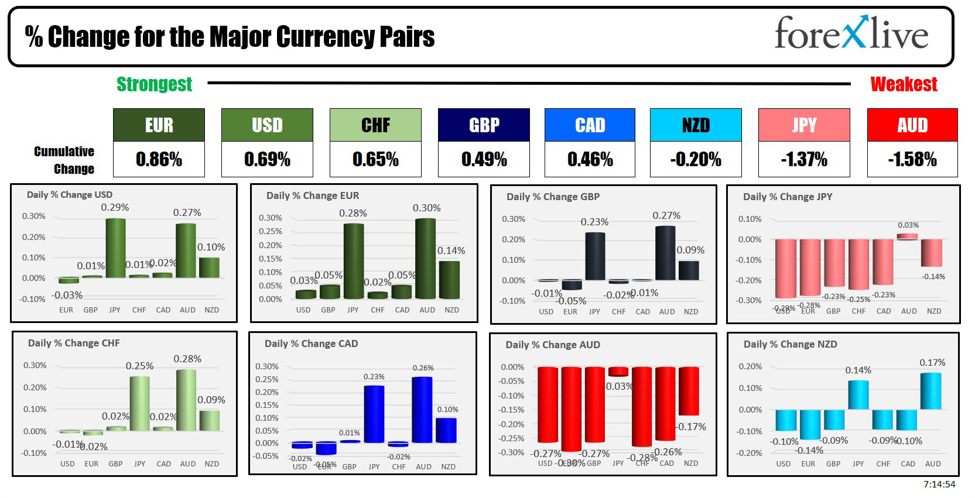

The EUR is the strongest and the AUD is the weakest as the North American session begins.The ECB meets on Thursday with the expectation of no change.

The USD is modestly higher ahead of the US retail sales, import/export prices, Business inventories and NAHB housing starts. Canada releases their key CPI data ahead of their interest rate decision next week. Fed’s Governor Kugler speaks at 2:45 PM ET. The trading ranges for currency pairs are very modest with the EURUSD (21 pips), GBPUSD (21 pips), USDCHF (16 pips), USDCAD (20 pips) and NZDUSD (29 pips) all below 30 pips from the low to the high. That is not a lot of price action.

The USDJPY does have an 82 pip trading range (the largest of the majors) after the break below the 61.8% of the last move higher late yesterday failed. Sellers turned to buyers and pushed the price back to the 200 hour MA at 158.733 before stalling (see green line on the chart below).

After the US session yesterday, Federal Reserve Bank of San Francisco President Mary Daly indicated a potential rate cut soon, emphasizing growing confidence in controlling inflation towards 2%, normalization of policy, a slowing US economy, and nearing the Fed’s goals. There are some analysts/economists calling for a July cut but the consensus is still for September and then December.

Earnings released this morning showed:

- State Street Corp (STT) Q2 2024 (USD): EPS 2.10 (exp. 2.03) BEAT, Revenue 3.19B (exp. 3.10B) BEAT

- Charles Schwab Corp (SCHW) Q2 2024 (USD): adj. EPS 0.73 (exp. 0.72) BEAT, Revenue 4.69B (exp. 4.68B) BEAT

- Morgan Stanley (MS) Q2 2024 (USD): EPS 1.82 (exp. 1.65) BEAT, Revenue 15.02B (exp. 14.30B) BEAT; reauthorized multi-year repurchase program up to USD 20B. Shares are trading down -2.76% despite the beat.

- Bank of America Corp (BAC) Q2 2024 (USD): EPS 0.83 (exp. 0.80) BEAT, Revenue 25.4B (exp. 25.22B) BEAT, Net interest income FTE 13.86B (exp. 13.81B) BEAT, Trading revenue ex DVA 4.68B (exp. 4.53B) BEAT. Shares are up around 2% in premarket trading

- PNC Financial Services Group Inc (PNC) Q2 2024 (USD): Diluted EPS 3.39 (exp. 2.98) BEAT, Revenue 5.41B (exp. 5.41B) MET

- UnitedHealth Group Inc (UNH) Q2 2024 (USD): adj. EPS 6.80 (exp. 6.66) BEAT, Revenue 98.9B (exp. 98.84B) BEAT, FY EPS view 27.50-28.00 (exp. 27.59) IN LINE. Shares are trading down -1.62% in premarket trading

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading trading down -$1.38 at $80.53 helped by hopes of a Trump victory which would open up the spigots. At this time yesterday, the price was at $82.14

- Gold is trading up $17.50 or 0.73% at $2439.20. At this time yesterday, the price was trading at $2419.34

- Silver is trading up $0.15 or 0.51% at $30.81. At this time yesterday, the price is trading at $30.77

- Bitcoin trading at $63,782. At this time yesterday, the price was trading at $62,549

- Ethereum is also trading sharply higher at $3418.40. At this time yesterday, the price was trading at $3342

In the premarket, the snapshot of the major indices are trading marginally higher. Yesterday, the Dow Industrial Average closed at a record high level for the first time since May 17. The S&P index closed just below its record high of 5633.92 (closed at $5631.21). The Nasdaq record high close from last Wednesday is at 18647.45.

- Dow Industrial Average futures are implying a gain of 31.12 points. Yesterday, the Dow Industrial Average rose 210.82 points or 0.53% at 40,211.73

- S&P futures are implying a gain of 9.03 points. Yesterday, the S&P index closed higher by 15.87 points or 0.28% at 5631.21.

- Nasdaq futures are implying a gain of 37.21 points. Yesterday, the index closed higher by 74.12 points or 0.40% at 18472.57

European stock indices are trading lower:

- German DAX, -0.58%

- France CAC -0.1%

- UK FTSE 100, -0.50%

- Spain’s Ibex, -0.85%

- Italy’s FTSE MIB, -0.35% (delayed 10 minutes).

Shares in the Asian Pacific markets closed mixed.

- Japan’s Nikkei 225, +.20%

- China’s Shanghai Composite Index, +0.08%

- Hong Kong’s Hang Seng index, -1.60%

- Australia S&P/ASX index, -0.23%

Looking at the US debt market, yields are higher with a steeper your curve:

- 2-year yield 4.419%, -3.3 basis points. At this time Friday, the yield was at 4.459%

- 5-year yield 4.082%, -4.9 basis points. At this time Friday, the yield was at 4.135%

- 10-year yield 4.175%, -5.4 basis points. At this time Friday, the yield was at 4.237%

- 30-year yield 4.403%, -5.1 basis points. At this time Friday, the yield was at 4.467%

Looking at the treasury yield curve the 2 – 30 year spread turned positive yesterday. It is back into negative territory today. The 2– 10 year spread” price level since January 23 at -22.7 basis points. Today, the yield spreads are marginally more negative:

- The 2-10 year spread is at -24.6 basis points. At this time yesterday, the spread was at -22.5 basis points.

- The 2-30 year spread is positive -1.8 basis points. At this time yesterday, the spread was at +0.05 basis points.

In the European debt market, yields are lower in the benchmark 10-year note sector:

This article was written by Greg Michalowski at www.forexlive.com.

Source link