- Oil – private survey of inventory shows a larger headline crude oil draw than was expected

- It is a solid day for US indices. Indices close the day near highs with PPI the catalyst.

- Rick Reider: Market cleaned out a lot of leveraged positions

- Crude oil futures settled at $78.35

- Atlanta Fed Pres. Bostic: Balance of risks and economy is getting back to level

- Geopolitics: Sec of State Blinken: Postpones trip to the Middle East

- Will oil prices follow gas prices?

- European indices close higher

- Iran holds military drills in the northern part of the country

- Market surge led by tech giants: Exploring today’s vibrant stock landscape

- Reuters poll: US 10 year treasury note yield to rise to 4.03% in three months:

- Geopolitics: Explosion heard in Tel Aviv

- Kickstart the FX trading day for Aug 13 w/a technical look at the EURUSD, USDJPY & GBPUSD

- US PPI Final Demand MoM 0.1% vs 0.2% estimate. YoY 2.2% vs 2.3% est

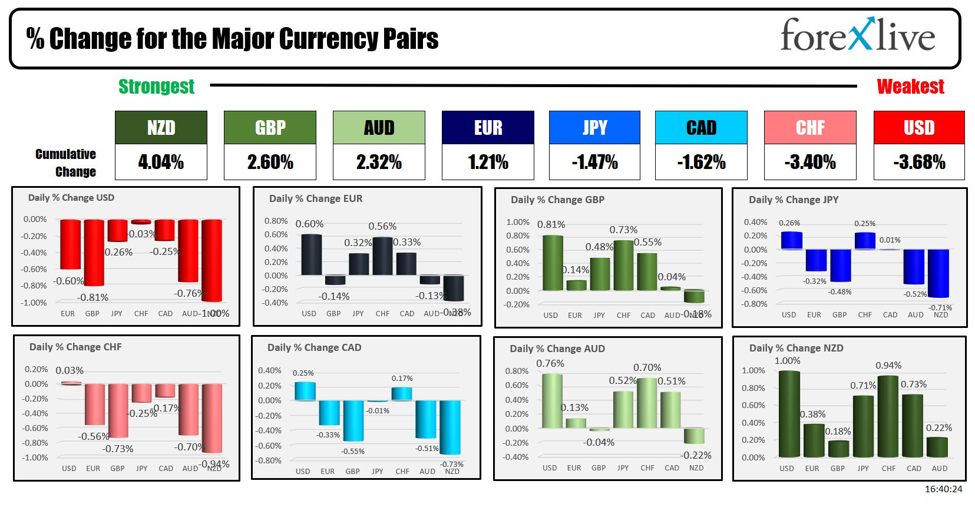

- The NZD is the strongest and the CHF is the weakest as the NA session begins

- Forexlive European FX news wrap 13 Aug – UK jobs data beats estimates

US PPI data came in tamer than expectations with a rise of 0.1% vs 0.2%. The YoY fell to 2.2% from 2.7%. The core ex food and energy was down to 2.4% from 3.0%. That is good news and although it does not necessarily translate into a better CPI tomorrow, hope springs eternal.

The data helped to send yields lower and weaken the USD. The greenback fell the most vs the NZD (ahead of the rate decision), the GBP and the AUD. It was near unchange vs the CHF.

The UK employment data released before the US open, showed surprising strength. That helped to strengthen the GBP in trading today. The GBP was just behind the NZD (and just ahead of the AUD) as the strongest of the major currencies.

The NZD and the AUD benefitted from risk on flows. The RBNZ will meet and announce its rate decision in the new trading day. There is some debate on a cut or not with a Reuters survey pegging 5.4% (from the current 5.5%).

US yields were encouraged by the inflation data, ending the day lower with the shorter end down the most.:

- 2 year 3.935%, -8.1 basis points

- 5 year 3.673%, -7.6 basis points

- 10 year 3.848%, -6.3 basis points

- 30 year 41.60%, -3.8 basis points

The US stocks also cheered on the data with the Nasdaq rising over 400 points and closing above its 100-day MA for the 1st time since August 1.

The final numbers are showing:

- Dow Industrial Average rose 408.63 points or 1.04% at 39765.63.

- S&P index rose 90.06 points or 1.69% at 5434.44 .

- NASDAQ index rose 407.00 points or 2.43% at 17187.61

The INformation technology sector of the S&P surged by 3.0% while energy sector fell by -1.0% despite increased tension in the middle east.

Crude oil is trading down -$1.42 or -1.79% at $78.68 after testing its 100-day MA at session highs (see chart below). The low for the day also tested its 200-day MA. Buyers and seller are playing the 100/200 day MA range – at least for the day – with traders looking for the next break and mometum in the direction of the break.

This article was written by Greg Michalowski at www.forexlive.com.

Source link