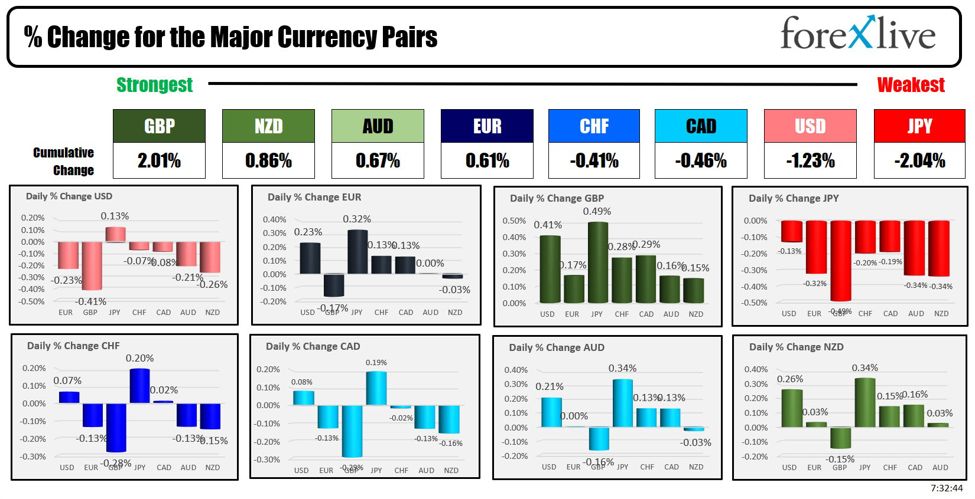

As the North American session begins, the GBP is the strongest and the JPY is the weakest.

Today, the US PPI will be released. Yesterday, the CPI data came in lower than expected on both the headline and the core. The PPI data is expected to show 0.1% MoM/2.3% YoY (vs 2.2% last month) for the headline number and 0.2% MoM/2.5% YoY ex food and energy (vs 2.3% last month).

The University of Michigan consumer sentiment preliminary will be released with the expectation of 68.5. The 1 Year inflation expectations came in at 3.0% last month.

US stocks were all mixed up yesterday with the Nasdaq tumbling (-1.95%) but the small cap Russell 2000 surging (+3.57%). The S&P which also fell (-0.88%), BUT Earnings have started to heat up with the traditional release of the some of the major banks including JP Morgan. All beat on the top and bottom line results but both Wells and JPM stock prices are still lower in pre-market trading. Citigroup earnings will be released at 8 AM ET.

-

Wells Fargo & Co (WFC) 02 2024 (USD). Shares are down -5.59% despite the beat.

- EPS: 1.33 (expected 1.29) – BEAT

- Revenue: 20.69 billion (expected 20.29 billion) – BEAT

- Reaffirms FY24 view

-

JPMorgan Chase & Co (JPM) 02 2024 (USD). The stock is down -1.53% despite the beat.

- EPS: 4.40 (expected 4.19) – BEAT

- Adjusted Revenue: 50.99 billion (expected 42.34 billion) – BEAT

- Managed Revenue: 22.86 billion (expected 22.82 billion) – BEAT

- Investment Banking Revenue: 2.46 billion (expected 2.13 billion) – BEAT

-

Bank of New York Mellon Corp (BK) 02 2024 (USD). Shares are up 0.59%

- Adjusted EPS: 1.51 (expected 1.43) – BEAT

- Revenue: 4.60 billion (expected 4.52 billion) – BEAT

- Cit (C) earnings: Shares are down -2% in premarket trading

- Adjusted earnings-per-share: $1.52 (expected $1.39) – BEAT

- Revenues: $20.1 billion (expected $20.07 billion) – BEAT

After the close yesterday, Federal Reserve Bank of Chicago President Austan Goolsbee expressed satisfaction with the June CPI report, describing it as “excellent” and highlighting significant improvements in shelter inflation. He stated that the current trajectory aligns with the Fed’s goal of 2% inflation and noted that keeping the policy rate steady amid falling inflation equates to tightening policy. Goolsbee emphasized that the economy is not overheating, the labor market is cooling but remains strong, and current financial conditions are restrictive. He also mentioned the need for flexibility in policy decisions and the importance of determining the appropriate timing for rate cuts.

In the US debt market, yields are higher with gains of about 1-2basis points across the curve. Yesterday the 30 year bond auction was less than stellar, but the three and 10 year note options on Tuesday and Wednesday were met with strong demand. The yield curve has continued its move toward flattening (from negative) with the 2-30 year spread up to -8.4 basis points.

The USDJPY today is up modestly after the sharp fall yesterday helped by the CPI and presumed intervention by the Bank of Japan. The price action was about 420 pips yesterday, but the price did rebound into the close. In the Asian session there was another move lower (down to 157.74 from ner 159.00), but the price has rebounded back higher and trades at 158.75 currently. The 200 bar MA on the 4 hour chart is just below at 158.68 which will be eyed as a barometer for buyers and sellers today.

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading higher by $0.80 or 0.97% at $83.42. At this time yesterday, the price was at $82.10

- Gold is trading down $-12.63 or -0.53% at $2403. At this time yesterday, the price was trading at $2381

- Silver is trading down $0.71 or -2.26% at $30.73. At this time on yesterday, the price is trading at $30.89

- Bitcoin trading lower at $57,353. At this time yesterday, the price was trading at $58,788

- Ethereum is also trading lower at $3076.40. At this time yesterday, the price was trading at $3148.40

In the premarket, the snapshot of the major indices are trading next. The S&P and NASDAQ snapped their string of record-high closing levels yesterday. The S&P snapped its six consecutive days of record closes, while the NASDAQ index halted its seven consecutive days of record levels.

- Dow Industrial Average futures are implying a gain of 74 points. Yesterday, the Dow Industrial Average rose 32.39 points or 0.08% at 39753.76.

- S&P futures are implying a gain of 3.96 points. Yesterday, the S&P index a 49.37 points or -0.88% at 5584.55

- Nasdaq futures are implying a decline of -1.83 points. Yesterday, the index tumbled -364.04 points or -1.95% at 18283.41

European stock indices are trading higher :

- German DAX, 0.37%

- France CAC +0.77%

- UK FTSE 100, + 0.27%

- Spain’s Ibex, +0.54%

- Italy’s FTSE MIB, +0.44% (delayed 10 minutes).

Shares in the Asian Pacific markets closed mixed. The Japan’s Nikkei 225 index 225 fell off its record-high closing level from Thursday straight

- Japan’s Nikkei 225, -2.45%

- China’s Shanghai Composite Index, +0.3%

- Hong Kong’s Hang Seng index, +2.59%

- Australia S&P/ASX index, +0.88%

Looking at the US debt market, yields are modestly higher ahead of the PPI data

- 2-year yield 4.501%, -0.5 basis points. At this time yesterday, the yield was at 4.636%

- 5-year yield 4.137%, +1.4 basis points.. At this time yesterday, the yield was at 4.247%

- 10-year yield 4.208%, +1.5 basis points at this time yesterday, the yield was at 4.293%

- 30-year yield 4.419%, +1.5 basis points. At this time yesterday, the yield was at 4.479%

Looking at the treasury yield curve the negative curve is getting less negative with the 2 – 30 year spread down to -8.4 basis points

- The 2-10 year spread is at -29.4 basis points. At this time yesterday, the spread was at -34.5 basis points.

- The 2-30 year spread is at -8.4 basis points. At this time yesterday, the spread was at -15.7 basis points.

In the European debt market, yields are higher in the benchmark 10 year note sector:

This article was written by Greg Michalowski at www.forexlive.com.

Source link