- Stocks move toward new lows going into the last 101-15 minutes but bounces into the close.

- Republican Pres. nominee Trump picks JD Vance as his VP running mate

- Crude oil futures settle at $81.91

- More from Powell: We don’t want to be too risk averse

- Fed’s Powell: Economy performed really well over the last couple of years

- Goldman Scahs makes the case for a July Fed cut. What’s priced in?

- European equity close: Struggles to start the week

- Gold catches a fresh big in push towards record high

- Bank of Canada business outlook survey highlights growing pessimism

- Classified documents case against Trump dismissed

- Another reason why the Bank of Canada is likely to cut rates this month

- US stocks open with gains. Markets shrug off assassination attempt.

- Kickstart the FX trading day for July 15 w/a technical look at the EURUSD, USDJPY & GBPUSD

- Bear steepener is the Trump trade so far

- New York Fed manufacturing index for July -6.6 versus -7.0 estimate

- Canada May wholesale sales -0.8% vs -0.9% expected

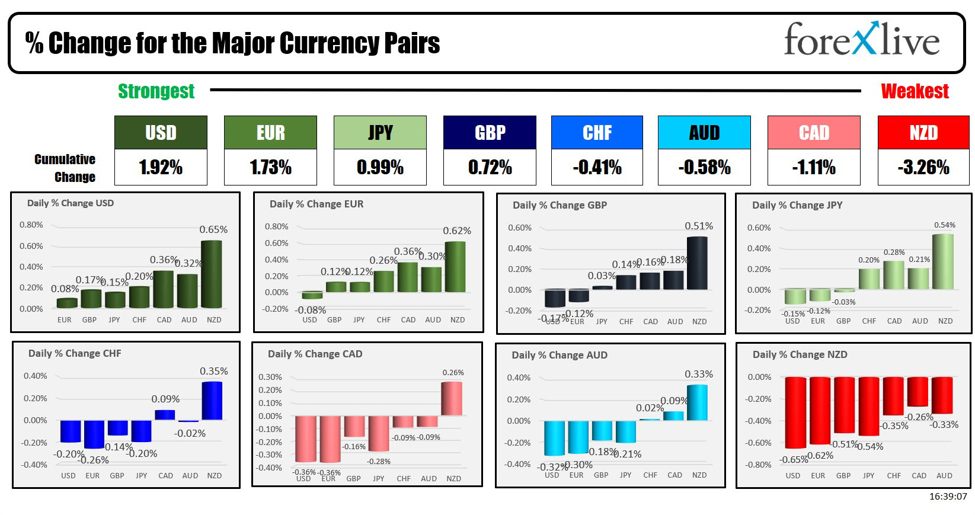

- The EUR is the strongest and the NZD is the weakest as the NA session begins

- ForexLive European FX news wrap: Dollar gains fade as markets digest Trump rally shooting

- Forex Expo Dubai 2024 Announces Emirates as Official Airline Partner

The markets largely shrugged off the shocking weekend assassination attempt on Republican nominee Donald Trump. Despite the dramatic events, including the start of the Republican National Convention where Trump was officially nominated and selected JD Vance as his vice-presidential pick, the so-called “Trump Trade” was ignited. This trade involves selling long-term bonds, thereby steepening the yield curve, and buying stocks, Bitcoin, and the USD, which saw gains today. The USD emerged as the strongest major currency, while the NZD was the weakest.

The Trump Trade is fundamentally driven by expectations that Trump’s administration would lower regulations, potentially increase oil drilling leading to lower oil prices, advocate for lower interest rates (possibly replacing Fed Chair Powell), and cut taxes. Additionally, his policy stance includes raising tariffs, closing borders, deporting illegal immigrants, exiting NATO, and halting payments to Ukraine. While these moves could benefit businesses, they may also increase inflation and deficits.

In the US debt market, yields rose with the

- 2-year yield at 4.461% (+0.2 basis points),

- 5-year yield at 4.135% (+2.4 basis points),

- 10-year yield at 4.231% (+4.4 basis points), and

- 30-year yield at 4.458% (+5.7 basis points).

The 2-10 year spread increased to -22.9 basis points, its highest (though still negative) since January 25, while the 2-30 year spread is nearly flat.

In the stock market, the Russell 2000 outperformed with a significant gain of 1.80%. The Dow Industrial Average also benefited, closing at a record high of 40,221.72, its first since May 17.

The S&P index closed just below its record at 5,633.92 after reaching a new intraday high of 5,666.94.

The NASDAQ index rose but remains short of its record last Wednesday at 18,647.45.

The day’s final changes showed the

- Dow up by 0.53%,

- S&P by 0.28%, and the

- NASDAQ by 0.40%.

On the fundamental front, the Empire Manufacturing Index came in at -6.6, slightly better than the -7.0 estimate.

Finally,, Federal Reserve Chair Jerome Powell, speaking at the Economic Club of Washington, underscored the economy’s strong performance over the past few years, though he noted a slowdown and ongoing progress in reducing inflation. He emphasized that the labor market is no tighter than pre-pandemic levels and highlighted recent positive inflation data. Powell reiterated that the Fed will make decisions based on evolving data, without political influence, and cautioned against delaying action on inflation. Confident in achieving a 2% inflation target without severe economic pain, he downplayed the likelihood of a hard landing scenario. Powell intends to remain in office until May 2026, with the timing of Fed actions dependent on sustained improvements in inflation data. He also noted the eurozone’s different economic position but acknowledged commonalities in global central bank policies. Lastly, Powell expressed long-term concerns about US deficits but stressed that it is not the Fed’s role to advise on fiscal policy.

This article was written by Greg Michalowski at www.forexlive.com.

Source link