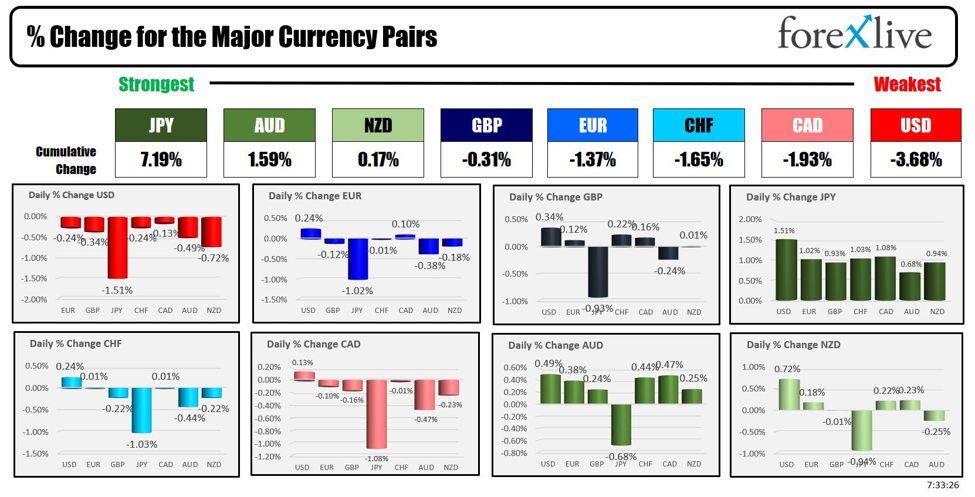

As the North American session begins, the JPY is the strongest of the major currencies, while the USD is the weakest. The move lower in the dollar is mostly attributed to a -1.51% fall vs the JPY after the USDJPY raced to a high of 160.21 and nearly to the April 1990 high at 160.40, before tumbling lower on the back of reported intervention from the Bank of Japan (Bloomberg reported citing the Dow Jones). The move higher came despite Japan being on holiday (Showa Day). The move to the downside took the pair initially down to test the pairs 200 hour MA (green line on the chart below currently at 155.192 – the low reached 155.04). The reactionary bounce off the MA support took the pair to a high of 157.17 before another flush out took the pair to a low for the day at 154.509. The price is trading higher again and back above the 200 and 100 hour MAs at 1551.914 and 155.83 respectively.

Looking at the other JPY pairs, they too have moved back to the downside with the EURJPY falling from its multi decade high at 171.56 (the 2008 high reached 169.958) to low of 165.22 (just below its 200-hour MA). Its price is back above its 100-hour MA at 166.84 (trading at 167.377 now). It is trading around 1.02% lower on the day.

Today, Germany preliminary CPI data for April came in at 0.5% versus 0.6% expected. The YoY rose 2.2% versus 2.3% expected (unchanged from prior month). THe HICP preliminary for April came in at 0.6% MoM (as expected) and 2.4% vs 2.3% estimate (and 2.3% last month).

Although today is void of any major US releases (and the Fed is still in the quiet period ahead of its Fed decision on Wednesday), this week will be busy with the Fed rate decision on Wednesday, the US jobs report on Friday and a slew of earnings scheduled. Below is a look at some of the key events and releases along with the schedule of the major earnings releases:

Tuesday, April 30

- China PMI. Expectations 50.3 versus 50.8 last month

- Canada GDP MoM (8:30 AM ET). Estimate 0.3% versus 0.6% last month.

