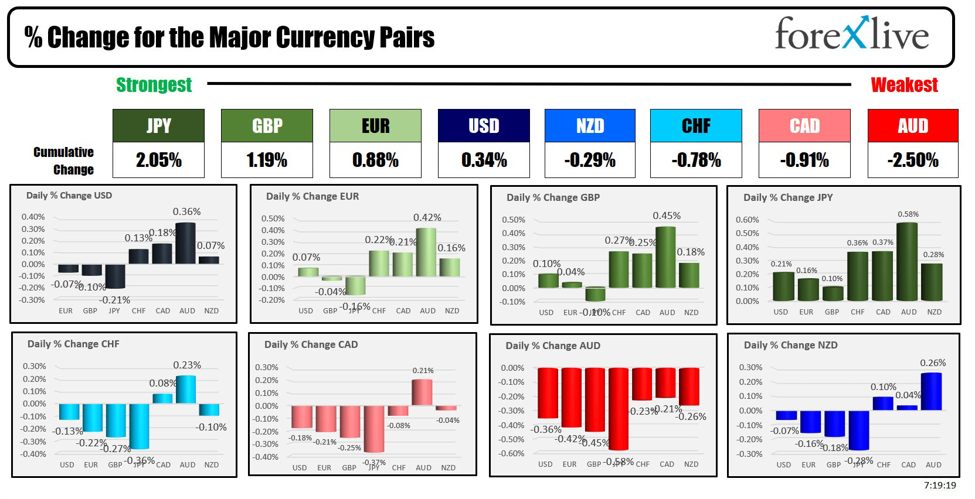

As the North American session begins the JPY is the strongest and the AUD is the weakest. The USD is in the middle of the table with gains vs the commodity currencies (AUD, CAD and NZD) and CHF, and losses vs the EUR, GBP and JPY.

There was a number of comments from bankers overnight.

In the US, Feds Musalem, Williams and Kugler spoke or gave intereviews with the tilt toward recalibration of rates:

- St. Louis Fed President Alberto Musalem, in a speech at a Money Marketeers of New York University Inc. event, suggested that more rate cuts are likely given the economic outlook, though he did not specify their timing or size. He emphasized that the costs of easing too much outweigh those of easing too little. Musalem supported the recent 50 basis point rate cut, noting that policy patience has benefited the Fed. He expects inflation to continue abating and converge to 2% in the coming quarters, while financial conditions remain supportive of growth. Despite a strong September jobs report, he maintained that the current policy path is appropriate and sees no emergency in the labor market. Musalem also noted that inflation risks still exist, though they are not high.

- Federal Reserve Bank of New York President John Williams stated that it will be appropriate for the central bank to reduce interest rates “over time” following September’s 50 bp rate cut. Williams was speaking with the Financial Times. His remarks align with Federal Reserve Chair Jerome Powell, who last week indicated the bank would likely stick with smaller, quarter-point cuts moving forward, emphasizing a cautious approach. Williams added that current monetary policy is well-positioned, with a favorable economic outlook and inflation trending back to 2%.

- Federal Reserve Governor Adriana Kugler stated that while the U.S. job market is beginning to cool, it remains resilient, and the Fed aims to avoid a significant weakening of the labor market. Speaking at a European Central Bank Conference, Kugler welcomed the lower unemployment figures from Friday’s jobs report and emphasized the importance of preventing a drastic slowdown that could cause unnecessary hardship. She noted that several indicators suggest the labor market is returning to pre-pandemic levels but stressed the need for balance in this cooling process.

From the ECB members the theme was :

- ECB Executive Board member Frank Elderson stated that the European Central Bank will continue to gradually ease its restrictive monetary stance if inflation projections, which anticipate reaching the 2% target by the second half of 2025, are confirmed. He mentioned that the ECB will approach its October meeting with an open mind, particularly as downside risks to growth appear to be materializing. Elderson noted that recent data showed these risks and may affect inflation forecasts. The pace of easing will remain flexible, driven by economic growth and inflation data, especially since recent figures have not aligned with the ECB’s expectations.

- Bank of Portugal Governor Mario Centeno noted that inflation in the Euro Area has converged toward its target. He also stated that the easing cycle will proceed faster than initially anticipated in June, with the process of lowering rates already underway

- ECB’s Vasle stated that while inflation risks are easing, uncertainty remains. He mentioned that an interest rate cut in October is an option, but this does not necessarily imply another cut in December.

