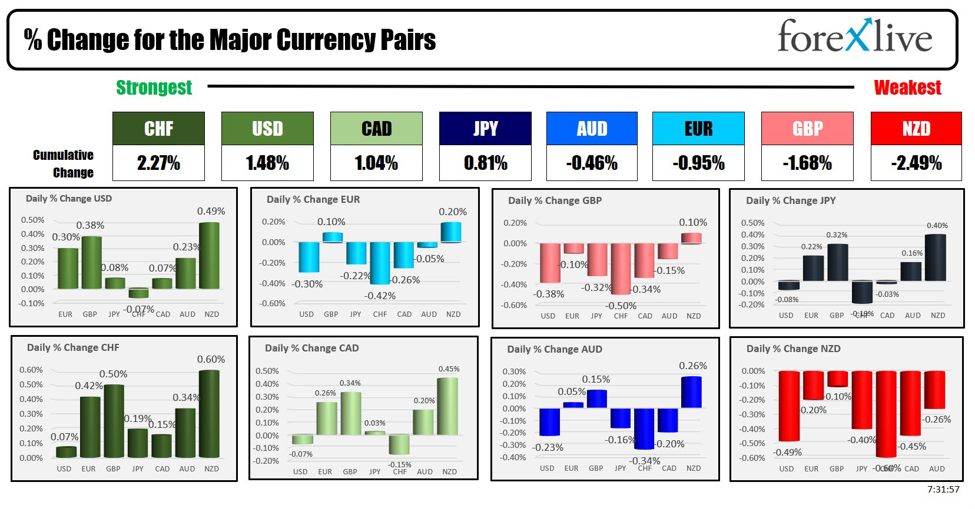

As the North American session begins, the CHF is the strongest and the NZD is the weakest. The USD is mostly stronger to start the US session.

Overnight, the Bank of Japan (BOJ) decided to maintain its overnight rates at 0.1% and voted to reduce JGB (Japanese Government Bond) purchases to allow long-term interest rates to move more freely. The decision on JGB purchases was made by an 8-1 vote, with BOJ Board Member Nakamura dissenting. Nakamura argued that the reduction should be decided after reassessing economic activity and prices in the July 2024 Outlook Report.

The BOJ plans to finalize the specific bond buying reduction plan for the next 1-2 years at its next policy meeting. The BOJ currently aims to purchase about 6 trillion yen ($38.5 billion) in bonds per month, and has informed the market of plans to purchase between 4.8 trillion yen and 7 trillion yen of bonds per month.

The bank highlighted that uncertainties surrounding domestic economic and financial developments remain high. Japan’s economy has recovered moderately, although some weaknesses have been observed, particularly in industrial output due to production and shipment suspensions at some automakers.

Inflation expectations have risen moderately, and private consumption has shown resilience despite the impact of price increases and continued suppression of auto sales. The BOJ emphasized the need to pay close attention to financial and foreign exchange market developments. Underlying CPI inflation is expected to rise gradually.

The BOJ will hold a meeting with bond market participants to discuss the policy decision and its implications for the market.

Later, BOJ Governor Kazuo Ueda said that plans to reduce JGB purchases predictably to allow long-term yields to form more freely, starting after the July meeting. The cut will be substantial, with the amount determined after market discussions. He emphasized monitoring economic uncertainties, financial and FX markets, and said rate adjustments will depend on inflation reaching the 2% target. Ueda indicated no immediate rush to hike rates further, focusing instead on evaluating FX movements and their impact on prices.

The USDJPY initially moved higher, but then gave back the gains and is little changed vs the USD currently (and mixed vs the other currencies with an upward bias).

On the economic calendar of releases in the NA session:

- 8:30 AM ET: Canada Manufacturing Sales m/m (previous: -2.1%, expected: 1.3%)

- 8:30 AM ET: Canada Wholesale Sales m/m (previous: -1.1%, expected: 2.6%)

- 8:30 AM ET: US Import Prices m/m (previous: 0.9%, expected: 0.0%)

- 10:00 AM ET: US Prelim UoM Consumer Sentiment (previous: 69.1, expected: 72.0), Current conditions est 71.0 vs 69.6 last. Expectations 70.0 est vs 68.8 last.

- 10:00 AM ET: US Prelim UoM Inflation Expectations 1 year. Last month 3.3%. 5 year last month 3.0%

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading up $0.35 at $78.97. At this time yesterday, the price was at $77.76

- Gold is trading up $30.74 or 1.34% at $2331.82. At this time yesterday, the price was at $2308.10

- Silver is trading up $0.29 or 1.02% at $29.25. At this time yesterday, the price was trading at $29.10

- Bitcoin trades modestly higher at $67,051. At this time yesterday, the price was trading up at $67,774

- Ethereum is also trading modestly higher $3516.04. At this time yesterday, the price was trading at $3498.80

In the premarket, the snapshot of the major indices are trading lower.

- Dow Industrial Average futures are implying a loss of -240 points. Yesterday, the Dow Industrial Average fell -65.13 points or -0.17% at 38647.09

- S&P futures are implying a loss of -17.74 points. Yesterday, the S&P index closed at another record level with a gain of 12.73 points or 0.23% at 5433.75

- Nasdaq futures are implying a -16.17 points. Yesterday, NASDAQ index also closed at a record level after a gain of 59.12 points or 0.34% at 17667.56

European stock indices are trading lower again today in the US morning snapshot. For the week, the major indices are all sharply lower as political concerns continue to weigh on investor sentiment. :

- German DAX, -1.34%. For the week the index is down -2.87%

- France CAC -2.38%. For the week -5.96%

- UK FTSE 100, -0.21%. For the week -1.16%

- Spain’s Ibex, -1.09%. For the week -4.03%

- Italy’s FTSE MIB, -2.90 (delayed 10 minutes).. For the week -5.82%.

Shares in the Asian Pacific markets were mixed:

- Japan’s Nikkei 225, 0.24%

- China’s Shanghai Composite Index, 0.12%

- Hong Kong’s Hang Seng index, -0.94%

- Australia S&P/ASX index, -0.33%

Looking at the US debt market, yields are lower.

- 2-year yield 4.666%, -2.2 basis points. At this time yesterday, the yield was at 4.753%

- 5-year yield 4.203%, -3.2 basis points. At this time yesterday, the yield was at 4.314%

- 10-year yield 4.197%, -4.2 basis points. At this time yesterday, the yield was at 4.318%

- 30-year yield 4.341% -6.0 basis points. At this time yesterday, the yield was at 4.481%

Looking at the treasury yield curve the spreads are moving more negative

- The 2-10 year spread is at -46.8 basis points. At this time Friday, the spread was at -43.8 basis points.

- The 2-30 year spread is at -32.5 basis points. At this time Friday, the spread was at -27.2 basis points.

European 10 year yields are down sharply

This article was written by Greg Michalowski at www.forexlive.com.

Source link