- VIX has closed at its highest since April 19

- Big Wins and Misses: IBM and Chipotle Beat Expectations, Ford Falls Short

- NASDAQ index has its worst trading day since November 2, 2022

- Crude oil settles at $77.59

- Bitcoin consolidating between 100 and 200 hour moving averages

- U.S. Treasury auctions off $70 billion of the 5-year note at a high yield of 4.121%

- European major indices close lower

- Atlanta Fed GDPNow growth estimate for 2Q comes in at 2.6% vs 2.7% previously

- Bank of Canada’s Macklem. We need to be more symmetric in our policy

- EIA weekly crude oil inventories drawdown of -3.741M vs drawdown of -1.583M estimate

- Fed’s Dudley: It may be too late to fend off a recession

- BOCs Macklem’s press conference opening statement

- What changed in the BOC rate statement from June to July? A lot

- US new home sales for June 0.617M vs 0.640M estimate

- The Bank of Canada cuts rates by 25 basis points to 4.50% from 4.75%

- US July flash services PMI 56.0 vs 55.0 expected

- Don’t expect geopolitics to get any better

- US preliminary wholesale inventories for June +0.2% versus 0.5% estimate

- US goods trade balance for June -$96.8 billion versus $-98.8 billion estimate

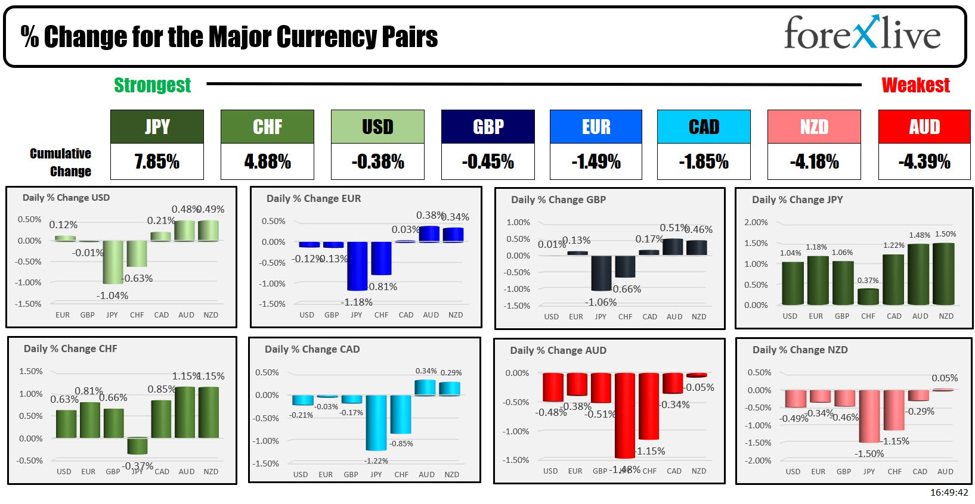

- The JPY is the strongest and the NZD is the weakest as the NA session begins

- ForexLive European FX news wrap: Yen gains continue, equities in retreat mode

- US MBA mortgage applications w.e. 19 July -2.2% vs +3.9% prior

The US stock trading got off to a weak start. Shares of 2 of the Magnificent 7 – Alphabet and Tesla – announced earnings after the close yesterday and the markets did not like them (even though Alphabet beat on the top and bottom lines).

Moreover, markets were a little spooked by comments made by former Fed Governor Dudley (the Fed is in the quiet period ahead of their interest rate decision) who said that the unemployment negative cycle was kicking in and the Fed should not dawdle with regard to cutting rates. He added that It might already be too late to slow unemployment from moving higher. Tomorrow’s initial jobless claims should be interesting after last week’s 342K jump. Continuing claims were also elevated last week

With earnings season just getting going, visions of “slower growth ahead” danced in traders heads and they took stocks lower.

After the lower opening, the best the Nasdaq could do today was -250 points on the day. The S&P’s best was -47.71 points. Ouch. The broader S&P and Nasdaq indices each had their worst trading days since December 2022 and November 2022 respectively. Ouch.

At the bell, the S&P fell -2.32% while the NASDAQ index tumbled -3.64%. The Dow Industrial Average average fell -1.25% and the Russell 2000 fell -2.13%.

In the Forex market, the JPY and the CHF were the flight to safety beneficiaries. They are the strongest of the major currencies. The AUD and the NZD were once again the weakest of the majors as concerns about China and potentially US, is traditionally not a good combination for those countries. I think it is the third day in a row that those currencies are the weakest (might be 4 days).

In Canada, the Bank of Canada cut rates for the second consecutive meeting by 25 basis points to 4.5% from 4.75%. The USDCAD moved above the high of the trading range since April at 1.38038. Can the price keep the momentum in the new day and push toward the high for the year at 1.38448?.

For the USDJPY, it tumbled below its 100-day moving average at 155.419 and also worked its way below the 38.2% retracement of the trend move up from the December 2023 low. That level came in at 153.654. However, late-day buying did push the price back above that 38.2% retracement. Upside resistance in the new date will be at the swing area between 154.52 and 154.87.

In the US debt market, the yield curve steepened with the 2-year down -1.2 basis points and the 30 year up 7.2 basis points:

- 2-year yield 4.432%, -1.2 basis points

- 5-year yield 4.175%, +2.5 based point

- 10-year yield 4.285%, +4.7 basis point

- 30-year yield 4.541%, +7.2 basis points

The 2-10 year spread is moved closer to parity at -14.7 basis points (its highest level since October 2023). The 2-30 year spread move to +10.9 basis points. That is it’s steepest since July 2022.Tomorrow, the first cut for Q2 growth will be released with the economists looking for 2.0%. The Atlanta Fed GDPNow closed it’s book on its model with a higher value of 2.6%.

Perhaps of greater interest will be the weekly claims data. Last week, the initial claims rose to 243K. It is expected to dip to 237K tomorrow. If it surprises to the upside once again, the Dudley fears may make for another troublesome day as bad news continues to be bad news. However, it may also mean the Fed will be ready a little earlier for a cut in July vs September. US core PCE will be released on Friday (Fed’s favorite inflation measure).

This article was written by Greg Michalowski at www.forexlive.com.

Source link