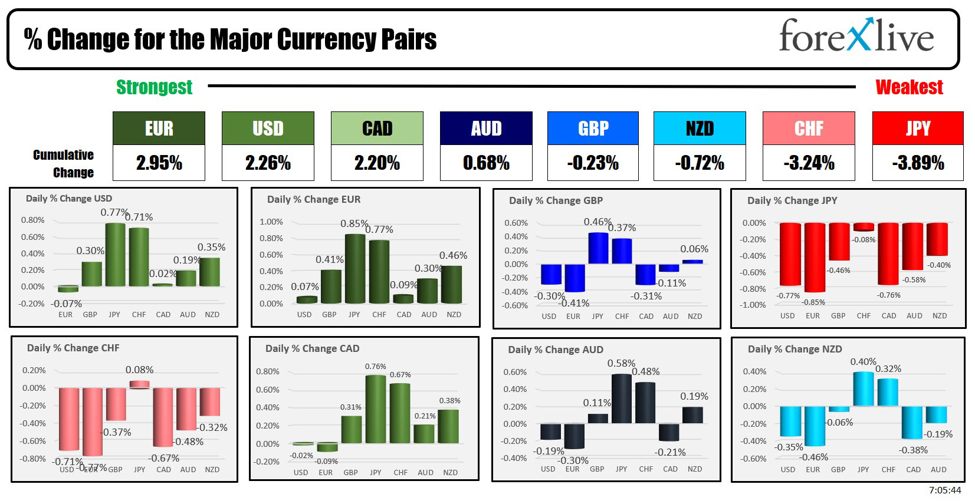

A day after the USD was the weakest of the major currencies, the greenback is one of the strongest of the major currencies. The EURUSD is the only currency that the USD is weaker against in the morning snapshot. The USD is unchanged vs. the CAD as well. The JPY and the CHF are the weakest of the major currencies.

The USD moved lower yesterday after weaker data from consumer confidence and the Richmond Fed surveys. US yields which were higher at this time yesterday, started to move lower with the 2-year down -3.8 bps at the close and the 10 year -0.4 bps. Today, yields are back higher.

In a sign of labor weakness, the WSJ Timiraos dropped a tweet from the details of the Conference Board consumer confidence showing the net share of respondents who say jobs are plentiful less those who say jobs are hard to get. The levels are at 2017 levels and has tumbled over the last 6 months. We do see the latest in the initial jobless and continuing claims tomorrow. Last week, the initial jobless claims dip to 219K which is still low historically.

The Fed cut rates last week as they recalibrate rates to the current environment with inflation lower and the threat to higher unemployment rising (although they see the end of 2025 Unemployment rate at 4.4%, but that may be because they see their actions working). The expectations of a 50 bp cut has tilted higher over the last 24 hours to 58% from 50% at this time yesterday.

In the UK, Bank of England (BOE) policymaker Megan Greene emphasized the importance of taking a cautious and gradual approach to easing monetary policy, stressing the need for data to confirm that the risk of persistent inflation is subsiding. While wage growth has decreased, it remains higher than BOE models can fully explain. Greene also noted that risks to economic activity lean to the upside, which could imply a higher long-term neutral rate. Her remarks reaffirm the BOE’s stance from the previous week. Despite the current pause, traders anticipate a rate cut in November, with a roughly 86% chance of a 25 basis point reduction priced in by the OIS market

The economic calendar was light in Europe today, and is light in the US and Canada as well. At 10 AM, the New Home sales in August will be released with the expectations at 0.700M vs 0.739M last month. The weekly EIA oil inventories will be released:

- Crude oil, -1.354M est

- Gasoline, -0.021M est

- Distillates, -1.637M est.

