- The Dow Industrial Average average can’t close at a record but closes just above 40,000

- The 2-10 year yield rises to -27.3 basis points. A close here will be highest since Jan 29

- Crude oil futures settle at $82.21

- Stock earnings for the quarter were kicked off. What’s on tap for next week?

- What happens after the first rate cut. Recession? Stocks move lower?

- A number of currency pairs stretched to key target levels including the NZDUSD. What next?

- Keep an eye on China’s Third Plenum meeting next week

- Japan’s Kanda: Won’t say whether intervention was conducted or not

- House Democratic leader Jeffries met with Biden yesterday. The read-out isn’t glowing

- UMich July consumer sentiment 66.0 vs 68.5 expected

- Kickstart the FX trading day for July 12 w/a technical look at the EURUSD, USDJPY & GBPUSD

- Canadian June home sales activity fell 9.4%

- Canada building permits for May -12.2% versus -5.9% expected

- US June PPI +2.6% vs +2.3% expected

- The GBP is the strongest and the JPY is the weakest as the NA session begins

- ForexLive European FX news wrap: Japanese yen settles down after big swings

- Japan top FX diplomat Kanda declines to comment on suspected intervention yesterday

- What has changed after the US CPI report

Yesterday, the US CPI was a friendly number as it came in lower than expectations. Today, the PPI data was the exact opposite. The headline numbers for the month were not only higher, but the prior months were revised higher as well.

The USD and yields move higher initially after the report, but the memory of the Chair comments this week where he talked about lower inflation and how it isn’t just about inflation but also the employment picture, along with the CPI data, sent yields and the dollar back to the downside.

Later at 10 AM the Michigan consumer confidence stayed near low levels (and below expectations) after the sharp, surprising drop from last month.

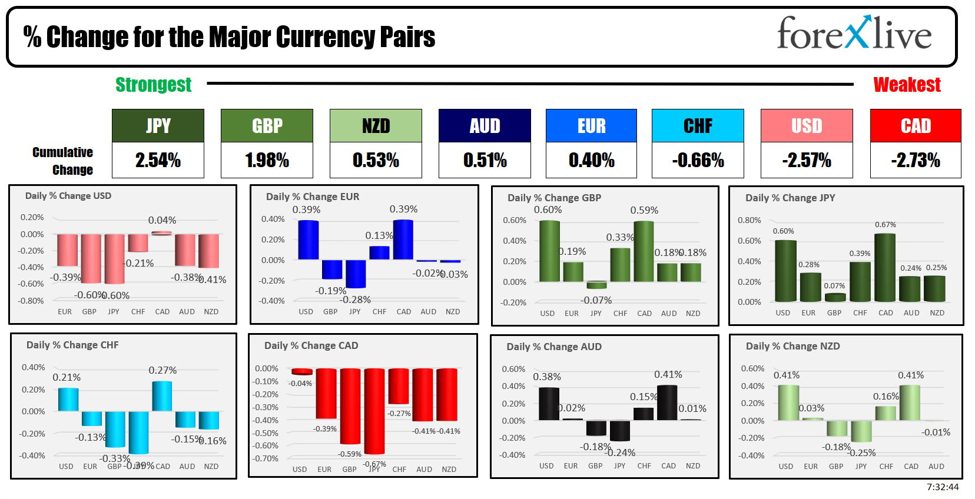

All of which helped to send the greenback lower vs all the major currencies today. At the end of the day, the USD was unchanged vs the CAD, but fell by -0.21% vs the CHF and had declines of -0.38% to -0.60% vs the other major indices (the USD fell -0.60% vs both the GBP and the JPY).

For the trading week the USD is ending mostly lower with only rising modesly vs the NZD. The greenbacks changes for the week vs the majors showed:

- EUR, -0.61%

- GBP, -1.35%

- JPY, -1.78%

- CHF, -0.08%

- CAD, -0.035%

- AUD, -0.53%

- NZD +0.43%

Looking at the US debt market today, the yields moved lower with the 2-year the biggest decliner. The yield spreads continue to chip away at the negative yield curve today:

- 2 year yield 4.457%, -4.9 basis points. For the week, the yield fell -15.4 basis points.

- 5 year yield 4.107%, -1.6 basis points. For the week, the yield fell -12.3 basis points.

- 10 year yield 4.186%, -0.6 basis points. For the week, the yield fell -9.5 basis points.

- 30 year yield 4.398%, -0.5 basis points. For the week, the yield fell -8.1 basis points

Looking at the spreads:

- 2-10 year spread, -27.1 basis points which is the least negative close since January. For the week, the spread rose 5.7 basis points.

- 2-30 year spread, -5.9 basis points which is the least negative close also since the end of January. The spread rose by 7 basis points this week.

In addition to lower CPI, the yields were helped by favourable 3 and 10 year note auctions (met by strong domestic demand). The 30 year bond was a different story, but 2 out of 3 outweighed the most difficult 30 year auction.

In other markets:

- Crude oil this week fell -1.14% to $82.21.

- Gold rose $19.54 or 0.82% to $2410.78

- Silver rose fell by -$0.47 or -1.38% to $30.77

- Bitcoin rose by $1778 to $57617

Next week,

Monday:

- Empire manufacturing

- Fed Chair Powell at 12 PM ET

Tuesday

- Canada CPI

- US Retail Sales

- NZD CPI at 6:45 PME ET

Wednesday:

- UK CPI

- Austalia employment data 9:30 PM ET

Thursday:

- UK employment

- ECB rate decision (no change expected)

- US weekly jobless claims

- Philly Fed Manufacturing

Friday

- UK Retail Sales

- Canada Retail Sales.

The major earnings releases for the week include:

Monday, July 15

- Goldman Sachs, BlackRock,

Tuesday, July 16

- Bank of America.United health group.Progressive.Morgan Stanley..Charles Schwab..PNC.Interactive Brokers. JB Hunt,

Wednesday, July 17

- Johnson & Johnson,United,Alcoa,Discover,Kinder Morgan

Thursday, July 18

- Taiwan Semi Conductor,Nokia,DR Horton,Netflix,Intuitive Surgical,PPG

Friday, July 19

- American Express,Halliburton,,Comerica,Travelers

When are the Magnificent 7 releasing its earnings this cycle?

- Alphabet, July 23

- Microsoft July 23

- Tesla July 23

- Amazon, July 25

- Meta Platforms, July 31

- Apple, August 1

- Nvidia, August 15

This article was written by Greg Michalowski at www.forexlive.com.

Source link