- ECBs Nagel kept things simple, saying he is open to an October rate cut.

The Reserve Bank of Australia released its meeting minutes from the September meeting, and discussed potential scenarios for both raising and lowering interest rates, given the uncertainty of the economic outlook. Members agreed that the current cash rate best balanced risks to inflation and the labor market, but acknowledged future financial conditions could require tighter or looser policies. The Board remains vigilant to upside inflation risks, with underlying inflation still too high. Policy may be tightened if current conditions are insufficient to bring inflation to target or eased if the economy weakens more than expected. The Board emphasized that policy will remain restrictive until there is confidence that inflation is moving sustainably toward its target range. Risks around Australia’s exports have shifted downward, and while many households face financial pressure, most are still able to service loans. The Term Funding Facility was also reviewed as a potential tool for unconventional monetary policy. Overall, the minutes reflect a cautious and hawkish stance, with a focus on inflation control.

- Reserve Bank of Australia Deputy Governor Andrew Hauser emphasized the need for the RBA to remain firm in its efforts to combat inflation, noting there is no sign of an imminent rate cut. He highlighted that while U.S. inflation is nearing its target, Australia lags behind, with inflation remaining persistent. Hauser expects core inflation to eventually reach the target, but acknowledged that lowering inflation remains a challenging and ongoing task for the central bank.

Meanwhile, in New Zealand the RBNZ will announce its rate decision at 9 PM ET today with the expectations for the RBNZ to cut rates by 50 basis points to 4.75%. The central bank did kickstart its decline in rates at the last meeting with a 25 basis point cut. .

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down $1.74 or -2.26% at $75.40. At this time yesterday, the price was at $75.53

- Gold is trading up $7.14 or 0.27% at $2649.79. At this time yesterday, the price was $2648.74

- Silver is trading down -$0.32 or -1.01% and $31.33. At this time yesterday, the price is at $31.67

- Bitcoin is trading lower than this time yesterday at $62,583. At this time yesterday, the price was at $63,049

- Ethereum is trading lower than this time yesterday at $2437.00. At this time yesterday, the price was at $2468.70

In the premarket, the snapshot of the major indices trading higher after yesterday’s declines.

- Dow Industrial Average futures are implying gain of 61.76 points. Yesterday, the index down -398.51 points or -0.94% at 41954.24

- S&P futures are implying a gain of 23.81 points. Yesterday, the index fell -55.13 points or -0.96% at 5695.94

- Nasdaq futures are implying a gain of 100.01 points. Yesterday, the index -213.95.or -1.18% at 17923.90

Yesterday, the small-cap Russell 2000 rose 32.65 points or 1.50% at 2212.79

European stock indices are trading lower:

- German DAX, -0.13%

- France CAC, -0.53%

- UK FTSE 100, -1.10%

- Spain’s Ibex, -0.27%

- Italy’s FTSE MIB, -0.05% (delayed by 10 minutes)

Shares in Asian Pacific session were mostly lower as China returned back from the Golden week holiday:

- Japan’s Nikkei 225, -1.00%

- China’s Shanghai Composite Index, +4.59%

- Hong Kong’s Hang Seng index, -9.41%

- Australia S&P/ASX index, -0.35%

Looking at the US debt market, yields are higher in the yield curve is little changed

- 2-year yield 3.972%, -3.1 basis points. At this time yesterday, the yield was at 4.007%

- 5-year yield 3.865%, -0.3 basis points. At this time yesterday, the yield was at 3.872%

- 10-year yield 4.035%, +0.9 basis points. At this time yesterday, the yield was at 4.017%

- 30-year yield 4.321%, +1.8 basis points. At this time yesterday, the yield was at 4.287%

Looking at the treasury yield curve it is steeper:

- The 2-10 year spread is at +5.8 basis points. At this time yesterday, the yield spread was +0.8 basis points.

- The 2-30 year spread is at +34.5 basis points. At this time yesterday, the yield spread was +27.5 basis points.

In the European debt market, the 10 year yields are little changed:

This article was written by Greg Michalowski at www.forexlive.com.

Source link