The private API data late yesterday showed larger than expected drawdowns:

A snapshot of the other markets as the North American session begins shows:

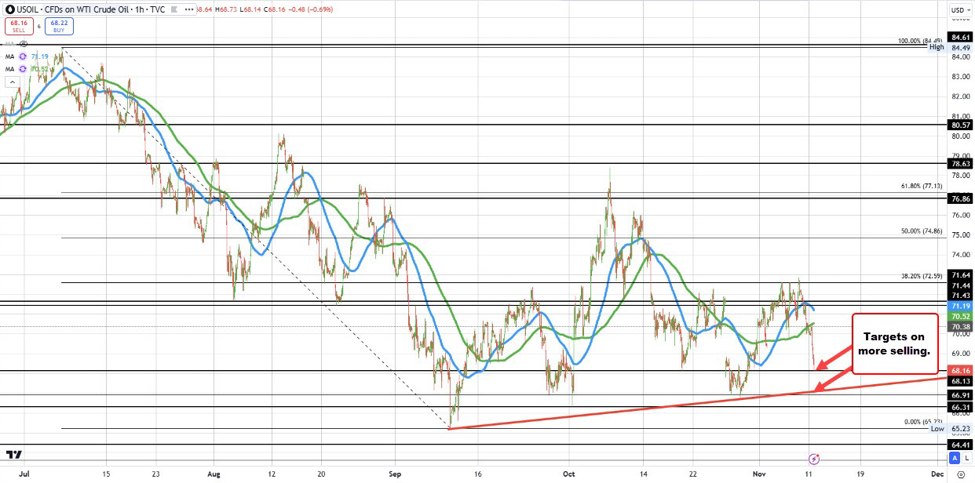

- Crude oil is trading down -$0.91 and $70.66. At this time yesterday, the price was at $71.97

- Gold is trading down -$1.50 or -0.06% at $2655.39. At this time yesterday, the price was $2625.90

- Silver is trading down -$0.23 or -0.75% and $31.84. At this time yesterday, the price is at $30.86

- Bitcoin is trading at $63,713. At this time yesterday, the price was at $63,522

- Ethereum is trading at $2619.30. At this time yesterday, the price was at $2639.40

In the premarket, the snapshot of the major indices trading marginally higher after the S&P and Dow industrial average closed at record levels again yesterday:

- Dow Industrial Average futures are implying a gain of 16.78 point. Yesterday, the index rose 83.57 points or +0.20% at 42208.22

- S&P futures are implying a decline of -2.18 points. Yesterday, the price rose 14.36 points or 0.25% at 5732.93

- Nasdaq futures are implying a decline of-42.59 points. Yesterday, the index rose 100.25 points or 0.56% at 18074.52

Yesterday, the small-cap Russell 2000 rose 3.712 points or 0.17% and 2223.99

European stock indices are trading mixed

- German DAX, -0.39%

- France CAC, -0.2%

- UK FTSE 100, +0.31%

- Spain’s Ibex, +0.02%

- Italy’s FTSE MIB, +0.16% (delayed 10 minutes).

Shares in the Asian Pacific markets China and Hong Kong intended to move higher after yesterday’s over 4% gains China stimulus initiatives:

- Japan’s Nikkei 225, -00.19%

- China’s Shanghai Composite Index, +1.16%

- Hong Kong’s Hang Seng index, +0.68%

- Australia S&P/ASX index, -0.19%

Looking at the US debt market, yields are higher

- 2-year yield 3.540%, +2.1 basis points. at this time yesterday, the yield was at 3.603%

- 5-year yield 3.402%, +2.4 basis points. At this time yesterday, the yield was at 3.539%

- 10-year yield 3.762%, +2.6 basis points. At this time yesterday, the yield is at 3.790%

- 30-year yield 4.111%, +2 point basis points..2 At this time yesterday, the yield is at 4.139%

Looking at the treasury yield curve, is similar to yesterday’s levels at this time

- The 2-10 year spread is at + 21.9 basis points. At this time yesterday, the yield spread was +18.8 basis points.

- The 2-30 year spread is at + 57.0 basis points. At this time yesterday, the yield spread was +53.4 basis points.

In the European debt market, the 10 year yields are mostly higher:

This article was written by Greg Michalowski at www.forexlive.com.

Source link