- US July retail sales +1.0% versus +0.3% expected

- Walmart offered six endorsements on the health of the US and global consumer

- US initial jobless claims 227K vs 235K expected

- US July Philly Fed -7.0 vs +6.0 expected

- August Empire Fed -4.7 vs -6.0 expected

- US July import prices 0.1% vs -0.1% expected

- US August NAHB home builder sentiment survey 39 vs 43 expected

- US June business inventories +0.3% vs +0.3% expected

- US July industrial production -0.6% vs -0.3% expected

- Fed’s Musalem: Time may be nearing for a change in the policy rate

- Canada June wholesale sales -0.6% vs -0.6% expected

- Atlanta Fed GDPNow Q3 2.4% vs 2.9% prior

- PBOC Governor Pan: Will stabilize expectations and help consolidate recovery

- Bank of America fund manager survey highlights optimism in a soft landing, equities

Markets:

- S&P 500 up 1.6%

- WTI crude oil 98-cents to $77.98

- US 10-year yields up 10 bps to 3.92%

- Gold up $8 to $2456

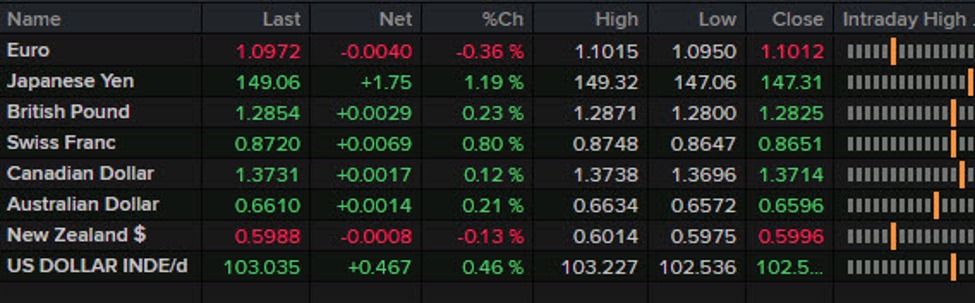

- AUD leads, JPY lags

It was all about the economic data today as US retail sales and initial jobless claims underscored a resilient economy that’s not tumbling towards a hard landing. Fed pricing for 50 bps fell to just 25% after the numbers, which were underscored by upbeat comments from Walmart executives following earnings.

The initial response was a strong wave of US dollar buying, particularly against the yen as is surged more than 170 pips in a straight line. Elsewhere the dollar rose 30-60 pips but those trades often didn’t last as the upbeat risk mood competed with higher Treasury yields.

Ultimately, USD/JPY tracked to the highs of the day late while the other trades chopped and sometimes completely retraced. Cable fell as low as 1.2800 from 1.2860 but later completely rebounded and is on track to close the day up by 30 pips.

The euro fell 50 pips to 1.0950 initially before fighting back to 1.0985 before giving back a dozen pips late, to close down 40 pips on the day.

The commodity currencies were choppy as well as they fully recovered from 30-40 pip declines only to sag again, with CAD closing near the lows of the day, partly on housing worries due to rates moving back up.

The day marks a stark turnaround from last Monday when the world was screaming recession and emergency rate cuts. Eyes will now be on Japan as the carry trade flirts with the 38.2% retracement of the July-August rout.

This article was written by Adam Button at www.forexlive.com.

Source link