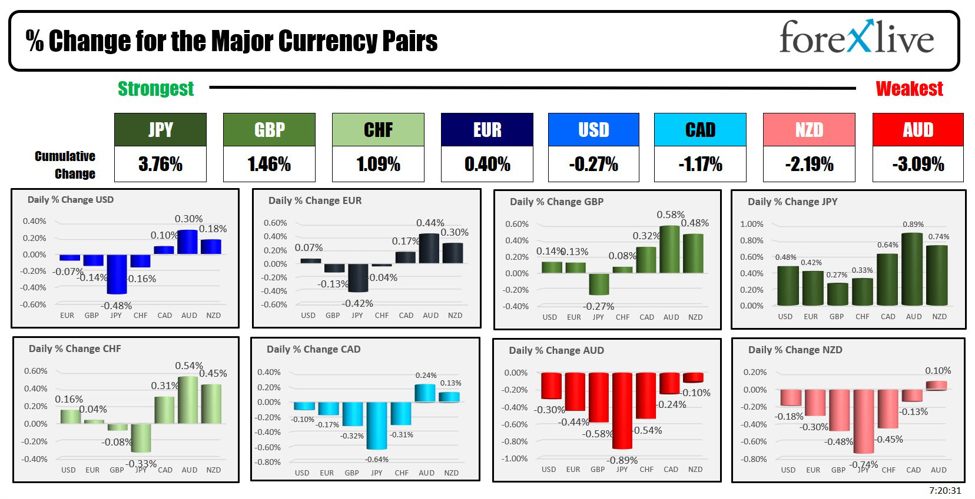

The JPY is the strongest and the AUD is the weakest as the NA session begins. The USD is mixed after the weekend news of the Pres. Biden stepping down and endorsement of Kamala Harris as the Presidential candidate. Can she turn the Dem story and negative momentum around? Who will be her VP candidate and how will he/she tilt the ticket bias? Mark Kellly from Arizona is a potential candidate who is more center. An ex-astronaut. His wife Gabby Giffored was a former US Representative who has shot and disabled. He is still a proponent of the 2nd amendment introducing the GOSAFE legislation that

- “Protects the rights of responsible gun owners while regulating the most dangerous semi-automatic rifles, detachable high-capacity magazines, and accessories that have increasingly concerned law enforcement and been used over and over again in mass shootings”

Will Harris tilt more toward the center? What does it mean for Trump and his momentum? The Democratic National Convention is not until August 19-22. That is good and gives time to regroup. Does Joe Manchin make a play?

In hindsight, the change has occurred at the peak of the Trump momentum. The attempted assassination has come and gone.. The RNC immediately thereafter is over. In my opinion, GOP nominee Trump had the opportunity to hit a home run at his acceptance speech, but when he goes to the “best of” with things like the “late great Hannibal Lecter” the pendulum swings back to his shortcomings.

Overall, the feeling is that it is more of a horse race. Time will tell. But stocks are higher led by the Nasdaq index. Yields are mixed vs Friday’s close.

Also over the weekend as the NA session begins, the People’s Bank of China cut its benchmark loan prime rates to record lows, with the one-year rate at 3.35% and the five-year rate at 3.85%, to support the slowing economy after weak GDP data last week. This follows promises of more stimulus from Chinese officials, though market sentiment remains weak amid speculation of Donald Trump’s potential second U.S. presidential term, which could renew trade tensions.

The Fed black out period has started ahead of the Fed meeting at the end of the month. The economic calendar is slow this week. Globally flash PMI data will be released. The Bank of Canada is expected to cut rates with inflation moving lower and with softer retail sales last week adding to that tilt. The advanced US GDP will be released on Thursday along with unemployment claims. Recall, that the unemployment claims did rise to 242K last week (highest since August 2023). The US PCE data – the Fed’s favorite inflation measure – will be released on Friday and is the biggest economic release of the week.

Then there is the earnings calendar this week with 2 of the Magnificent 7 scheduled to release (Tesla and Alphabet on Tuesday). A myriad of other industry leaders will also report:

Tuesday:

- GM

- Coca Cola

- Tesla

- Alphabet

- Visa

- Texas Instrument

Wednesday:

- AT&T

- General Dynamic

- Chipotle

- Ford

- ServiceNow

- IBM

- Whirlpool

Thursday

- American Airlines

- Honeywell

- Southwest Airlines

- Juniper

- Deckers

Friday:

- 3M

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down $-0.46 or -0.58% at $78.18. At this time Friday, the price was at $81.03

- Gold is trading down $-4.95 or -0.20% at $2395.70. At this time Friday, the price was trading at $2408.47

- Silver is trading and $0.39 or -1.34% at $28.81. At this time Friday, the price is trading at $29.07

- Bitcoin trading at $67,432 after a sharp move higher over the weekend. At this time Friday, the price was trading at $64,220

- Ethereum is also trading at $3494.80. At this time Friday, the price was trading at $3426

In the premarket, the snapshot of the major indices are trading mixed :

- Dow Industrial Average futures are implying a gain of 48.02 points. On Friday, the Dow Industrial Average -377.49.4-0.93% at 40,287.54.

- S&P futures are implying a gain of 34.25 points. On Friday, the S&P index closed lower by -39.59 points or -0.71% at 5504.99

- Nasdaq futures are implying a gain of 191 points. On Friday, the index fell -144.28 points or -0.81% at 17726.94

- The Russell 2000 index fell -13.93 points or -0.63% at 2184.34

European stock indices are trading hired across the board:

- German DAX, +1.42%

- France CAC +1.34%

- UK FTSE 100, +0.81%

- Spain’s Ibex, +0.76%

- Italy’s FTSE MIB, was 0.92% (delayed 10 minutes).

Shares in the Asian Pacific markets closed mixed.

- Japan’s Nikkei 225, -1.16%

- China’s Shanghai Composite Index, -0.61%

- Hong Kong’s Hang Seng index, +1.25%

- Australia S&P/ASX index, -0.50%

Looking at the US debt market, yields are higher:

- 2-year yield 4.5 to 3%, +1.6 basis points. At this time yesterday, the yield was at 4.50%

- 5-year yield 4.161%, -0.2 per basis points. At this time yesterday, the yield was at 4.152%

- 10-year yield 4.225%, -1.6 basis points at this time yesterday, the yield was at 4.229%

- 30-year yield 4.426% -2.4 basis points at this time yesterday, the yield was at 4.441%

Looking at the treasury yield curve ):

- The 2-10 year spread is at -29.8 basis points. At this time yesterday, the spread was at -27.1 basis points.

- The 2-30 year spread is -9.8 basis points. At this time yesterday, the spread was at -5.6 basis points

This article was written by Greg Michalowski at www.forexlive.com.

Source link