- US employment cost index for the first quarter (10 AM ET). 1.0% versus 0.9% last quarter

- US consumer confidence (10 AM ET). Estimate 104.0 versus 104.7 last month

Wednesday, May 1

- New Zealand employment statistics (6:45 PM ET, Tuesday). Employment change 0.3% versus 0.4% last quarter. Unemployment rate 4.3% versus 4.0 present

- US ADP nonfarm employment change (8:15 AM ET). Estimate 180K versus 184K last month

- US ISM manufacturing (10 AM ET). Estimate 50.0 versus 50.3 last month

- US JOLTs job openings (10 AM ET). Estimate 8.68 million versus 8.76 million last month

- Federal Reserve interest rate decision (2 PM ET). No change expected

- Federal Reserve press conference (2:30 PM ET)

Thursday, May 2

- Swiss CPI MoM (2:30 AM ET). Estimate 0.2% versus 0.0% last month.

- US initial jobless claims (8:30 AM ET). Estimate 210K versus 207K last week.

- Bank of Canada’s Macklem speaks (8:45 AM ET)

Friday, May 3

- US jobs statistics (8:30 AM ET). Non-farm payroll estimate 250K versus 303K last month. Unemployment rate 3.8% versus 3.8% last month. Average hourly earnings of 0.3% versus 0.3% last month.

- US ISM services PMI (10 AM ET). Estimate 52.0 versus 51.4 last month.

In addition to the key economic releases,the earnings calendar next week will once again be full of a number of key large-cap stocks. Below is a sampling of the major releases for each trading day (* is after the close):

- Monday, April 29: Paramount*, Logitech*

- Tuesday, April 30: PayPal, 3M, McDonald’s, Coca-Cola, Amazon *, AMD*, Super Micro Computers*, Starbucks*

- Wednesday, May 1: Pfizer, CVS, MasterCard, Qualcomm

- Thursday, May 2: Moderna, Apple *,Coinbase *, Fortinet *, DraftKings *

A snapshot of the other markets as the North American session begins currently shows.:

- Crude oil is trading little changed at $83.76. At this time Friday, the price was at $84.35.

- Gold is trading down $0.77 at $2337.11. At this time Friday, the price was higher at $2345.83

- Silver is trading up 12% or 0.50% at $27.33.. At this time Friday, the price was at $27.60

- Bitcoin currently trades at $62,310. At this time Friday, the price was trading at $63,342

In the premarket, the US major indices are trading modestly higher after gains in training last week.

- Dow Industrial Average futures are implying a gain of 74 point. On Friday, the index rose 153.86 points or 0.40% at 38239.67

- S&P futures are implying a gain of 11.10 points points. On Friday, the index rose 51.54 points or 1.02% at 5099.95

- Nasdaq futures are implying a gain of 65 points points. On Friday, the index rose 316.14 points or 2.03% at 15927.90

The European indices are trading mixed ahead of the US open:

- German DAX, -0.06%

- France CAC , +0.12%

- UK FTSE 100, +0.39%

- Spain’s Ibex, -0.74%

- Italy’s FTSE MIB, -0.15% (delayed 10 minutes)

Shares in the Asian Pacific markets were mostly higher

- Japan’s Nikkei 225, closed for holiday

- China’s Shanghai Composite Index, +0.79%

- Hong Kong’s Hang Seng index, +0.54%

- Australia S&P/ASX index, +0.1%

Looking at the US debt market, yields are mostly lower after rising yesterday after the GDP data.

- 2-year yield 4.978%, -2.1 basis points. At this time yesterday, the yield was at 4.999%

- 5-year yield 4.653%, -2.9 basis points at this time yesterday, the yield was at 4.70%

- 10-year yield 4.623%, -4.5 basis points. At this time yesterday, the yield was at 4.685%

- 30-year yield 4.737%, -4.4 basis points. At this time yesterday, the yield was at 4.791%

Looking at the treasury yield curve spreads moved more inverted:

- The 2-10 year spread is at -35.5 basis points. At this time yesterday, the spread was at -31.4 basis points

- The 2-30 year spread is at -24.2 basis points. At this time yesterday, the spread was at -21.0 basis points

European benchmark 10-year yields are lower:

This article was written by Greg Michalowski at www.forexlive.com.

Source link