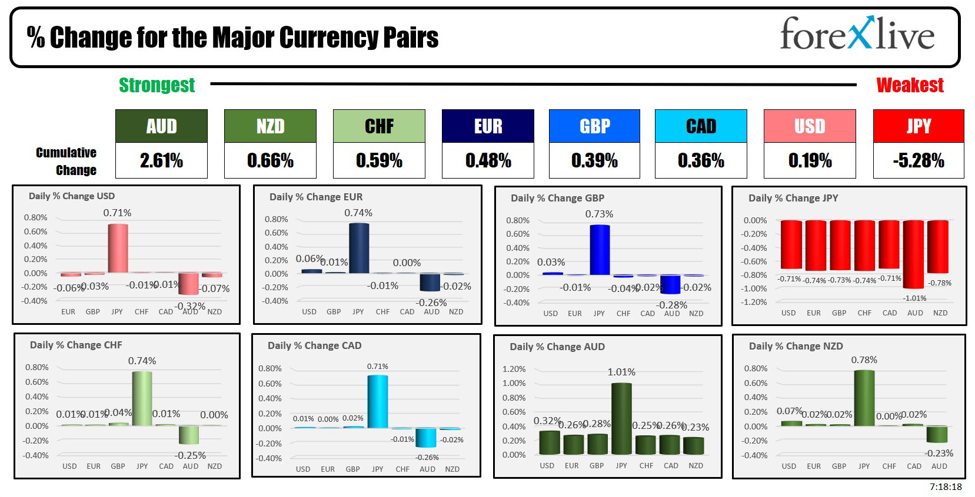

As the North American session begins, the AUD is the strongest and the JPY is the weakest. The JPY is lower across all the major currencies after the Bank of Japan (BOJ) maintained its interest rates at approximately 0-0.10%, a decision made unanimously with a 9-0 vote. Notably, the BOJ removed a key statement from its monetary policy, no longer specifying the purchase of about 6 trillion yen in Japanese Government Bonds (JGBs) per month, indicating a subtle shift in its quantitative easing strategy. This follows a significant rate hike on March 18, the first in 17 years, suggesting a cautious approach to managing the nation’s economic recovery and monetary conditions. The bank acknowledged a moderate recovery in Japan’s economy, although it recognized some areas of weakness and improving output gaps. It also highlighted moderately heightened medium and long-term inflation expectations and generally balanced economic risks, despite the extremely high uncertainties surrounding Japan’s economic and price outlook. The BOJ emphasized the importance of vigilance towards currency and market movements and their potential impacts on the economy and prices. Additionally, it observed that more firms are beginning to pass on rising wages to sales prices, anticipating a positive cycle of wage and inflation increases to continue, with consumer spending expected to rise gradually under accommodative financial conditions.During a press conference, Bank of Japan Governor Kazuo Ueda outlined the central bank’s current monetary policy stance and considerations for future adjustments. Ueda emphasized that the BOJ plans to maintain easy financial conditions for the time being but indicated that the bank’s future monetary policy will be guided by the evolving economic and price conditions, rather than being dictated by a single indicator. He acknowledged that while the Japanese economy has shown moderate recovery, there are still some weaknesses, and highlighted the need to monitor financial and foreign exchange market movements due to their potential impact on the economy and prices.

Governor Ueda clarified that the BOJ’s policy is not aimed at directly controlling the exchange rate but noted that they will continue to observe the effects of foreign exchange on the economy and inflation. Despite the weak yen not significantly influencing trend inflation so far, it has contributed somewhat to higher inflation forecasts. Ueda stated that the likelihood of reaching the BOJ’s 2% inflation target is gradually increasing and that adjustments to the degree of monetary easing might be necessary if underlying inflation rises. He also mentioned that foreign exchange fluctuations could be a factor in monetary policy decisions if they significantly affect underlying inflation, though the impact of FX on inflation is generally considered temporary.

The decision did cause down and up volatility (off of the initial reaction with bond buying omitted from the statement). However, after comments and further review, the net effect has been a continued run to the upside in the JPY pairs (lower JPY). The USDJPY is trading at a new high of 156.829. The next major stop 160.00? The price is running from the 100 hour MA which is down at 155.220 (blue line on the chart below). The 200 hour MA did stall the fall (green line). Buyers leaned against the MAs on the dip. Going forward, it would take a move below that MA to increase the bearish bias.

Today in the US, the Core PCE price index for March will be released at 8:30 AM ET. Off of the measure imbedded in the US GDP suggests the number will be higher than expectations of 0.3% and 2.7% YoY. The market will be focused on revisions as well to gauge the trend. Personal income and consumption (0.5% and 0.6% estimate) are also due at 8:30 AM ET.

At 10 AM ET, the U of Michigan consumer sentiment (FINAL) will be released. The preliminary came in at 77.9. Last month was 79.4. Current conditions preliminary came in at 79.3 (vs 82.5 last month) and expectations came in at 77.0 (vs 77.4 last month)

US stocks are higher on the back of support after earnings from Alphabet and Microsoft which BEAT expectations after the close. Below is a summary of some of the major releases after the close and whether they beat or missed vs the expectations:

Western Digital Corp (WDC): Shares are trading up 0.81% in premarket trading.

