–

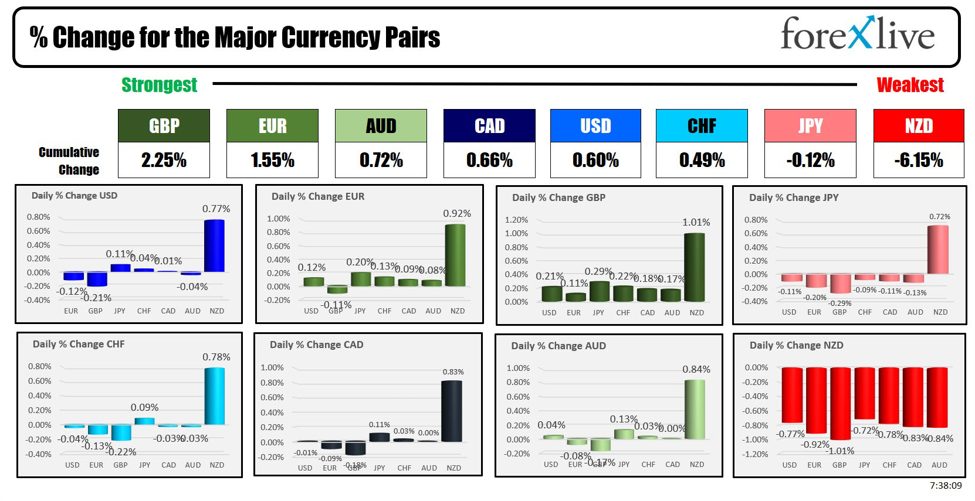

As the North American session begins, the GBP is the strongest of the major currencies, while the NZD is the weakest. Most of the price reaction today is in the NZD which fell sharply vs all the major currencies after its rate decision.

The Reserve Bank of New Zealand’s kept rates unchanged in what was a more dovish decision. The central bank emphasized that restrictive monetary policy has effectively reduced consumer price inflation, with expectations for headline inflation to fall within the 1-3% target range by the second half of this year. That diverged from the last rate decision which was considered more hawkish.

Despite easing labor market pressures and consistent economic activity, some domestic price pressures persist. Consequently, the Bank maintains a restrictive stance but indicates potential tempering of this restraint over time, aligning with the anticipated decline in inflation pressures.

WestPac’s response?

The market reaction to the Reserve Bank of New Zealand’s rate decision was dovish, surprising many who expected a reiteration of May’s hawkish messages. The final paragraph of the statement suggested that monetary restraint would be tempered over time, reflecting a less hawkish stance.

Additionally, BNZ has adjusted their forecast, now anticipating a rate cut in November instead of February.

It will be another quiet day on the economic front with only wholesale inventories at 10 AM on the schedule along with the weekly cruel inventories at 10:30 AM ET. From an event standpoint, Fed Chair Powell will complete his today trek to Capitol Hill, with his testimony to the House financial services committee. Yesterday, the chairman danced around committing to any course of policy action although he did reiterate that the course for the next rate change would be to the downside. He characterized the risk as two-way and not just skewed toward inflation. He commented on a couple occasions, that the labor market has cooled considerably, but that it remains strong. Nevertheless, he thought employment wasn’t a large contributor to inflationary pressures. The door remains open for a cut in September.

Rates in the US yesterday did move higher but it may have been impacted by the auction calendar this week with the treasury selling 3/10/30-year coupon issues. Yesterday the three year auction was a success on back of solid domestic demand in the US. Today, the treasury will auction off 10 year notes at 1 PM ET. Today, yields are lower. Stocks in the premarket are trading higher led by the NASDAQ and S&P once again. The S&P has closed at a new record for four consecutive days. The NASDAQ index has closed at a new record for five consecutive days.

