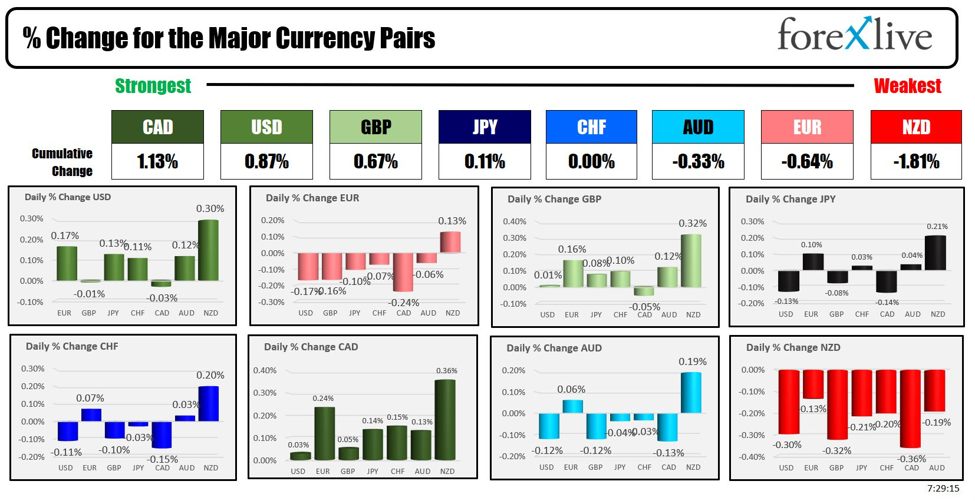

As the North American session begins, the CAD is the strongest and the NZD is the weakest. The USD is mostly stronger – but modestly – with gains vs all the major currencies with the exception of the CAD and GBP (which are virtually unchanged).

Overnight, ECB core CPI came in stronger at 2.9% versus 2.8% expected (unchanged from last month). The headline data was as expected however.

There was plenty of ECB speak overnight. Some of the highlights:

- Wunsch said there is room for second breakup barring any major negative surprises. Most are expecting 1 to 2 by the end of the year.

- Lane said that June inflation data seems in line with our assessment, Buck commented that service inflation remains essential and that the ECB needed to take a bit of time to assess inflation.

- di Guindos said we are not following a predetermined path on interest rates and that uncertainty remains high.

- Muller agreed that we can probably cut rates again before year end, but should not rush to do so and the patient with further rate cuts.

- Centeno said that every meeting is open for us to make a decision but said that we were to be prudent on rates. He did add that there is confidence that inflation will hit 2%percent target next year.

- Vasle at that we can cut rates further things go as expected, but need more data to confirm inflation trajectory.

In Australia, ING overnight said that they are now expecting a rate hike at the next RBA interest rate decision. Last week the Australia CPI data rose by 4.1% versus 3.8% prior (click here for the full story).

There was some Fed officials speaking overnight. New York Fed President John Williams expressed confidence that the Federal Reserve is on track to achieve its 2% inflation target sustainably. He noted that he continues to see moderating price pressures, reinforcing his belief in the Fed’s current path. Williams made these remarks in a video for a Bank for International Settlements conference.

In other chatter, Chicago Fed President Austan Goolsbee stated that current interest rates are restrictive, which could become problematic if maintained for too long. He highlighted emerging warning signs in the job market and emphasized the importance of monitoring jobs reports and price data. Goolsbee noted a series of improved inflation readings in the U.S., suggesting a potential path back towards the 2% inflation target. He indicated that if inflation normalizes, interest rates will also return to more typical levels.Today, Powell is speaking at 1330 GMT / 0930 US Eastern time at the ECB forum in Sintra. He will be joined by ECB Pres. Lagarde on the panel. Period the job to job report will add to the employment data ahead of the BLS job report on Friday. The expectations are for job openings to come in at 7.96 million down from 8.06 million last month. Looking ahead to Friday, the non-farm payroll is expected to add 195,000 jobs versus 272,000 last month.

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading up $0.71 or 0.84% at $84.07. At this time yesterday, the price was at $81.96

- Gold is trading down $9.98 or -0.43% at $2321.69. At this time yesterday, the price was trading at $2338

- Silver is trading down $0.17 or -0.59% at $29.27. At this time on yesterday, the price is trading at $29.29

- Bitcoin trades at $62,680. At this time yesterday, the price was trading up at $62,600

- Ethereum is also trading at $3448.10. At this time yesterday, the price was trading at $3458.90

In the premarket, the snapshot of the major indices are trading lower in premarket trading after gains yesterday. In the second act closed at a record level.

- Dow Industrial Average futures are implying a loss of -143 points. Yesterday, the Dow Industrial Average rose 50.66 points or 0.13% at 39169.53.

- S&P futures are implying a decline of -24.34 points. Yesterday, the S&P index rose 14.61 points or 0.27% at 5475.10.

- Nasdaq futures are implying a decline of -119.10 points. Yesterday, the NASDAQ index rose 146.70 points or 0.83% at 17879.305

European stock indices are trading lower after rising across the board yesterday:

- German DAX, -1.27%

- France CAC -1.06%

- UK FTSE 100, -0.54%

- Spain’s Ibex, -1.79%

- Italy’s FTSE MIB, -1.23% (delayed 10 minutes)..

Shares in the Asian Pacific markets were mixed

- Japan’s Nikkei 225, +1.12%

- China’s Shanghai Composite Index, +0.08%

- Hong Kong’s Hang Seng index, +0.29%

- Australia S&P/ASX index, -0.42%

Looking at the US debt market, yields are lower.

- 2-year yield 4.747%, -2.5 basis points. At this time yesterday, the yield was at 4.758%

- 5-year yield 4.403%, -3.7 basis points. At this time yesterday, the yield was at 4.392%

- 10-year yield 4.443%, -3.6 basis points. At this time yesterday, the yield was at 4.414%

- 30-year yield 4.609%, -3.4 basis points. At this time yesterday, the yield was at 4.579%

Looking at the treasury yield curve the spreads are continuing to rise and are chipping away at the negative yield curve:

- The 2-10 year spread is at -30.3 basis points. At this time yesterday, the spread was at -34.4 basis points. A week ago, the spread was at -50.6 basis points

- The 2-30 year spread is at -13.8 basis points. At this time yesterday, the spread was at -18.4 basis points. A week ago the spread was at -37.3 basis points

European benchmark 10 year yields are mixed:

This article was written by Greg Michalowski at www.forexlive.com.

Source link