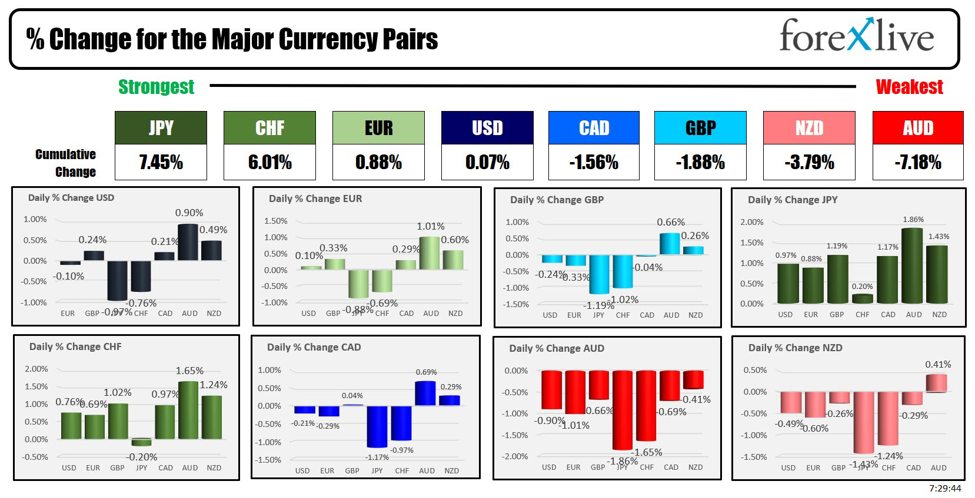

As the North American session begins, the JPY is the strongest of the major currencies (again), while the AUD (and NZD) is the weakest (again). The USD is mixed with declines vs the JPY and the CHF (they are the safe haven – again), offset by gains vs the AUD and NZD (they are the weak links – again).

It’s the day after the worst declines in the broader S&P and NASDAQ indices since 2022. Japan’s Nikkei index had its worst day since June 2021.

In China, the PBOC had another surprise cut when they lowered the Medium-Term Lending Facility (MLF) by 20 basis points. ING commented on the decision saying the move was surprising for two main reasons: the timing and the scale of the cut.

- Despite keeping the MLF rate unchanged earlier this month, most analysts expected any rate adjustments to occur next month. However, given the broader direction towards monetary easing and the real economy’s needs, the PBOC acted sooner.

- Additionally, the 20bp reduction was larger than the expected 10bp cut to the 7-day reverse repo rate and the 10bp reductions in the Loan Prime Rates (LPR).

ING noted that this larger cut could support banks’ interest margins, although further LPR reductions might follow as a consequence.

China’s slowing economy is hurting the AUD and NZD and also helping to push commodities like crude oil, copper and silver lower.

- Crude oil is down nearly -10% since July 5

- Silver is down -13.39% since July 11.

- Copper is down -22% from its recent peak in May.

In Europe, ECB’s Nagel commented on the current economic situation, stating that the “greedy inflation beast is no more.” He emphasized that the ECB is adopting a meeting-by-meeting approach and cannot pre-commit to any actions for September. Nagel mentioned that rate cuts could be possible if data remains on track but stressed the need to maintain a restrictive policy until inflation reaches 2%. He also noted that the path to stabilizing inflation is expected to be bumpy.On tap in the US session today includes:

- Advance GDP q/q: Forecast: 2.0%, Previous: 1.4%

- Advance GDP Price Index q/q: Forecast: 2.6%, Previous: 3.1%

- Unemployment Claims: Forecast: 237K, Previous: 243K

- Durable Goods Orders m/m: Forecast: 0.3%, Previous: 0.1%

- Core Durable Goods Orders m/m: Forecast: 0.2%, Previous: -0.1%

Recall that last week, the initial jobless claims did spike higher to 243K. If there is another move higher it will be bad, but it might get the Fed’s attention to preempt with a cut in policy next week.

Also, today, the U.S. Treasury portion of seven year notes. The two-year note auction was stellar on Tuesday. Yesterday the five-year note was ok but also had a positive tail (auctioned at a higher yield vs the WI level). The seven year will decide the success or failure of the auctions this week.

The earnings calendar is full motion. After the close yesterday IBM, ServiceNow and Chipotle beat estimates. Ford fell short of expectations with EPS.

IBM: Shares are up 3.85% in premarket

- Revenues 15.77 billion versus 15.62 billion estimat – BEAT

- EPS $2.43 versus $2.20 expected- BEAT

Chipotle: Shares are up 3.77% in premarket

- Revenues $2.97 billion versus $2.94 billion expected: BEAT

- EPS $0.34 versus $0.32 expected: BEAT

ServiceNow: Shares are up 7.03% in premarket

- Revenues $2.63 billion versus $2.61 billion BEAT

- EPS $3.13 versus $2.84 estimate BEAT

Ford: Shares are down -13.53% in premarket activity

- Revenues $47.8 billion versus $44.02 billion estimate BEAT

- EPS $0.47 versus $0.68 estimate MISS

This mornings earnings releases were highlighted by the following companies:

