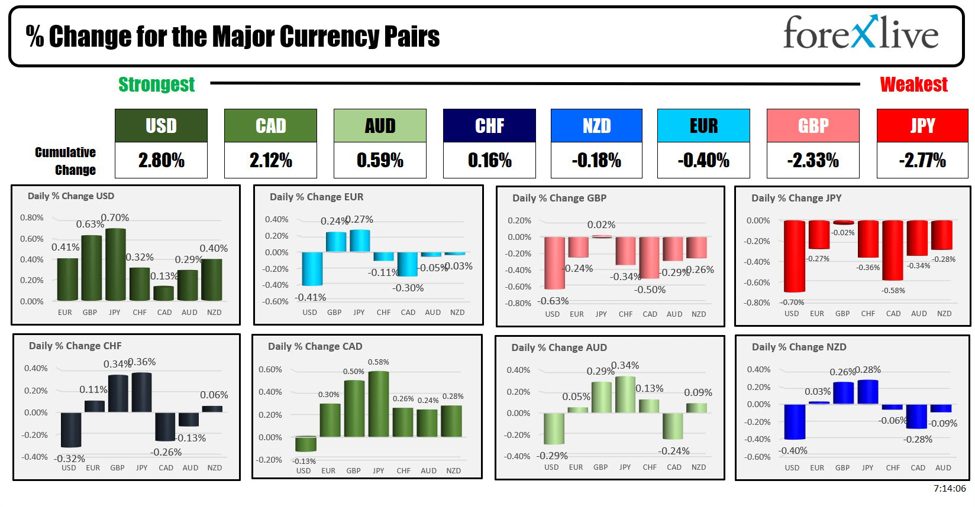

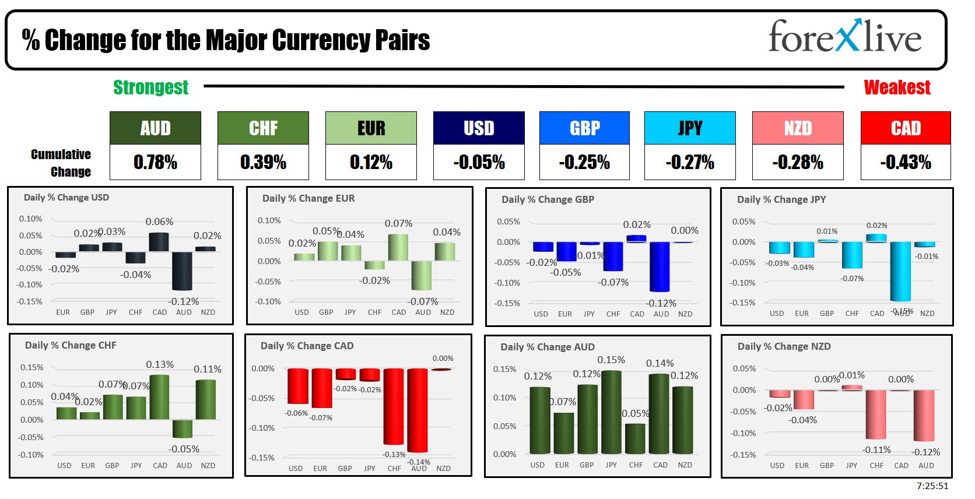

As the North American session begins, the AUD is the strongest and the CAD is the weakest. Having said that, the top to bottom ranking is scrunched together with little separating the winners and losers. The market is awaiting key data is my guess.

Today, the FOMC meeting starts, but it won’t end (well they will go home after work today) until tomorrow when at 2 PM the Fed Chair Powell will announce the Fed rate decision along with the dot plot and the expectations for GDP, employment, and inflation. In the old days when Greenspan was the Chair, they used to film him walking in the building on the first day of the 2-day meeting, and if he had a briefcase it meant one thing, if he didn’t it meant the opposite(such is the life of a chartest I guess… kinda like me sitting in the same spot if the game on TV is going well for my team).

The Fed decision is modestly tilted to 50 bps of cuts vs 25 but it can go either way. If the Fed feels that the lagged effect and the delay in tightening along with the spread between inflation and the current rate is too restrictive, they could do 50. They could also do a 25 bps dovish cut and explicitly say more cuts are coming at a measured pace. Or they can go the ECB path and have a hawkish cut where they say it is all data dependent and then do every other meeting (they already are talking about no cut in October).