- Adjusted EPS of $0.63, BEAT expectations of $0.21.

- Revenue of $3.46bln, BEAT expectations of $3.36bln.

Snap Inc (SNAP): Shares are soaring by 25.44% in premarket trading

- Adjusted EPS of $0.03, BEAT expectations of -$0.05.

- Revenue of $1.19bln, BEAT expectations of $1.12bln.

T-Mobile US Inc (TMUS): Shares are trading down -1.12%.

- EPS of $2.00, BEAT expectations of $1.87.

- Revenue of $19.59bln, MISSED expectations of $19.81bln.

Alphabet Inc (GOOGL): Shares are trading up 11.79% in premarket trading

- EPS of $1.89, BEAT expectations of $1.51.

- Revenue of $80.54bln, BEAT expectations of $78.59bln.

Gilead Sciences Inc (GILD): Shares are trading down -0.18% in premarket trading.

- Adjusted EPS of -$1.32, BEAT expectations of -$1.51.

- Revenue of $6.69bln, BEAT expectations of $6.34bln.

Intel Corp (INTC): Shares are down -8.0% in pre-market trading.

- Adjusted EPS of $0.18, BEAT expectations of $0.14.

- Revenue of $12.70bln, MISSED expectations of $12.78bln.

Microsoft Corp (MSFT). Shares are trading up 4.35%

- EPS of $2.94, BEAT expectations of $2.82.

- Revenue of $61.86bln, BEAT expectations of $60.8bln.

Some earnings today included oil giant Phillips, Exxon Mobile and Chevron. Shares of Phillips 66 is down -0.37%, Exxon shares are trading down -0.93%, while Chevron shares are down -1.0%. Below are some of the major releases from the morning.

Phillips 66 (PSX)

- EPS of $1.90b, MISSED expectations of $2.17.

AutoNation (AN)

- EPS of $4.49, BEAT expectations of $4.45.

- Revenue of $6.49M, MISSED expectations of $6.49bln.

Colgate-Palmolive Co (CL)

- EPS of $0.83, BEAT expectations of $0.81.

- Revenue of $5.07bln, BEAT expectations of $4.96bln.

Exxon Mobil (XOM)

- Adjusted EPS of $2.06, MISSED expectations of $2.20.

- Revenue of $83.083bln, BEAT expectations of $78.35bln.

Chevron Corp (CVX)

- EPS of $2.93, BEAT expectations of $2.87.

- Revenue of $48.7bln, MISSED expectations of $50.66bln.

Centene Corp (CNC)

- EPS of $2.26, BEAT expectations of $2.08.

- Revenue of $40.4bln, BEAT expectations of $36.54bln.

A snapshot of the other markets as the North American session begins currently shows.:

- Crude oil is trading up $0.75 at $84.35. At this time yesterday, the price was at $82.95.

- Gold is trading up $14.21 or 0.61% at $2345.83. At this time yesterday, the price was higher at $2329.19

- Silver is trading up $0.17 or 0.65% at $27.60.. At this time yesterday, the price was at $27.42

- Bitcoin currently trades at $64,342. At this time yesterday, the price was trading at $63,829

In the premarket, the US major indices are trading higher after Microsoft and Alphabet beat expectations after close yesterday

- Dow Industrial Average futures are implying a gain of 51 points. Yesterday, the index fell -375.12 points or -0.98% at 38085.81

- S&P futures are implying a gain of 37 points. Yesterday, the index fell -23.21 points or -0.46% at 5048.41

- Nasdaq futures are implying a gain of 182 points. Yesterday, the index fell -100.99 points or -0.64% at 15611.76

The European indices are trading higher ahead of the US open:

- German DAX, +0.73%

- France CAC , +0.31%

- UK FTSE 100, +0.47%

- Spain’s Ibex, +1.29%

- Italy’s FTSE MIB, +0.91% (delayed 10 minutes)

Shares in the Asian Pacific markets were mostly higher

- Japan’s Nikkei 225, +0.81%

- China’s Shanghai Composite Index, +1.17%

- Hong Kong’s Hang Seng index, +2.12%

- Australia S&P/ASX index, -1.39%

Looking at the US debt market, yields are mostly lower after rising yesterday after the GDP data.

- 2-year yield 4.999%, +0.2 basis points. At this time yesterday, the yield was at 4.926%

- 5-year yield 4.708%, -0.9 basis points. At this time yesterday, the yield was at 4.649%

- 10-year yield 4.685%, -2.0 basis points. At this time yesterday, the yield was at 4.652%

- 30-year yield 4.791%, -2.9 basis points. At this time yesterday, the yield was at 4.789%

Looking at the treasury yield curve spreads moved more inverted:

- The 2-10 year spread is at -31.4 basis points. At this time yesterday, the spread was at -27.8 basis points

- The 2-30 year spread is at -21.0 basis points. At this time yesterday, the spread was at -13.9 basis points

European benchmark 10-year yields are lower:

This article was written by Greg Michalowski at www.forexlive.com.

Source link