- Decline in US Stocks Continues, Tech Giants Witness Major Losses

- Yellen says market should determine exchange rates

- NYT Sienns College Poll: Trump 48%. Harris 46% among registered voters

- US treasury auctions off $44 billion of the 7 year notes at a high yield of 4.162%

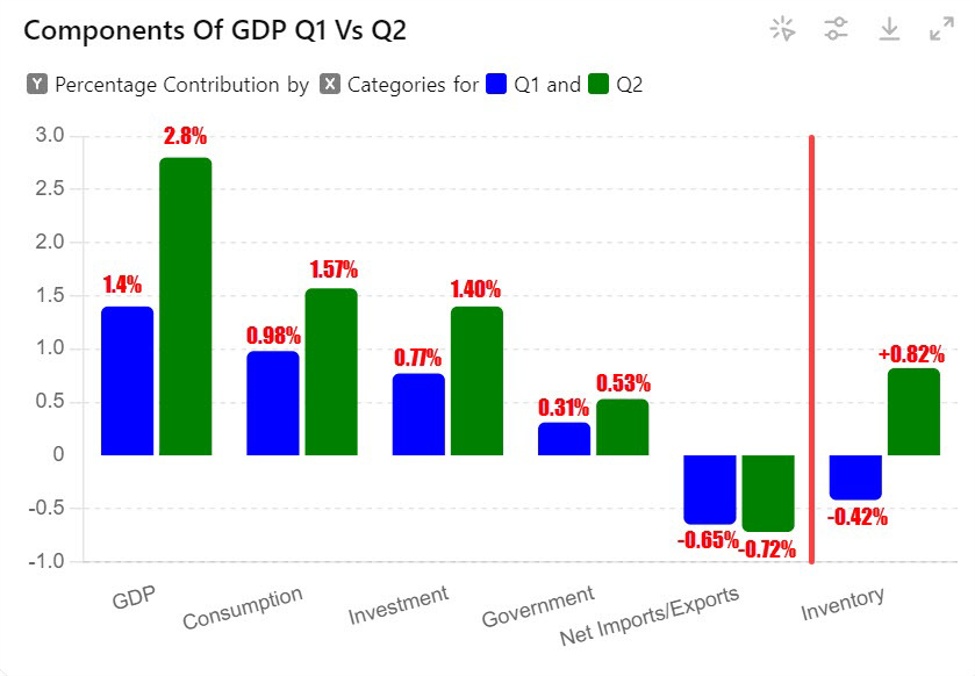

- Ex inventories, GDP Q1 is near 1.80%%. GDP Q2 adjusted is near 2.0%. Not far from trend.

- European major indices close mixed (thanks to the UK FTSE 100)

- WSJ Timiraos: Core PCE can still be up 0.18% when released on Friday, but….

- Kickstart the FX trading day for July 25 w/a technical look at the EURUSD, USDJPY & GBPUSD

- Former Fed Pres.Bullard: Fed is likely to signal they are getting ready to go in September

- US GDP Advanced for Q2 2.8% vs 2.0% estimate

- US advanced durable goods for June -6.6% versus 0.3% expected

- US initial jobless claims 235K vs. 238K expected

- The JPY is the strongest and the AUD is the weakest as the NA session begins

- ForexLive European FX news wrap: Yen gains stay the course as risk selloff continues

The USD GDP for Q2 came in stronger than expectations at 2.8%. Growth was led by consumption as he contributed 1.57%, and investment which added 1.4%. However, within the investment bucket, inventory accumulation added about 0.8% to the final 2.8% gain. So ex-inventory, GDP was closer to the 2.0% trend growth

PS the 1Q came in at 1.4% but -0.42% was inventory. If you look at ex-inventory, growth was 1.82%. So overall, 1Q was stronger than what was implied, while 2Q was weaker than the 2.8% reported (ex-inventories at least)> who

Looking at the inflation data, it was somewhat favorable. However, core PCE prices annualized were bit higher than the expectations. Specifically, they rose 2.9% versus 2.7% expected. That was still much lower than the 3.7% from Q1, which is good to know.

The core PCE – the Fed’s favored inflation gauge – will be released tomorrow at 8:30 AM ET.. Today, was a view into that number as it included a figure for June.

Mathematically, we already know other data for the year. Therefore, the higher 2.9% implies that either the June number will be higher, or there will be revisions to the prior months (in order to get to 2.9%).So we will see at 8:30 AM tomorrow. New

Other data today showed Durable goods tumbled by -6.6% but it was impacted by volatile transportation component.

The weekly initial jobless claims did dip to 235K vs 245K last week. Continuing claims were also lower than expectations which suggests joblessness is not worsening (at least for now).

So fundamentally, GDP is around 2% for the 1H of 2024. Employment is a little weaker of late, but not in a fast decline.

In the stock market today – a day after the broader indices had their worst day since the end of 2022 – the downward momentum continued in those indices.

The S&P fell -27.89 points or -0.51%. The Nasdaq index shed another -160 points or -0.93% after falling -3.6% yesterday. The good news is it could have been worse. At session lows the Nasdaq was down over -300 points. Is the Nasdaq, going to go for -10%? It is currently down around 8% from it’s recent highs.

The fall in the stock market, kept the flow of fund in the forex focused toward the CHF. It is ending the day as the strongest of the major currencies. The NZD and the AUD, remain as the weakest as they react to slower China growth (and the potential for a weakening of the US economy in 2H of 2024).

The USDJPY which ran to a new low going back to May, bounced higher (after testing a key support target)and is ending the day little changed.

The EURUSD is ending the day little changed fter a run lower failed, as did a rebound higher. Sellers are more in control in the short term going into the new trading day. See post HERE.

The USDCAD took out it’s 2024 high but only by a few pips before failing and wandering back toward key support near a break point higher from yesterday’s trading.

The AUDUSD and the NZDUSD remain under pressure (see video here for the key technical levels in play for those pairs).

This article was written by Greg Michalowski at www.forexlive.com.

Source link