Also on the schedule today is:

- BOE Mann speaking at 11:30 AM ET

- Fed Gov. Bowman and Goolsby both speak at 2:30 PM ET

- Fed Gov. Lisa Cook scheduled to speak at 7:30 PM ET

A snapshot of the other markets as the North American session begins shows:

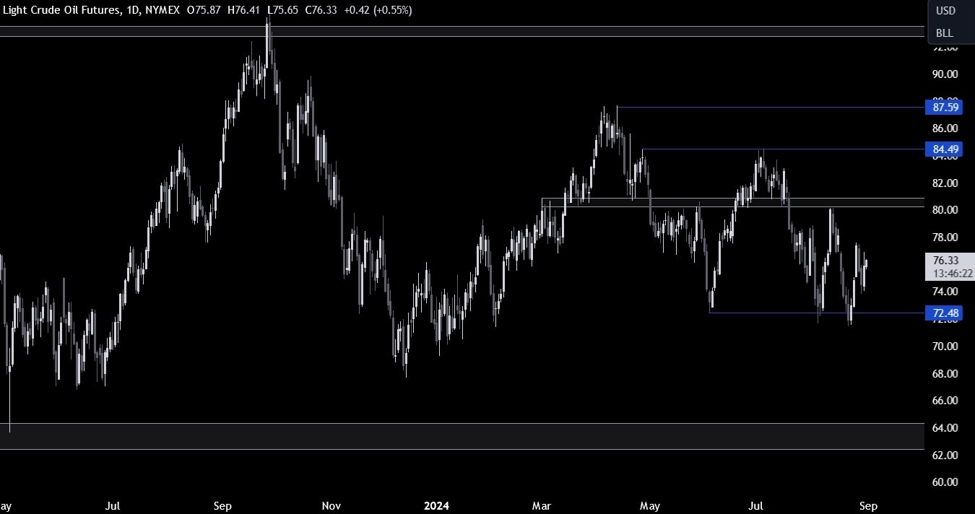

- Crude oil is trading down -$0.14 or -0.18% at $81.26. The price is currently on pace for its fourth consecutive down day. At this time yesterday, the price was at $82.05

- Gold is trading up $15 or 0.64% at $2378.40. At this time yesterday, the price was trading at $2360.64

- Silver is trading up $0.25 or 0.84% at $31.02. At this time on yesterday, the price is trading at $31.05

- Bitcoin trading higher at $58,509. At this time yesterday, the price was trading at $57,439

- Ethereum is also trading higher at $ 3,111.90. At this time yesterday, the price was trading at $3081.80

In the premarket, the snapshot of the major indices are trading higher. The S&P and NASDAQ continue their string of record high closing levels. The S&P has closed higher for four consecutive days. The NASDAQ index has closed higher for five consecutive days (working on its sixth today).

- Dow Industrial Average futures are implying a gain of 21.2 points. Yesterday, the Dow Industrial Average fell -52.82 points or -0.13% 39291.98.

- S&P futures are implying a gain of 15.50 points. Yesterday, the S&P index rose 4.11 points or 0.07% at 5576.97 (a new record close).

- Nasdaq futures are implying a gain of 84 points. Yesterday, the index rose 25.55 points or 0.14% at 18429.29 (a new record)

European stock indices are rebounding higher after some recent declines on the political changes:

- German DAX, +0.68%

- France CAC +0.67%

- UK FTSE 100, was 0.62%

- Spain’s Ibex, +0.99%

- Italy’s FTSE MIB, +0.85% (delayed 10 minutes).

Shares in the Asian Pacific markets were mostly lower with the exception of Manzanita which closed at a new high level:

- Japan’s Nikkei 225, +0.61%

- China’s Shanghai Composite Index, -0.68%

- Hong Kong’s Hang Seng index, -0.29%

- Australia S&P/ASX index, -0.16%

Looking at the US debt market, yields are higher

- 2-year yield 4.609%, -4.8 basis points. At this time yesterday, the yield was at 4.641%

- 5-year yield 4.223%, -2.5 basis points.. At this time yesterday, the yield was at 4.255%

- 10-year yield 4.274%, -2.6 basis points. At this time yesterday, the yield was at 4.295%

- 30-year yield 4.468%, -2.7 basis points. At this time yesterday, the yield was at 4.478%

Looking at the treasury yield curve the spreads became more negative from yesterday’s levels at this time:

- The 2-10 year spread is at -33.5 basis points. At this time yesterday, the spread was at -34.5 basis points.

- The 2-30 year spread is at -14.2 basis points. At this time yesterday, the spread was at -16.4 basis points.

In the European debt market, yields are lower in the benchmark 10 year note sector:

This article was written by Greg Michalowski at www.forexlive.com.

Source link