UBS says a cut is long overdue but doing 50 might be a panic signal. Morgan Stanley says a 50 bp cut may trigger another wave of Yen carry trade unwind and growth worries. Blackrock says the pricing of deep Fed cuts is overdone (and everyone says the bond market is always right – unless they are not).

Also today, Canada CPI will be released along with US retail sales. Canada CPI is expected to come in at 0.0% with the YoY at 2.1%. The Core YoY was at 1.7% last month, the trimmed at 2.5% est vs 2.7% last, and the Median at 2.2% est. vs 2.4% last. The BOC chose to cut 25 bps at its last meeting.

The US retail sales are expected to decline by -0.2% vs 1.0% gain last month. The Control group is expected to show a rise of 0.3% vs 0.3% last month. Ex Gas and Auto is expected at 0.2% est vs 0.4% last month) .

US Capacity Utilization (77.9% est vs 77.8% last month) and industrial production (0.2% est vs -0.6% last month).are expected at 9:15 AM ET, and Business inventories (0.3% est. vs 0.3% last month) and NAHB Housing index (40 est vs 39 last month) are all expected at 10 AM ET.

The US treasury will auction 20-year bonds at 1 PM ET. Last week’s auctions were characterize by strong overseas demand.

US stocks are higher in pre-market trading after mixed results yesterday. The US yield are mixed with the shorter end higher and the longer end lower (marginally).

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down -$0.93 at $69.18. At this time yesterday, the price was at $69.72

- Gold is trading down -$2.73 or -0.11% at $2579.69. At this time yesterday, the price was $2567.00. Gold closed a record level yesterday.

- Silver is trading up five cents or 0.16% at $30.76. At this time yesterday, the price is at $29.99

- Bitcoin is trading at $59,185. At this time yesterday, the price was at $58,336

- Ethereum is trading at $2311. At this time yesterday, the price was at $2371.50

In the premarket, the snapshot of the major indices are positive. Intel is up as they announced an agreement with Amazon AWS, that they were putting off plant building overseas, that they would separate the foundry business from their chip making business, and other measures. The market is buying it with a gain of around 6.89% in premarket trading at $22.39 (vs $20.91). That is the good news. The bad news is the price is down from $50.29 or -58.39%. A snapshot of the market is showing:

- Dow Industrial Average futures are implying a gain of 147.92 points. Yesterday, the index rose 228.30 points or 0.55% at 41622.08

- S&P futures are implying a gain of 25.41 points. Yesterday, the price rose 7.07 points or 0.13% at 5633.09. The gain was its six consecutive rise.

- Nasdaq futures are implying a gain of 119.22 points. Yesterday, the index snapped a five-day win streak with a decline of -91.85 points or -0.52% at 17592.13.

Yesterday, the small-cap Russell 2000 was higher by 53.06 points or 2.49% at 2182.49

European stock indices are trading higher with solid gains:

- German DAX, +0.74%

- France CAC, +0.76%

- UK FTSE 100, +0.77%

- Spain’s Ibex, +1.37%

- Italy’s FTSE MIB, +0.99% (delayed 10 minutes).

Shares in the Asian Pacific markets were mixed:

- Japan’s Nikkei 225, -1.03%

- China’s Shanghai Composite Index, banking holiday

- Hong Kong’s Hang Seng index, +1.37%

- Australia S&P/ASX index, +0.24%

Looking at the US debt market, yields are mixed.

- 2-year yield 3.569%, +1.4 basis points. At the same Friday, the yield was at 3.546%

- 5-year yield 3.408%, +0.4 basis points. At this time Friday, the yield was at 3.407%

- 10-year yield 3.608%, -1.3 basis points. At this time Friday, the yield is at 3.636%

- 30-year yield 3.912%, -2.6 basis points. At this time Friday, the yield is at 3.9262%

Looking at the treasury yield curve,

- The 2-10 year spread is was 4.3 basis points. At this time yesterday, the yield spread was +8.9 basis points.

- The 2-30 year spread is +34.4 points. At this time yesterday, the yield spread was was 41.5 basis points.

In the European debt market, the 10 year yields are mostly lower:

This article was written by Greg Michalowski at www.forexlive.com.

Source link