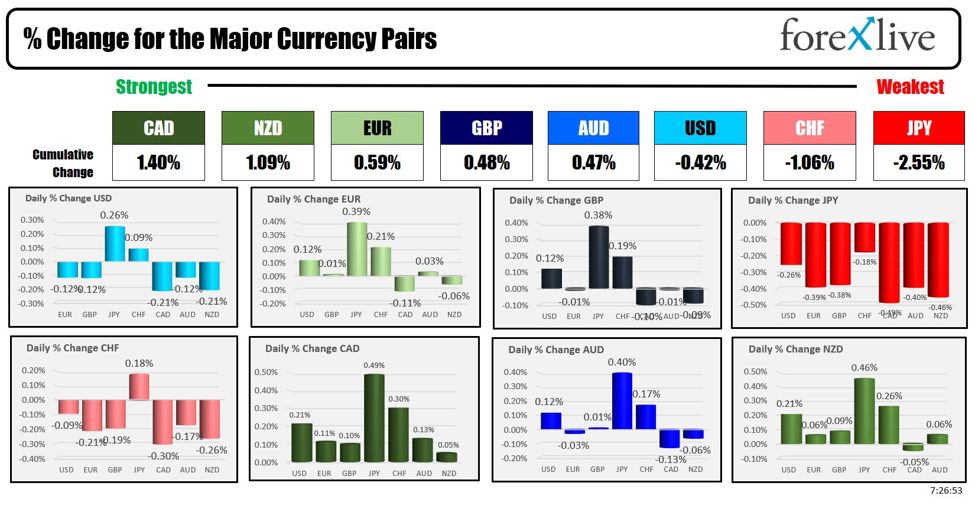

As the North American session begins, the CAD is the strongest and the JPY is the weakest. The USD is mixed to start the day with US stocks marginally higher and yields continuing their run to the upside despite the Fed rate cut of 50 basis points last week to recalibrate rates given the inflation trends. The market is now pricing in a 50/50 chance for 50 basis points in November. The 10-year yield is now up 18 basis points from a September 16 low and working on its 6th straight day higher. Crude oil is higher. Gold is modestly lower after closing at another record level yesterday as tension in the middle east heat up.

In China, officials have announced several measures aimed at stimulating economic growth, with the People’s Bank of China (PBOC) cutting reserve requirements for banks by 50 basis points to unlock more liquidity. To support the struggling property market, the government will reduce mortgage rates on existing loans, while also planning 500 billion yuan ($70.8 billion) in liquidity support for local stocks. These actions follow the PBOC’s recent cut to a short-term repo rate, as officials work to address persistent disinflation and a prolonged downturn in the property market, which is hampering the growth of the world’s second-largest economy. The stock markets in China and Hong Kong each rose over 4%

Overnight Jaime DImon, CEO of JPMorgan Chase, reiterated his concerns about the growing risks of global instability, emphasizing that geopolitics remains the most significant threat to the world economy. Speaking in an interview from India, Dimon warned that geopolitical conditions are worsening with risks from disruptions in energy supply and increasing involvement of other nations in ongoing conflicts. He specifically referenced attacks by Yemen’s Houthi rebel group on crude oil tankers in the Red Sea. Dimon urged the U.S. to prepare for a prolonged conflict between Ukraine and Russia, reinforcing his earlier warning that geopolitical instability poses a greater risk than inflation or a potential U.S. recession. While remaining a long-term optimist, Dimon expressed skepticism about the U.S. economy in the short term, noting that markets are overly optimistic and cautioning against expecting everything to improve quickly.

Dimon has been consistently skeptical about the US economy. So far he has been more the “boy who cried wolf” vs. Nostradamos. However, things like geopolitics are not problems, are not problems until the market wakes up one morning and makes it a problem. With deficits in the US rising and rising and the candidates lining up with promises, promises (Trump is proposing $10T of Tax giveaways. Harris is pigbacking on some of the Trump proposals, but she does propose higher taxes on the wealthy).

It isn’t a problem, until it is a problem.

