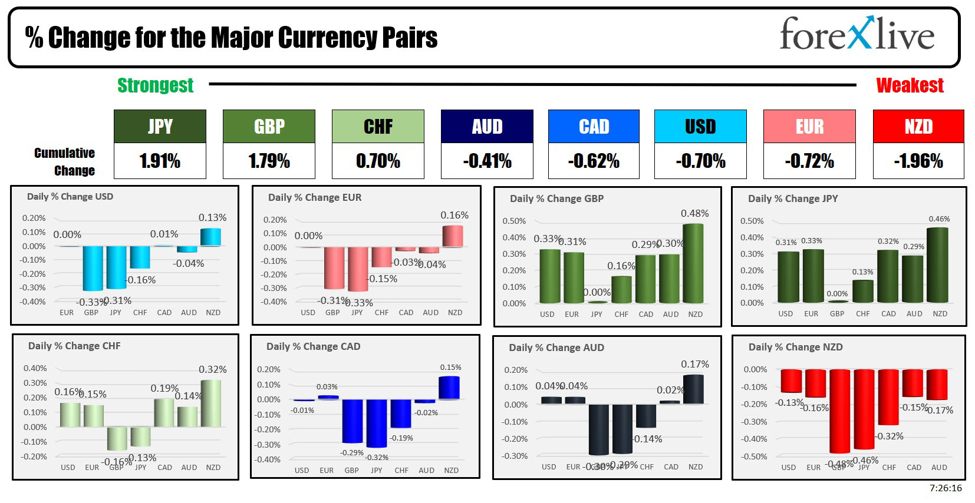

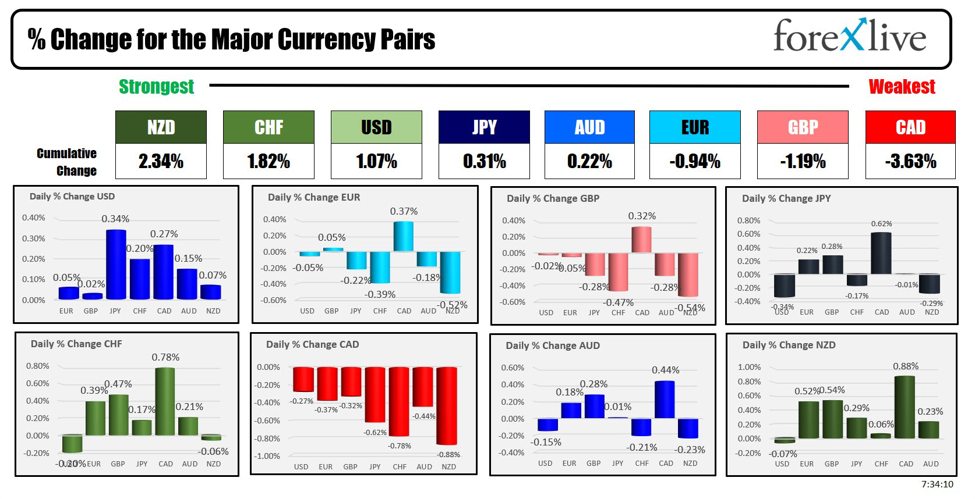

As the NA session begins, the NZD is the strongest and the CAD is the weakest. The USD is stronger ahead of the PPI and also the Canada employment report for September.

The PPI is expected to rise by 0.1% for the headline and the 0.2% for the core (ex food and energy). The YoY are expected at 1.6% for headline and 2.7% (and 2.4% from last month) for the core. The CPI data was higher yesterday by 0.1% for both the headline and the core which has the markets on edge for Fed policy going forward.

For the Canada jobs data, the employment change is expected at 27K with the unemployment rate stretching up to 6.7% (would be the highest since November 2021). The USDCAD has been moving sharply higher since November 2 at 1.3472. The high today reached 1.3778 with the next topside target at 1.38035.

Chicago Fed President Austan Goolsbee, speaking on Bloomberg’s Odd Lots, emphasized that inflation has significantly cooled, and the labor market remains strong, with unemployment at levels the Fed is satisfied with. He expressed confidence that inflation will continue moving towards the 2% target, noting that policymakers’ projections reflect this outlook. Goolsbee cautioned against overreacting to single data points and highlighted the market’s trust in the Fed’s ability to manage inflation, contrasting the current situation with the 1970s, where inflation expectations escalated, which hasn’t happened this time.

Yesterday, Atlanta Fed Pres. Bostic said that he could say skipping a November rate decline.The expectation of no change in November is up to about 18% (with 82% expecting a 25 basis point cut). Dallas Fed Pres. Logan also was cautious about policy changes at the next meeting.

