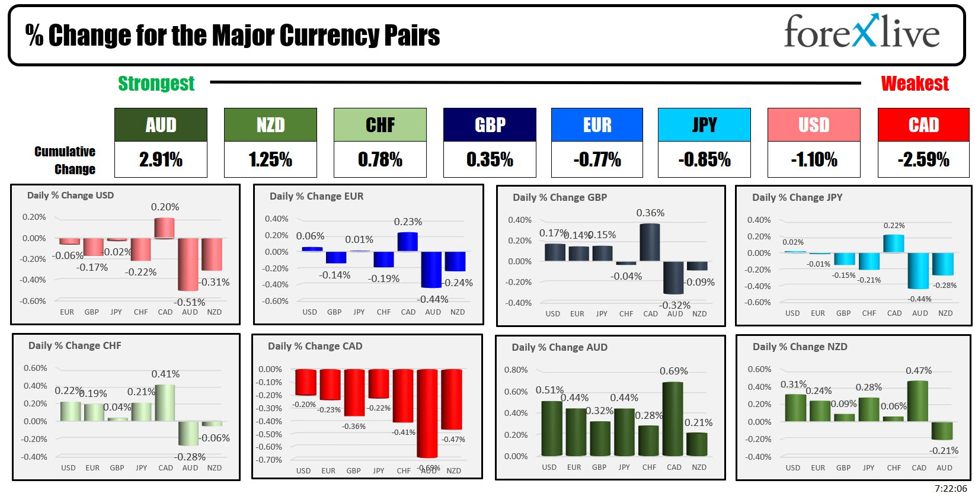

As the North American session begins, the AUD is the strongest and the CAD is the weakest. The ECB will announce its rate decision at 8:15 AM ET, with the expectation for a 25 basis point decline

- ECB expected to lower deposit rate by 25 basis points from 3.50% to 3.25%, with markets pricing nearly a 100% chance of this outcome.

- The sentiment has swayed to a cut after the ECB pattern was to cut in June, no cut in July and cut in Septembers .

- September PMI data was much worse than expected which started the sway.

- Inflation for September contributed to this dovish outlook with the headline falling to 1.8% from 2.2% and the core falling to 2.7% from 2.8% .

- A number of ECB members have hinted at the cut

ECBs Lagarde will start her scheduled press conference at 8:45 AM ET. Markets will be focused on hints of schedule – if any – for futher cuts ahead.

In addition to the ECB rate decision, there are a number of economic releases and events that will be a focus for the markets today:

8:30am

- Core Retail Sales m/m: Forecast 0.1%, Previous 0.1%

- Retail Sales m/m: Forecast 0.3%, Previous 0.1%

- Unemployment Claims: Actual 260K, Forecast 241K, Previous 258K. The hurricanes could be an influence in this number.

- Philly Fed Manufacturing Index: Forecast 4.2, Previous 1.7

9:15am

- Capacity Utilization Rate: Forecast 77.9%, Previous 78.0%

- Industrial Production m/m: Forecast -0.1%, Previous 0.8%

10:00am

- US Business Inventories m/m: Forecast 0.3%, Previous 0.4%

- NAHB Housing Market Index: Actual 43, Forecast 43, Previous 41

-

10:30am

- Natural Gas Storage: Forecast 80B, Previous 82B

11:00am

- Crude Oil Inventories: Forecast 1.8M, Previous 5.8M. Gasoline est -1.47M vs -6.30M last week. Distillates est -2.181M vs -3.124M last week

The private data released late yesterday showed:

11:00 AM

- FOMC Member Goolsbee Speaks

Tentative:

- Treasury Sec Yellen Speaks

2:00 PM

- Federal Budget Balance: Actual 4.5B, Previous -380.1B

4:00pm

- TIC Long-Term Purchases: Previous 135.4B

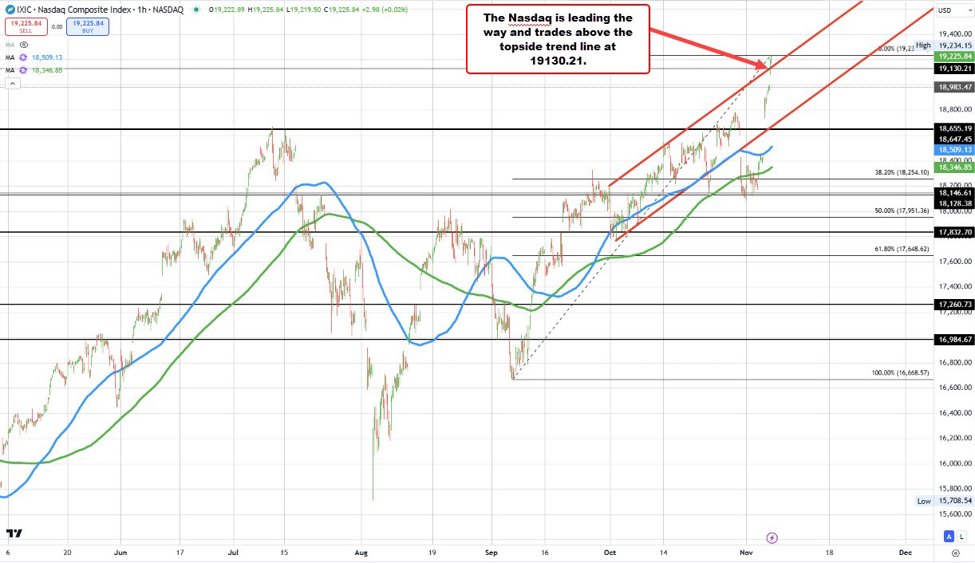

The US stocks are sharply higher in premarket trading, with the Nasdaq leading the way after TSMC earning smashed expectations:

- .Net profit: T$325.26 billion ($10.1 billion), higher than Reuters’ estimate of T$300.2 billion.

- Revenue: T$759.69 billion, up 39% year-over-year.

- Q4 revenue forecast: Between $26.1 billion and $26.9 billion with a gross margin of 57% to 59%.

- Annual revenue expected to grow around 30%.

Shares of TSM in the US are trading up 9.51% in premarket trading.

- Nvidia shares are up 3.10%.

- SMCI are up 3.34%.

- AMD shares are up 2.68%

- Broadcom shares are up 2.86%

The other earnings releases this morning showed:

- Blackstone Inc (BX) Q3 2024: EPS 1.01 (exp. 0.91) → BEAT, AUM 1.11tn (exp. 1.11tn) → MET

- Travelers Companies Inc (TRV) Q3 2024: EPS 5.24 (exp. 3.70) → BEAT, Revenue 11.9bn (exp. 11.45bn) → BEAT

- KeyCorp (KEY) Q3 2024: adj. EPS 0.30 (exp. 0.30) → MET, Revenue 0.695bn (exp. 1.27bn) → MISSED

- Marsh & McLennan Companies Inc (MMC) Q3 2024: adj. EPS 1.63 (exp. 1.62) → BEAT, Revenue 5.69bn (exp. 5.7bn) → MET

- Truist Financial Corp (TFC) Q3 2024: EPS 0.97 (exp. 0.91) → BEAT, Revenue 5.14bn (exp. 5.09bn) → BEAT

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading unchanged at $70.39. At this time yesterday, the price was at $70.16

- Gold is trading up $7.22 or 0.27% at $2680.93.. At this time yesterday, the price was $2680.00

- Silver is trading up nine cents or 0.27% at $71.75. At this time yesterday, the price is at $31.88

- Bitcoin is trading higher at $66,909. At this time yesterday, the price was at $68,030

- Ethereum is trading at $2600.90. At this time yesterday, the price was at $2638

In the premarket, the snapshot of the major indices are showing the Dow industrial average little changed with a gain of 18.3 points. The NASDAQ index is the beginner with a premarket gain of 174 points

- Dow Industrial Average futures are implying gain of 18.30 points. Yesterday, the index rose 337.28 points or 0.79% at 43077.70

- S&P futures are implying a gain of 23.02 points points. Yesterday, the index rose to 27.21 points or 0.47% at 5842.47.

- Nasdaq futures are implying a gain of 174 points. Yesterday, the index rose 51.49 points or 0.28% at 18367.08

Yesterday, the small-cap Russell 2000 rose sharply by 36.85 points or 1.64% at 2286.67

European stock indices are trading mostly higher:

- German DAX, +0.59%

- France CAC, +1.13%

- UK FTSE 100, +0.34%

- Spain’s Ibex, -0.15%

- Italy’s FTSE MIB, +0.99% (delayed by 10 minutes)

Shares in Asian Pacific session shares were mostly lower:

- Japan’s Nikkei 225, -0.69%

- China’s Shanghai Composite Index, -1.05%

- Hong Kong’s Hang Seng index, -1.02%

- Australia S&P/ASX index, +0.86%

Looking at the US debt market, yields are trading modestly higher

- 2-year yield 3.946%, +1.2 basis points. At this time yesterday, the yield was at 3.95%

- 5-year yield 3.856%, +1.4 basis points. At this time yesterday, the yield was at 3.828%

- 10-year yield 4.031%, +1.8 basis points. At this time yesterday, the yield was at 4.006%

- 30-year yield 4.317%, +1.8 basis points. At this time yesterday, the yield was at 4.294%

Looking at the treasury yield curve close steeper on Friday. At the close

- The 2-10 year spread is at +8.7 basis points. At this time Friday morning, the yield spread was +8.3 basis points.

- The 2-30 year spread is at +37.2 basis points. At this time Friday morning, the yield spread was +37.0 basis points.

The benchmark 10 year yields are modestly higher ahead of the ECB rate decision:

This article was written by Greg Michalowski at www.forexlive.com.

Source link