- BofA: A brief and recent history of US FX policy

- US equities edge higher as Nvidia scores another gain

- Crude oil futures settle at $81.41

- Betting odds of Biden sticking around firm

- Why Fed easing will come too late to prevent a major slowdown in growth

- U.S. Treasury auctions off $58 billion of three-year notes at a high yield of 4.399%

- The EIA short term energy outlook is out and they see demand increasing

- European major indices close lower.

- Powell: The labor market appears to be fully back in balance

- Fed Chair Powell: Elevated inflation is not the only risk we face

- Semiconductor surge leads the charge: Today’s market exploration and insights

- Kickstart the FX trading day for July 9 w/a technical look at the EURUSD, USDJPY & GBPUSD

- Japanese stocks broke out today. Blackrock sees more to come

- Forexlive European FX news wrap 9 July – An uneventful session

- The USD is the strongest and the JPY is the weakest as the NA session begins

- US June NFIB small business optimism index 91.5 vs 90.5 prior

Fed Chair Powell testified at the U.S. Senate today on Capitol Hill in the first of two testimonies in front of US lawmakers. Tomorrow the chair will be speaking to the House of Representatives.

During his testimony today, Fed chair explicitly said that he would not talk about a change in rates timetable, although he did signal that is most likely to be a decline in rates. He characterized the risk as two-way and not just skewed toward inflation. He commented on a couple occasions, that the labor market has cooled considerably, but that it remains strong. Nevertheless, he thought employment wasn’t a large contributor to inflationary pressures.

The chairs comments kept September cut on the table, and the potential for two cuts still an “odds-on favorite” possibility (with December pricing in a 75% chance). Below is a summary of the major points made by the chairman on policy, the economy, inflation, growth, and employment

Policy and Decision-Making:

- The Fed remains committed to a 2% inflation goal and maintaining well-anchored long-term inflation expectations.

- Decisions on rate adjustments will be made carefully, considering incoming data, balance of risks, and appropriate policy paths.

- There are risks both in reducing restraint too late or too little, which could weaken the economy and job market, and in reducing restraint too soon or too much, which could reverse inflation progress.

- The Fed will continue making decisions on a meeting-by-meeting basis and does not plan a policy rate cut until there’s greater confidence that inflation is heading sustainably toward 2%.

Economy:

- The US economy is expanding at a solid pace and has performed exceptionally compared to global peers.

- GDP growth appears to have moderated in the first half of 2024.

Inflation:

- Inflation remains above the 2% goal, but there has been considerable progress toward this target with recent monthly readings showing modest further progress.

- More good inflation data is needed to build confidence in cutting rates.

- Restrictive policy is currently helping to put downward pressure on inflation.

Growth:

- The economy has been expanding solidly, but there are significant housing issues exacerbated by the pandemic.

- The Fed’s tighter policy is impacting housing sector activity, with the best way to address housing supply issues being to reduce inflation.

Employment:

- The labor market has cooled considerably but remains strong and is now more or less back to pre-pandemic levels.

- Unemployment is still low by historical standards.

- Wage increases, while still high, are coming down to more sustainable levels.

- The Fed recognizes the labor market is not a broad source of inflationary pressures now and aims to balance risks in achieving employment and inflation goals.

Additional Points:

- The Fed is having discussions about potential changes to the Basel III endgame proposal and is close to an agreement on these changes.

- Immigration is seen as neutral on inflation in the long run, but it may have had short-term impacts, particularly on the housing market in certain areas.

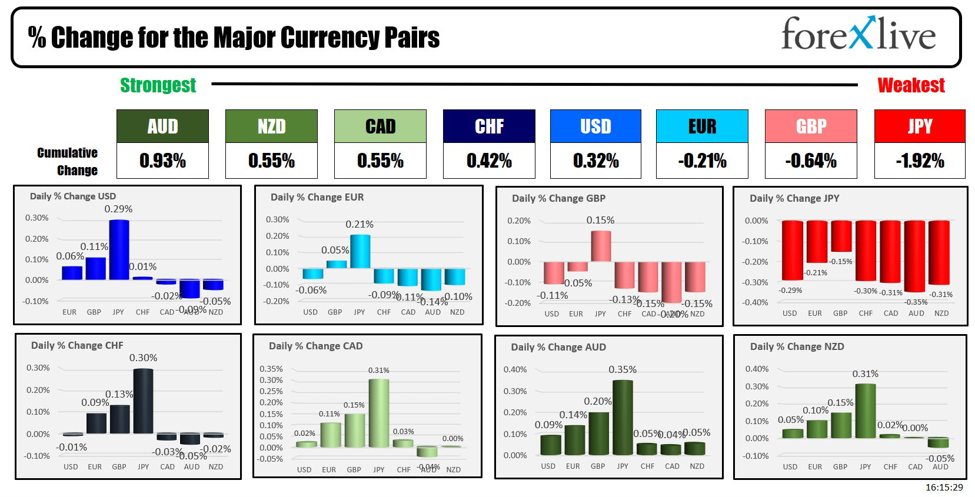

As the dust settles in the Forex market, the AUD is ending the day as the strongest of the major currencies, while the JPY is the weakest. The USD is ending mixed/modestly higher with modest declines versus the CAD, AUD and NZD, and gains vs the JPY, GBP, and EUR.

The USD was higher intraday, but the start of the coupon auctions for the week at the 1 PM ET auction, saw strong demand for the 3-year note. The auction not only had a negative tail to the WI of -0.8 basis points, but had above average bid-to-cover ratio as well. Demand was led by strong domestic buyers which was a bit unusual. More recent auctions have been led by the international demand (see auction results by clicking here).

The auction results helped to ease some of the supply concerns that may have weighed on treasury prices earlier today. Though yields are ending the day higher, they are also off their high levels just prior to the auction. The U.S. Treasury will auction off 10 and 30-year issues tomorrow and on Thursday.

At the end of day, a snapshot of the market shows:

- 2-year yield 4.626%, +0.8 basis points

- 5-year yield 4.244%, +0.2 basis points

- 10 year yield 4.297%, +2.9 basis points

- 30 year yield 4.490%, +3.2 basis points

The Fed Chair Powell comments and auction results, did not hurt the stock market, but the price action was more up and down. Nevertheless, the broader indices (i.e., S&P and NASDAQ indices), did close higher once again and at record levels. For the S&P index, it has now closed at a new record for four consecutive days. For the NASDAQ index, it has closed at a new record for five consecutive days.

- The S&P index rose 0.07%.

- The Nasdaq index rose by 0.14%

The Dow industrial average (of 30 stocks) traded down -198.20 points at session lows, and as high as up 147.48 points at session highs. The index is closing down -52.82 points in what was volatile up-and-down trading for that index.

In other markets:

- Crude oil fell for the third consecutive day. Strain down $0.68 or -0.83% at $81.65

- Spot gold is trading up $5.89 or 0.25% at $2363

- Silver is trading unchanged at $30.79

- Bitcoin is trading higher at $57,958.

In the new trading day, the Reserve Bank of New Zealand will announce its interest-rate decision with no change expected.

Tomorrow will be another quiet day on the economic calendar with Fed chair Powells testimony at 10 AM ET, weekly oil inventory data at 10:30 AM ET. The U.S. Treasury will auction off 10-year notes at 1 PM ET. Feds Bowman and Goolsby will speak at 2:30 PM ET, and Feds Cook will speak later in the evening at 7:30 PM ET.

This article was written by Greg Michalowski at www.forexlive.com.

Source link