Looking at the economic data out of Europe today, most came out of the UK with mixed results.

- German Final CPI m/m: Actual 0.0%, Forecast 0.0%, Previous 0.0% (MET forecast)

- GBP GDP m/m: Actual 0.2%, Forecast 0.2%, Previous 0.0% (MET forecast)

- GBP Construction Output m/m: Actual 0.4%, Forecast 0.5%, Previous -0.4% (MISSED forecast)

- GBP Goods Trade Balance: Actual -15.1B, Forecast -18.8B, Previous -18.9B (BEATforecast)

- GBP Index of Services 3m/3m: Actual 0.1%, Forecast 0.3%, Previous 0.4% (MISSEDforecast)

- GBP Industrial Production m/m: Actual 0.5%, Forecast 0.2%, Previous -0.7% (BEAT forecast)

- GBP Manufacturing Production m/m: Actual 1.1%, Forecast 0.3%, Previous -1.2% (BEAT is forecast

Earnings season was kicked off today with financials leading the way. Apart from Wells Fargo which missed on Revenues, the other reports show beats led by JPM. Shares are higher on the news. Below is how some of the major companies reported today:

-

JPMorgan Chase & Co (JPM) Q3 2024: Shares are up 1.26%

- EPS: $4.37 (expected $4.01) → BEAT

- Revenue: $43.32 billion (expected $41.63 billion) → BEAT

-

Wells Fargo & Co (WFC) Q3 2024: Shares are up 3.62%

- EPS: $1.42 (expected $1.28) → BEAT

- Revenue: $20.36 billion (expected $20.81 billion) → MISS

-

Bank of New York Mellon Corp (BK) Q3 2024: is are up 1.41%

- EPS: $1.52 (expected $1.42) → BEAT

- Revenue: $4.85 billion (expected $4.54 billion) → BEAT

-

BlackRock Finance Inc (BLK) Q3 2024: is are up 2.33%

- EPS: $11.46 (expected $10.33) → BEAT

- Revenue: $5.22 billion (expected $5.01 billion) → BEAT

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down -$0.63 or -0.80% at $75.32. At this time yesterday, the price was at $74.12

- Gold is trading up $16 or 0.61% at $2645.73. At this time yesterday, the price was $2612.30

- Silver is trading up nine cents or 0.31% at $31.24. At this time yesterday, the price is at $30.57

- Bitcoin is trading near levels from this time yesterday at $61,156. At this time yesterday, the price was at $61,193

- Ethereum is trading at $2417.80. At this time yesterday, the price was at $2403.10

In the premarket, the snapshot of the major indices trading modestly lower after yesterday’s declines.

- Dow Industrial Average futures are implying decline of -20.10 points. Yesterday, the index now -57.88 points or -0.14% at 42454.12

- S&P futures are implying a decline of – -5.8 points. Yesterday, the index fell -11.99 points or -0.21% at 5780.05

- Nasdaq futures are implying a decline of -64.01 points. Yesterday, the index fell -9.57 points or -0.05% at 18282.05

Yesterday, the small-cap Russell 2000 fell -12.16 points or 0.55% at 2188.41

European stock indices are trading modestly higher:

- German DAX, +0.20%

- France CAC, +0.07%

- UK FTSE 100, -0.04%

- Spain’s Ibex, +0.30%

- Italy’s FTSE MIB, +0.10% (delayed by 10 minutes)

Shares in Asian Pacific session shares were mixed:

- Japan’s Nikkei 225, +0.57%

- China’s Shanghai Composite Index, -2.55%

- Hong Kong’s Hang Seng index, on holiday

- Australia S&P/ASX index, -0.10%

Looking at the US debt market, yields are lower with the two year yield back below the 4.000% level

- 2-year yield 3.978%, -2.1 basis points. At this time yesterday, the yield was at 4.053%

- 5-year yield 3.912%, -0.7 basis points. At this time yesterday, the yield was at 3.943%

- 10-year yield 4.092%, -0.2 basis points. At this time yesterday, the yield was at 4.092%

- 30-year yield 4.356%, +1.8 basis points. At this time yesterday, the yield was at 4.356%

Looking at the treasury yield curve is steeper

- The 2-10 year spread is at +11.6 basis points. At this time yesterday, the yield spread was +3.8 basis points.

- The 2-30 year spread is at +41.7 basis points. At this time yesterday, the yield spread was +30.2 basis points.

In the European debt market, the 10 year yields are trading higher

This article was written by Greg Michalowski at www.forexlive.com.

Source link