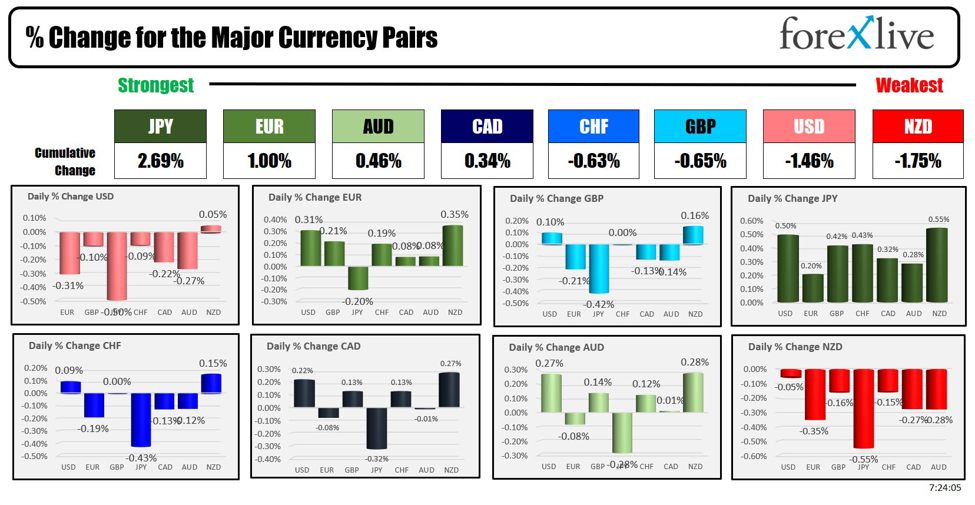

The JPY is the strongest and the NZD is the weakest as the North American session begins. The USD is lower ahead of the US CPI data. Stocks (in premarket trading) and bond yields are also lower to start the US session.

The consensus on the headline number is +0.2% m/m and +2.6% y/y. The latter would be the lowest since 2021. In fact, anything below last month’s 2.9% reading will be the lowest since 2021. Adam points out in his preview post:

More importantly will be the core number, which excludes food and energy. The consensus there is for a 0.2% m/m reading and a 3.2% y/y/y reading, in part because home prices and rents are taking some time to filter through. Another metric the Fed will be watching is ‘supercore’ inflation, which is CPI services ex-housing. It was at 4.5% y/y last month and that’s a reminder that goods are doing all the heavy lifting in the report at the moment, in part because insurance rates take a long time to be passed on.

The forex market reaction? Adam points out:

“Overall, I see downward risks to the US dollar and the potential for a rise in risk assets on this report. A upside miss should be easily brushed aside because of the pressure from oil and raw materials that’s looming. Meanwhile, a downside miss will raise the possibility the Fed could tag 2% inflation this year. There are some base effects that reverse late in the year that will add some pressure but the lower track will underscore that inflation is yesterday’s problem.”

The CPI will be released at 8:30 AM ET.

Later at 10:30 AM, the weekly EIA oil inventory data will be released at 10:30 AM with:

- Crude oil +0.987M estimate.

- Gasoline -0.109M estimate

- Distillates +0.313M estimate

Looking at the private data released late yesterday showed yet another larger than expected drawdowns of crude -2.79M

In the European session the UK data dump this morning mostly missed expectations:

- GDP m/m: 0.0% (Forecast: 0.2%, Previous: 0.0%) – MISSED expectations.

- Construction Output m/m: -0.4% (Forecast: 0.4%, Previous: 0.5%) – MISSED expectations.

- Goods Trade Balance: -20.0B (Forecast: -18.0B, Previous: -18.9B) – MISSED expectations.

- Index of Services 3m/3m: 0.6% (Forecast: 0.6%, Previous: 0.8%) – MET expectations.

- Industrial Production m/m: -0.8% (Forecast: 0.3%, Previous: 0.8%) – MISSED expectations.

- Manufacturing Production m/m: -1.0% (Forecast: 0.2%, Previous: 1.1%) – MISSED expectations.

In the US, the mortgage applications rose by 1.4% helped by the lowest 30 year mortgage rate since January 31 at 6.29%

The presidential debate is over with the consensus that Harris won.

The US treasury will auction off 10 year notes at 1 PM. The 3-year note auction yesterday was met with very strong demand from international investors. They showed up and bought.

As a reminder, the Fed is in a blackout period ahead of the interest-rate decision next Wednesday. More immediately, the ECB will announce its interest-rate decision tomorrow, with the main refinancing rate expected to fall to 3.65% from 4.25%. The ECB deposit rate is expected to fall to 3.5% from 3.75%.

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading up $1.70 or 2.57% at $67.43. At this time yesterday, the price was at $67.70

- Gold is trading up $7.62 or 0.31% at 2523.80. At this time yesterday, the price was at $2506.17

- Silver is trading up $0.46 or 1.64% at $28.84. At this time yesterday, the price is at $28.42

- Bitcoin is trading $860 or -1.49% at $56,801. At this time yesterday, the price was at $57,264

- Ethereum is trading down $49 or -2.08% at $2328.90. At this time yesterday, the price was at $2354

In the premarket, the snapshot of the major indices are mixed/modestly changed after gains yesterday

- Dow Industrial Average futures are implying fall of -94 points.. Yesterday, the index fell -92.64 points or -0.23% at 40736.96

- S&P futures are implying a decline of -6.77 points. Yesterday, the index rose 24.47 points or 0.45% at 5495.52

- Nasdaq futures are implying a loss of -22.16 points. Yesterday, the index rose 141.28 points or 0.84% at 17025.88

Yesterday, the small-cap Russell 2000 was near unchanged at 2097.43

European stock indices are trading modestly higher:

- German DAX, +0.46%

- France CAC, +0.31%

- UK FTSE 100, +0.21%

- Spain’s Ibex, +0.91%

- Italy’s FTSE MIB, +0.08% (delayed 10 minutes).

Shares in the Asian Pacific markets closed modestly higher:

- Japan’s Nikkei 225, -1.49%

- China’s Shanghai Composite Index, -0.82%

- Hong Kong’s Hang Seng index, -0.73%

- Australia S&P/ASX index, -0.30%

Looking at the US debt market, yields are little changed:

- 2-year yield 3.581%, -2.8 basis points. At the same Friday, the yield was at 3.674%

- 5-year yield 3.400%, -2.6 basis points.. At this time Friday, the yield was at 3.502%

- 10-year yield 3.618%, -2.6 basis points. At this time Friday, the yield is at 3.717%

- 30-year yield 3.932%, -2.3 basis points. At this time Friday, the yield is at 4.018%

Looking at the treasury yield curve,

- The 2-10 year spread is +3.7 basis points. At this time yesterday, the yield spread was +4.2 basis points.

- The 2-30 year spread is +35.6 basis points. At this time yesterday, the yield spread was +34.2 basis points.

In the European debt market, the 10 year yields are lower:

This article was written by Greg Michalowski at www.forexlive.com.

Source link