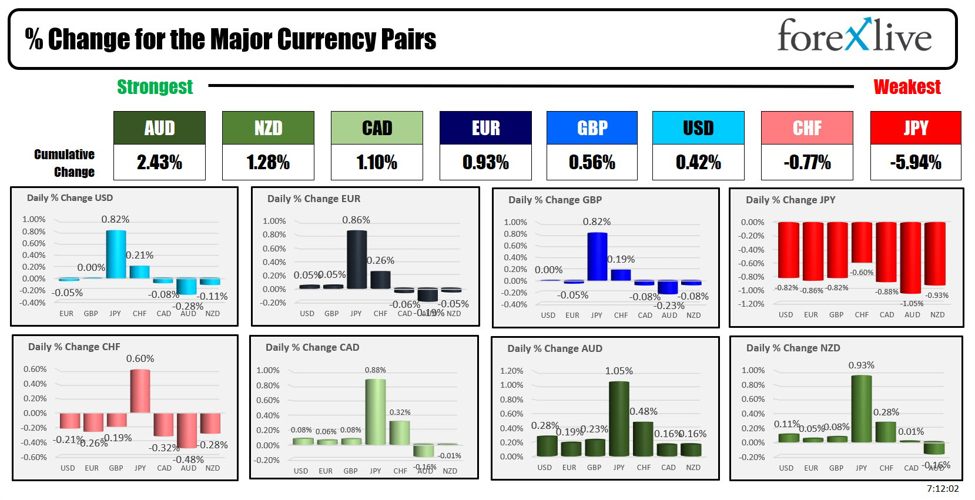

The AUD is the strongest and the JPY is the weakest as the NA session begins. The USD is mixed to start the day.

The newest “day after” is the day after the Iran attack on Isreal. The question now is what, if any, is the response? Will Isreal target more important Iranian strategic sites?

Focus from the US, is a shift in the US response to the attack. Not only did the US help with the the defense from the attack directly, but the White House national security spokesman Jake Sullivan called Iran’s recent attack a “significant escalation” and warned of “severe consequences.” While Sullivan did not provide details on what these consequences might entail, he emphasized that the U.S. will coordinate with Israel to ensure a response. Unlike after Iran’s attack in April, Sullivan refrained from urging Israel to show restraint.

Former Israel prime minister Naftali Bennett last night, using very strong language, said: “This is the greatest opportunity in 50 years to change the face of the Middle East.” He arguing that Israel should go after Iran’s nuclear facilities, in order to “fatally cripple this terrorist regime”.

Buckle in.

Today in the US, ADP will announce the employment projection with expectations of 120K vs 99K last month. The US employment report is out on Friday with the expectation of 144K – around the level from last month.

The weekly oil inventory data will be released at 10:30 AM ET.

Stay informed on Forexlive with today’s Fed speaker schedule featuring Hammack, Musalem, Bowman, and Barkin discussing research, policy, and economic outlook.

Next week, the RBNZ meets and the expectations are coming in for a 50 bp cut:

Yesterday BNZ called for a 50 bp cut as well.

- According to the latest analysis from the Westpac NZ Economics Team, inflation appears well-contained at around 2%, while the broader economy remains sluggish.

- The rationale for maintaining rates significantly above the neutral level is increasingly tenuous. With global central banks reacting to similar economic dynamics and adjusting policy, the Reserve Bank of New Zealand is likely to follow suit, particularly considering the extended gap in its meeting schedule from November to February.

ECBs Elderson said that there is no room for inflation complacency.

In Japan, BOJ Ueda told PM Ishiba that Japan’s economy is extraordinarily easy environment, the Greek” nation between Bank of Japan and government. Ueda also told the prime minister that the Bank of Japan will adjust the degree of monetary easing if the expected outlook is realized, but will take careful steps to determine that process.

China is off all week for the Golden Week holiday.

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading up $2.24 or 3.21% at $72.07. At this time yesterday, the price was at $67.67

- Gold is trading down -$11.82 or -0.45% at $2651.04. At this time yesterday, the price was $2654.75.

- Silver is trading up four cents or 0.10% at $31.44. At this time yesterday, the price is at $31.41

- Bitcoin is trading lower than this time yesterday at $61,185. At this time yesterday, the price was at $63,769

- Ethereum is trading lower than this time yesterday at $2456. At this time yesterday, the price was at $2630.80

In the premarket, the snapshot of the major indices trading marginally lower:

- Dow Industrial Average futures are implying a decline of-$159.25 points. Yesterday, fell -173.18 points or -0.41% at 42156.97

- S&P futures are implying a loss of -16.50 points. Yesterday, the index fell -53.73 points or -0.93% at 5708.75

- Nasdaq futures are implying a loss of -35.41 points. Yesterday, the index fell -278.81 points or -1.53% at 17910.36

Yesterday, the small-cap Russell 2000 fell -32.93 points or -1.48% to 2197.03

European stock indices are trading mixed/mostly lower:

- German DAX, -0.67%

- France CAC, -0.19%

- UK FTSE 100, +0.06%

- Spain’s Ibex, -0.58%

- Italy’s FTSE MIB, -0.52% (delayed by 10 minutes)

Shares in the Japan were lower and Australia lower. Hong Kong Hang Seng surged: China is closed for the Golden Week.

- Japan’s Nikkei 225, -2.18%

- China’s Shanghai Composite Index, on holiday for Golden week

- Hong Kong’s Hang Seng index, +6.20%

- Australia S&P/ASX index, -0.13%

Looking at the US debt market, yields are mixed to higher:

- 2-year yield 3.616%, -0.4 basis points. At this time yesterday, the yield was at 3.628%

- 5-year yield 3.527%, +0.7 basis points. At this time yesterday, the yield was at 3.529%

- 10-year yield 3.760%, +1.7 basis points. At this time yesterday, the yield is at 3.744%

- 30-year yield or .108%, +2.7 basis points. At this time yesterday, the yield is at 4.074%

Looking at the treasury yield curve, is more positive/steeper:

- The 2-10 year spread is at +14.3 basis points. At this time yesterday, the yield spread was +11.6 basis points.

- The 2-30 year spread is at +49.1 basis points. At this time yesterday, the yield spread was +44.4 basis points.

In the European debt market, the 10 year yields are higher:

This article was written by Greg Michalowski at www.forexlive.com.

Source link