- Germany April preliminary CPI +2.2% vs +2.3% y/y expected

- US Treasury refunding update: $243 billion vs $202 billion prior

- ECB’s De Guindos: We are heading in the right direction on inflation

- Dallas Fed manufacturing business index -14.5 vs -14.4 prior

- The ECB games its staff survey to avoid further embarrassment

Markets:

- Gold down $2 to $2335

- US 10-year yields down 5 bps to 4.62%

- WTI crude oil down $1.10 to $82.76

- S&P 500 up 0.3%

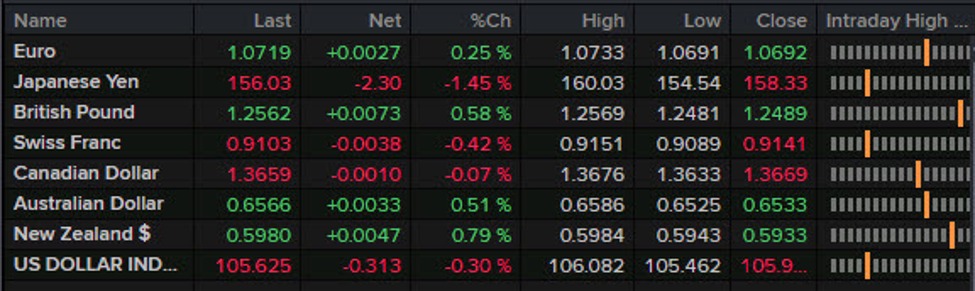

- NZD leads, JPY lags

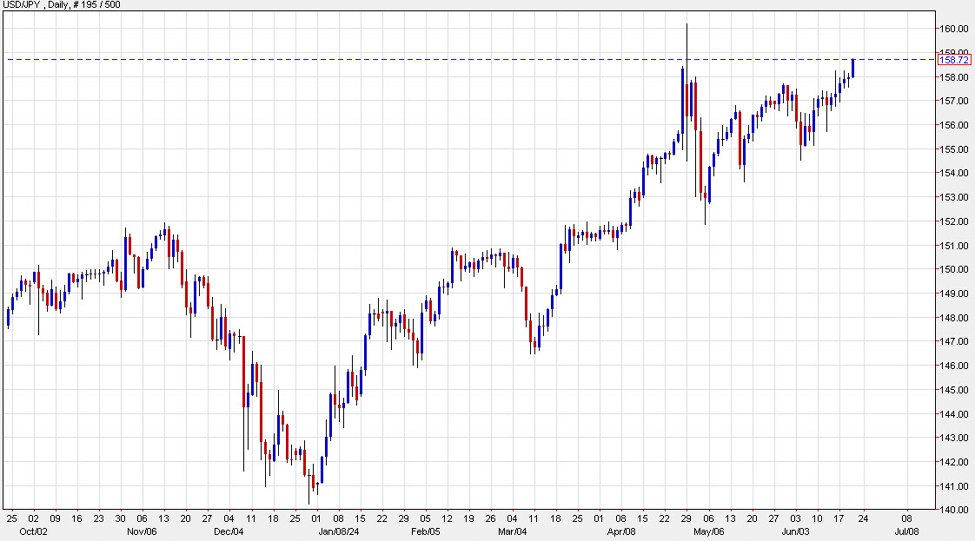

It was all about the yen today after what looks like a round of intervention from the MoF. A Dow Jones report unofficially confirmed it as did a 500 pip drop after breaking the 160.00 barrier. The move was slowly fading as North American traders arrived and appeared to stabilize just below 157.00. Then in the US afternoon, a second wave of selling hit taking the pair back to 155.00. The dip was bought again and the pair settled out near 156.00.

Aside from the yen, it wasn’t quite. The US dollar was generally softer as Treasury yields slipped. Cable took advantage with a 70 pip gain, most of it in North American trade. The Treasury borrowing estimates briefly knocked down yields but the market later concluded it was a timing and cash balance issue.

The euro also made some headway against the softening dollar. Some dollar weakness was likely related to position squaring ahead of a big week of economic data, staring with Consumer Confidence tomorrow.

Commodity currencies were generally higher but NZD and AUD far outpaced the loonie as oil prices pulled back. Talk of further rate hikes is helping to lift the Aussie back towards 0.6000.

This article was written by Adam Button at www.forexlive.com.

Source link