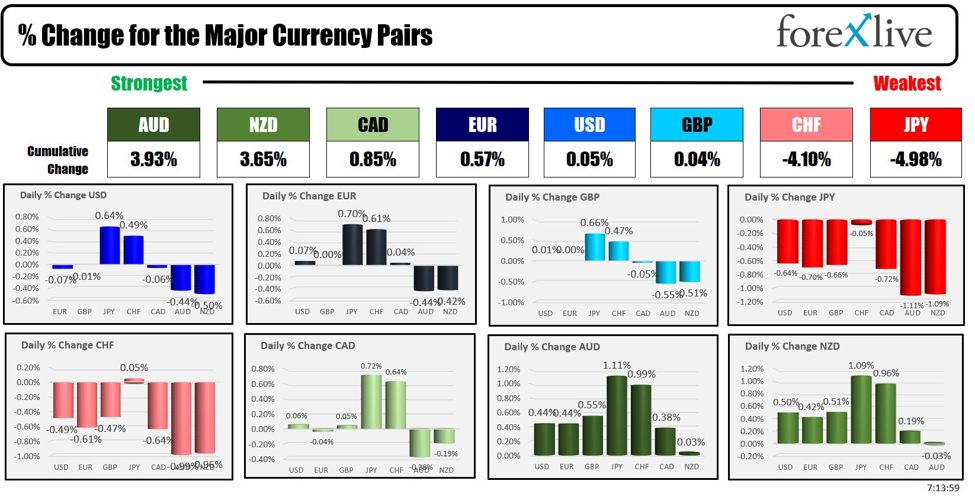

As the NA session begins the AUD is the strongest and the JPY is the weakest. The USD is mixed with gains and losses vs the major currencies. It is a bank holiday in Japan today. It is Monday in the rest of the world, and the economic calendar is light. In the US and Canada today the Canada Building permits and the US Fed. Budget Balance will be released:

- 8:30 AM CAD: Building Permits m/m – Forecast: 5.6%, Previous: -12.2%

- Tentative USD: Cleveland Fed Inflation Expectations – Forecast: 3.8%

- 2:00 PM USD: Federal Budget Balance – Forecast: -254.3B, Previous: -66.0B

Over the weekend and into today, there was some central bank speak and commentary. This week, the RBNZ will announce its rate decision with debate on a cut or no cut.

Summarizing the central banking views today:

- Reserve Bank of Australia Deputy Governor Hauser, speaking at an Economic Society of Australia event, highlighted the significant uncertainty surrounding economic forecasts. He noted that while inflation is expected to remain sticky due to weaker supply and a tight labor market, there is a risk that unemployment could rise faster than currently assumed. Hauser also mentioned the potential for household consumption to increase in line with real incomes, though there is a risk it could rise more strongly due to increased wealth. Additionally, the trajectory of the savings rate remains uncertain.

- This week, the RBNZ meets and decides its interest rate decision on Wednesday. In anticipation, the New Zealand Institute of Economic Research (NZIER) Shadow Board is divided on whether the Reserve Bank of New Zealand (RBNZ) should cut the Official Cash Rate (OCR) in its upcoming August Monetary Policy Statement, but with a majority of the Shadow Board members still supporting a 25 basis-point rate cut due to the slowing economy, labor market conditions, and inflation nearing the target band, others recommend keeping the OCR at 5.50 percent. One member argued that there isn’t sufficient evidence from economic data to justify a rate cut at this time.

- Bank of England (BOE) policymaker Catherine Mann expressed ongoing concerns about upside risks to inflation, highlighting that goods and services prices are expected to rise again and that wage growth remains a significant factor. She noted that wage pressures could take years to diminish. However, Mann mentioned that she has moderated her hawkish stance from a 10 to a 7, as price pressures have eased somewhat in 2024.

- Fed Governor Michelle Bowman, in her speech, emphasized caution regarding potential rate cuts, citing ongoing inflation risks despite some progress. She pointed out that core PCE inflation averaged 3.4% in the first half of 2024, which is still above the Fed’s 2% target. Bowman highlighted factors that could keep inflation elevated, such as supply chain normalization, geopolitical risks, and possible fiscal stimulus, while also expressing concerns about immigration driving up housing costs. She noted signs of cooling in the labor market but emphasized the need for a patient approach to policy decisions, warning against overreacting to single data points. Her comments push back against market expectations of a 50 basis-point rate cut in September.

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading up $0.90 or 1.16% at $77.73. At this time yesterday, the price was $76.66

- Gold is trading up $11.22 or 0.46% at $2442. At this time yesterday, the price was trading at $2426.42

- Silver is trading up $0.44 or 1.60% at $27.89. At this time yesterday, the price is trading at $27.48

- Bitcoin is trading at $59,829. At this time yesterday, the price was trading at $60,693

- Ethereum is trading at $2673. At this time yesterday, the price was trading at $2638.40

In the premarket, the snapshot of the major indices are modestly higher. Lastly, the S&P and NASDAQ indices closed lower for the fourth consecutive week. The Dow Industrial Average closed lower for its second consecutive week

- Dow Industrial Average futures are implying a gain of 67.52 points. Yesterday, the Dow Industrial Average rose 51.05 points or 0.13% at 39497.55

- S&P futures are implying a gain of 4.84 points. Yesterday the S&P index rose 24.85 points or 0.47% at 5344.15

- Nasdaq futures are implying a gain of 44.20. Yesterday the index rose 85.28 points or 0.51% at 16745.30

Yesterday, the small-cap Russell 2000 fell -3.508 points or -0.17% at 2080.91.

European stock indices are trading mostly higher:

- German DAX, +0.18%

- France CAC, -0.09%

- UK FTSE 100, +0.39%

- Spain’s Ibex, +0.14%

- Italy’s FTSE MIB, +0.63% (delayed 10 minutes).

Shares in the Asian Pacific markets closed mixed:

- Japan’s Nikkei 225, on holiday

- China’s Shanghai Composite Index, -0.14%

- Hong Kong’s Hang Seng index, +0.13%

- Australia S&P/ASX index, was 0.46%

Looking at the US debt market, yields are little changed:

- 2-year yield 4.050%, -0.3 basis points. At this time yesterday, the yield was at 4.021%

- 5-year yield 3.796%, unchanged. At this time yesterday, the yield was at 3.784%

- 10-year yield 3.945%, +0.3 basis points. At this time Friday, the yield was at 3.943%

- 30-year yield 4.230%, +0.6 basis points. At this time Friday, the yield was at 4.232%

Looking at the treasury yield curve, the spreads are showing

- The 2-10 year spread is at -10.4 basis points. At this time yesterday, the spread was at -7.6 basis points.

- The 2-30 year spread is at +18.2 basis points. At this time yesterday, the spread was +21.3 basis points.

In the European debt market, the benchmark 10-year yields are higher:

This article was written by Greg Michalowski at www.forexlive.com.

Source link