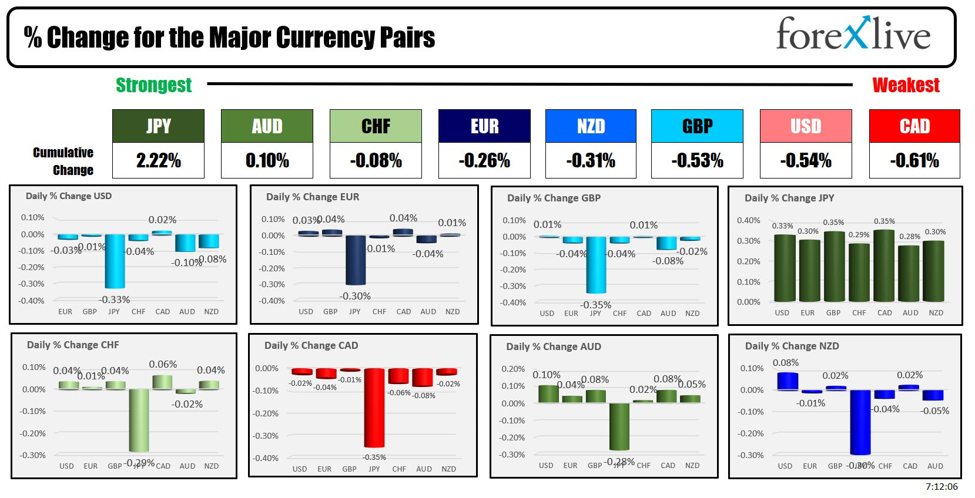

As the North American session begins, the JPY is the strongest and the CAD is the weakest. Looking at the currencies other than the JPY above, if it weren’t for the declines vs the JPY, the changes of all the currencies would be minimal for all of the major currencies vs each other. Trading ranges for the USD vs the majors is relatively modest as the last 1/3 of the trading day is approaching. The USDJPY has an 80 pip trading range with a 22-day average (about a month) of 188 pips. The other ranges are 35 pips or less with the EURUSD only 25 pips currently (vs a 22 day average of 57 pips). That says either there is room to roam today (to extend the trading ranges, or that the market is unsure of the next moves and would rather watch.

Watch what?

The forex market is watching the US major stock indices which moved sharply lower yesterday with the Nasdaq down more than 3.25% with Nvidia leading the way lower as it had it’s worst day since April 19 when the stock fell an even -10%. After the close, there was a report that Nvidia received a subpoena by the dept of Justice in antitrust probe of AI business. Yesterday the decline was -9.53%. Today the stock and the indices are trading lower with the Nasdaq down another -130 points and Nvidia down another -1.6% or so. The European shares are all lower today. In the Asian Pacific session, the Nikkei 225 fell -4.24% and Australia S&P/ASX index fell -1.88%.

The market is watching the yields. The US 10 year yield is down -3 bps after falling nearly 9 bps yesterday. European 10 year yields are also lower today (and were lower yesterday).

The market is watching – and waiting – for the key US jobs report on Friday ahead of the Federal Reserve meeting on September 18. The data yesterday was not all that great, but there is mixed employment data pre-NFP with the initial claims settling near 231K vs a peak near 250K a month or so ago. There is speculation that the number will help make the decision by the Fed between a 25 bp cut or 50 bp cut. See related posts HERE and HERE.

Oil prices rebounded today after bouncing near $70 yesterday. The high last week moved to $77.60.

There is a lot to watch but the forex market is not reacting at least so far today (PS watch the technicals for clues of a move).

Key on the economic calendar today:

- Bank of Canada rate decision at 9:45 AM ET. Adam sees the chance (he puts it at 50-50) for a 50 bp cut but the market is only expecting a 23% chance. The market is expecting a 25 basis point cut to 4.25% from 4.5%.

- US factory orders for July and revision to US durable goods orders will be released at 10 AM ET. Factory orders are expected to rise by 4.7% after declining by -3.3% last month.

- JOLT job openings will be released at 10 AM with expectations for 8.100M vs 8.184M last month

- Just ahead at 8:30 AM the US and Canada trade data will be reported. In the US the trade deficit is expected at -79.0B vs -73.1B last month. In Canada, the est. is for a surplus

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading up $0.50 at $70.82. At this time yesterday, the price was at $72.47

- Gold is trading down $3.36 or -0.13% at $2489.02. At this time yesterday, the price was at $2488.47. Goldman has 3 reasons to buy gold.

- Silver is trading up one cent or 0.08% at $28.05. At this time yesterday, the price is at $28.28.

- Bitcoin is trading lower at $56,615. At this time yesterday, the price was at $59,129

- Ethereum is trading lower at $2401.50. At this time yesterday, the price was at $2509.40

In the premarket, the snapshot of the major indices are lower after sharp declines yesterday

- Dow Industrial Average futures are implying a decline of -81.25 points. Yesterday the index fell -626.15 points or -1.51% at 40,936.94

- S&P futures are implying a decline of -21.28 points. Yesterday the index fell -119.47 points or -2.12% at 5528.92

- Nasdaq futures are implying a decline of -135.24 points. Yesterday the index fell-577.33 points or -3.26% at 17136.30

yesterday, the small-cap Russell 2000 fell -60.42 points or -3.09% at 2149.21

European stock indices are trading lower

- German DAX, -0.91%

- France CAC, -1.13%

- UK FTSE 100, -0.53%

- Spain’s Ibex, -0.71%

- Italy’s FTSE MIB, -0.49% (delayed 10 minutes).

Shares in the Asian Pacific markets closed lower:

- Japan’s Nikkei 225, -4.24%

- China’s Shanghai Composite Index, -0.67%

- Hong Kong’s Hang Seng index, -1.1%

- Australia S&P/ASX index, -1.88%

Looking at the US debt market, yields are little changed:

- 2-year yield 3.848%, -3.9 basis points. At the same yesterday, the yield was at 3.931%

- 5-year yield 3.618%, -3.6 basis points. At this time yesterday, the yield was at 3.718%

- 10-year yield 3.810%, -3.4 basis points. At this time in yesterday, the yield is at 3.911%

- 30-year yield 4.103%, -2.8 basis points. At this time yesterday, the yield is at 4.193%

Looking at the treasury yield curve,

- The 2-10 year spread is at -3.3 basis points. At this time yesterday, the yield spread was -1.8 basis points.

- The 2-30 year spread is at +25.7 basis points. At this time yesterday, the yield spread was caused 26.3 basis points.

In the European debt market, the 10 year yields are lower:

This article was written by Greg Michalowski at www.forexlive.com.

Source link