Nasdaq Inc (NDAQ) Q2 2024: Shares are up 0.75%

- Adjusted EPS: $0.69 vs. $0.64, BEAT

- Revenue: $1.16 billion vs. $1.13 billion, BEAT

American Airlines Group Inc (AAL) Q2 2024: Shares are down -8.36%

- Adjusted EPS: $1.09 vs. $1.05, BEAT

- Revenue: $14.334 billion vs. $14.36 billion, MISSED

Northrop Grumman Corp (NOC) Q2 2024: Shares up 2.01% in premarket

- EPS: $6.36 vs. $5.93, BEAT

- Revenue: $10.22 billion vs. $10.02 billion, BEAT

Southwest Airlines Co (LUV) Q2 2024: Shares are down -4.81%. They are bagging

- EPS: $0.58 vs. $0.51, BEAT

- Revenue: $7.4 billion vs. $7.32 billion, BEAT

Royal Caribbean (RCL) Q2 2024: Shares are still down -2.13% despite the beat and raised guidance/dividend reinstatement. Go figure.

- Adjusted EPS: $3.21 vs. $2.75, BEAT

- Net Income: $850 million vs. $770 million, BEAT

- Reinstates Dividend: $0.40/share vs. $0.00

- Increases FY guidance: Adjusted EPS $11.35-11.45 vs. $11.08

RTX (RTX) Q2 2024: Shares are up 3.02% in premarket for the defense contractor.

- Adjusted EPS: $1.41 vs. $1.30, BEAT

- Revenue: $19.72 billion vs. $19.28 billion, BEAT

- Raises FY guidance: Adjusted EPS $5.35-5.45 vs. $5.38, Revenue $78.75-79.5 billion vs. $78.99 billion

Hasbro Inc (HAS) Q2 2024: Shares are up 7.69% in premarket on the big beat.

- Adjusted EPS: $1.22 vs. $0.78, BEAT

- Revenue: $953 million vs. $940 million, BEAT

Dow Inc (DOW) Q2 2024:Shares are down -4.82% premarket on the miss.

- EPS: $0.68 vs. $0.72, MISSED

- Revenue: $10.92 billion vs. $11.01 billion, MISSED

Honeywell International Inc (HON) Q2 2024: Shares are down -4.53%

- EPS: $2.49 vs. $2.42, BEAT

- Revenue: $9.6 billion vs. $9.41 billion, BEAT

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down -$1.23 at $76.36. At this time yesterday, the price was at $77.90

- Gold is trading down $-26 or -1.09% at $2371.44. At this time yesterday, the price was trading at $2417.72

- Silver is trading down $1.34 or -4.67% at $27.57 as the price reacts to expected slower growth. At this time yesterday, the price is trading at $29.33

- Bitcoin trading down and trades at $64,208 . At this time yesterday, the price was trading at $66,461. Yesterday, the price was trading in between the 100 and 200 hour MA, but then broke below and the sellers entered (see chart below).

- Ethereum is trading lower at $3174.03 . At this time yesterday, the price was trading at $3465.40

In the premarket, the snapshot of the major indices are trading lower with the declines led by the NASDAQ index.

- Dow Industrial Average futures are implying a loss of -4.2 points. Yesterday, the Dow Industrial Average fell -504.22 points or -1.25% at 39853.88

- S&P futures are implying a loss of -6.88 points. Yesterday, the S&P index closed lower by -128.63 points or -2.32% at 5427.12. The change was its worst trading day since December 2022

- Nasdaq futures are implying a decline of -42 points in modal trading. Yesterday, the index closed lower by -654.94 points or -3.64% at 17342.41. That was its worst trading day since November 2022.

- Yesterday, the Russell 2000 index fell -47.89 points or -2.13% at 2195.37.

European stock indices are trading lower :

- German DAX, -1.17%

- France CAC, -1.90%

- UK FTSE 100, -0.50%

- Spain’s Ibex, -1.26%

- Italy’s FTSE MIB, -2.53% (delayed 10 minutes).

Shares in the Asian Pacific markets closed lower:.

- Japan’s Nikkei 225, -3.28% which is its worst date since June 2021

- China’s Shanghai Composite Index, -0.52%

- Hong Kong’s Hang Seng index, -1.77%

- Australia S&P/ASX index, -1.29%

Looking at the US debt market, yields are trading mixed:

- 2-year yield 4.366%, -4.9 basis points. At this time yesterday, the yield was at 4.420%

- 5-year yield 4.088%, -6.3 base points. At this time yesterday, the yield was at 4.131%

- 10-year yield 4.225%, -6.1 basis points. At this time yesterday, the yield was at 4.231%

- 30-year yield 4.495%, -5.3 basis points. At this time yesterday, the yield was at 4.472%

Looking at the treasury yield curve, it is a steepening. The two – 30 year spread move back into positive territory.

- The 2-10 year spread is at -14.4 basis points. At this time yesterday, the spread was at -18.5 basis points. The high today was the highest since -11.8 basis points from October 23, 2023.

- The 2-30 year spread is +12.6 basis points. At this time yesterday, the spread was +5.6 basis points. The high today reached the highest level since July 2022

In the European debt market, the benchmark 10 year yields are lower:

This article was written by Greg Michalowski at www.forexlive.com.

Source link