The Reserve Bank of Australia (RBA) was the latest central bank to announce its policy objective when it left its cash rate unchanged at 4.35% in September 2024, as expected. The central bank noted that current policy remains restrictive and is working as anticipated, but the outlook is still uncertain. Inflation remains above the 2-3% target range, and returning it to target is the RBA’s priority. The bank emphasized that policy will need to stay restrictive until inflation is sustainably moving towards the target. The RBA remains committed to taking necessary actions to control inflation and is keeping options open for future policy moves.RBA Governor Michele Bullock stated that rates will remain on hold for the time being, with no consideration of a rate hike at the recent meeting. She noted that recent data hasn’t materially affected the policy outlook, and while headline inflation may fall within the 2-3% target, underlying inflation progress remains slow. Bullock emphasized that disinflation in other major economies is more advanced than in Australia, and their policy is less restrictive. Although no rate cuts are expected in the near term, the RBA is prepared to adjust in either direction based on data. She also highlighted that even if headline inflation meets the target, it doesn’t necessarily mean inflation is fully under control.Finally, BOJ Governor Kazuo Ueda emphasized the need for timely and appropriate monetary policy without adhering to a fixed schedule, due to uncertainties. He noted that rate hikes could be appropriate if trend inflation aligns with forecasts but stressed that market developments remain unstable. Ueda is closely monitoring the U.S. and global economic outlook and believes Japan can take time to assess market moves. He expects moderate growth in consumption as household incomes rise and sees the impact of wage hikes strengthening. He also remarked on the importance of stable exchange rates and noted that speculative yen positions have largely unwound.

On the economic calendar today:

- Case Shiller Home price data for July is expected to surely 0.4% increase for the month (last month 0.4%) and 5.9% for the year (versus 6.5% last month)

- US consumer confidence for September is expected to rise to 104.0 versus 103.3 last month.

- Fed composite index for September will be released with -19 last month.

Later at 1 PM, the US treasury will auction off 2-year notes.

Fed’s Michelle Bowman is scheduled to speak. Bowman last week became the first central bank governor to dissent against a policy decision favored by the Fed chair since 2005 when she favored a 25 basis point cut

Bank of Canada’s Macklem will be speaking at 1:10 PM today. The USDCAD moved lower yesterday (higher CAD), but bounced later in the day. Today the USDCAD is back down, and looks toward natural support near 1.3500. . The low price yesterday extended to 1.3486 before bouncing higher. The 100-hour moving average and 100-bar moving average on the 4-hour chart are above at 1.3557. Getting above both those levels is needed to increase the buyers confidence going forward technically. Yesterday the price moved away from a cluster of MAs.

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading up up $1.60 or 2.27% at $71.97. At this time yesterday, the price was at $71.15

- Gold is trading down- $2.41 or -0.09% at $2625.90. At this time yesterday, the price was $2623.90

- Silver is trading up $0.20 or 0.65% at $30.86. At this time yesterday, the price is at $30.74

- Bitcoin is trading at $63,522. At this time yesterday, the price was at $63,458

- Ethereum is trading at $2639.40. At this time yesterday, the price was at $2646.50

In the premarket, the snapshot of the major indices trading marginally higher after the S&P and Down industrial average closed at record levels yesterday:

- Dow Industrial Average futures are implying a gain of 35.20 point. Yesterday, the index rose 61.29 points or 0.15% at 42124.65

- S&P futures are implying a gain of 3.68 points. Yesterday, the price rose 16.02 points or 0.28% at 5718.57

- Nasdaq futures are implying a gain of 29.05 points. Yesterday, the index rose 25.95 points or 0.14% at 17974.27

Friday, the small-cap Russell 2000 was lower by -7.607 points or -0.34% at 2220.28

European stock indices are trading mostly higher:

- German DAX, +0.53%

- France CAC, +1.22%

- UK FTSE 100, +0.21%

- Spain’s Ibex, -0.13%

- Italy’s FTSE MIB, +0.49% (delayed 10 minutes).

Shares in the Asian Pacific markets China and Hong Kong stocks soared after announced stimulus measures by China:

- Japan’s Nikkei 225, +0.57%

- China’s Shanghai Composite Index, +4.15%

- Hong Kong’s Hang Seng index, +4.13%

- Australia S&P/ASX index, -0.13%

Looking at the US debt market, yields are mixed with the shorter end higher and the longer lower (flatter yield curve):

- 2-year yield 3.603%, +2.7 basis points at this time yesterday, the yield was at 3.574%

- 5-year yield 3.539%, +4.3 basis points. At this time yesterday, the yield was at 3.501%

- 10-year yield 3.790%, +5.3 basis points. At this time yesterday, the yield is at 3.750%

- 30-year yield 4.139%, +5.7 basis points. At this time yesterday, the yield is at 4.099%

Looking at the treasury yield curve, is similar to yesterday’s levels at this time

- The 2-10 year spread is at +18.8 basis points. At this time yesterday, the yield spread was a 17.9 basis points.

- The 2-30 year spread is at +53.4 basis points. At this time yesterday, the yield spread was +52.6 basis points.

In the European debt market, the 10 year yields are mostly lower:

This article was written by Greg Michalowski at www.forexlive.com.

Source link