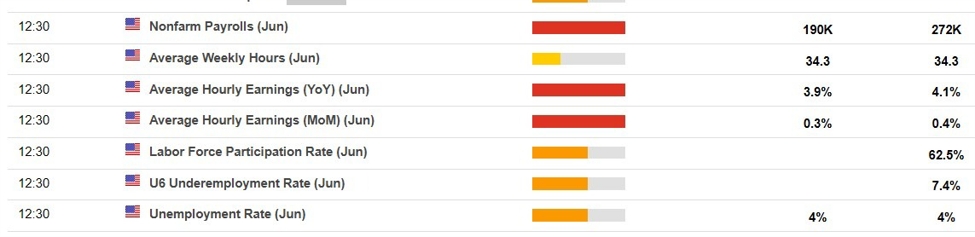

It’s all because of this: US July non-farm payrolls +114K vs +175K expected

Or at least that is what the narrative is running with. Bloomberg highlighted the Sahm rule after the Fed last week and it was again a focus point after the spike in the unemployment rate on Friday.

Alongside the softer non-farm payrolls number, it’s easy to get all caught up in the hype and forget the smaller details. That such as the slight increase in the participation rate also perhaps playing a bit part in the jobless rate increase.

That being said, facts are facts. US unemployment is now higher than it was before the pandemic. And after Friday’s report, it is also higher than the Fed’s supposed “natural” rate of unemployment of 4.2%.

But let’s rewind to just before that. After the FOMC meeting last week, Powell sold the story of a soft landing in the economy. And markets lapped it all up. Equities jumped and were poised for a strong finish to the week, all before the heavy selling came on Thursday. And then the carnage on Friday of course.

So, how did we go from soft landing to crash landing?

Before, there were still many arguing that it’s fine for the Fed to leave rate cuts to September. And all of a sudden, the same camp is arguing for the Fed to now go 50 bps in back-to-back meetings. Insanity. Just because of a little kicking and screaming when yet, the S&P 500 is still up 12% on the year after the Friday close.

The thinking is that the latest US jobs report may highlight that the Fed is behind the curve on rate cuts. So, the main question now is are they really?

Well, if labour market signals are anything to go by, there is certainly an argument for that. But the US consumer remains solid and that’s a counter-argument at least. But whatever the case is, it is what the Fed perceives to be true that is going to be the most important factor.

And I would say that policymakers will remain stubborn for now. However, the next question is will they get bullied into a decision by markets? We’ve seen that one too many a time over the years already.

And right now, after the AI boom, we’re perhaps seeing a mini-bust in the stock market and investors are kicking and screaming. They want the Fed to pacify them once again and to inject that liquidity into their veins again.

The stock market is not the economy but it doesn’t mean that Wall Street has no say in all this. The Fed has been bullied into making decisions before and they may very well succumb to that again in September.

This article was written by Justin Low at www.forexlive.com.

Source link