- NASDAQ index off to a strong start. Closes at a record level.

- Former Fed Gov. Clarida: Sees one Fed rate cut in December

- Democrats weighing early nomination for Pres. Biden

- ECB Pres. Lagarde: it will take time to be certain that inflation is on track

- Crude oil futures and settle at $83.38

- ECBs Wunsch: The markets pricing on rate cuts reasonable

- Goldman Sachs: Another sign that the dollar still stands above the ‘challengers’

- European indices closed the day with gains

- ECBs Sinkus: There is a possibility for 2 more cuts in 2024

- Atlanta Fed GDPNow growth estimate for Q2 1.7% versus 2.2% previously

- What’s driving the rout in bonds

- French antitrust regulators preparing to charge Nvidia

- US construction spending for May -0.1% versus 0.2% expected

- US May ISM manufacturing index 48.5 vs 49.1 expected

- US June S&P Global manufacturing PMI 51.6 vs 51.7 prelim

- Kickstart the FX trading day for July 1 w/a technical look at the EURUSD, USDJPY & GBPUSD

- Climbing Treasury yields underpin a strong bid in the US dollar

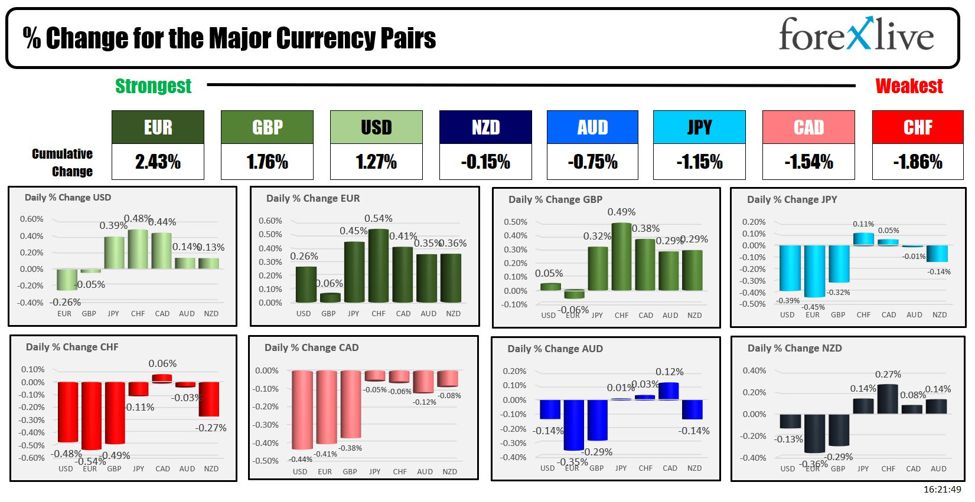

- The GBP is the strongest and the CHF is the weakest as the NA session begins

- Germany June CPI +2.2% vs +2.3% y/y expected

- ForexLive European FX news wrap: Euro up after first round of French elections

The USD moved higher today pushed by the rise in yields that saw the yield curve steepen once again.

Markets are reacting to a number of things in the debt market. Adam highlighted those ideas in his post HERE.

However, what seems to be the main driver is the markets perception that a Trump presidency will lead to a steeper yield curve on the back of more tax stimulus leading to more growth. That growth would the potential for more inflation. In addition, the enactment of more tariffs could also lead to higher inflation if a tariff trade war ensues.

The 2-10 year treasury spread has moved to -28.9 basis point which is up sharply from -50.9 basis points at the lows from last Tuesday of last week. The 2-30 year yield spread is up to -12.9 basis points after being as low as -37 basis points just last week. Although still negative, the yield curve is getting decisively less negative – especially since the debate on Thursday.

Today former president Trump was given relief from the Supreme Court after its ruling that the President should be give broad immunity. That will likely lead to the prosecution from January 6 being less likely and give the President and his staff more time to focus on the election. Coming off the Biden performance at last week’s debate and the Democratic Party’s seeming decision to keep Biden as their candidate, it has the market feeling that Trump – and the Republicans – may sweep to victory in November.

Looking at the yield curve changes today:

- 2 year yield 4.759%, +4.0 basis points.

- 5-year yield 4.429%, +9.9 basis points.

- 10 year yield 4.469% +12.6 basis points

- 30-year yield 4.631%, +12.9 basis points

Looking at the changes in the foreign exchange, the USD was mostly higher, but was still behind the EUR and the GBP for strongest honors to start the trading week. The USD was the strongest vs the CHF, CAD and JPY.

For the USDJPY, it moved to another new high for the year and to the highest level going back to January 1987. The high price today reached 161.72. The high price from 1990 reached 160.40. That is now a risk-defining level for buyers. As long as the price can remain above that 1990 high level, the buyers remain in full control and the door remains open for further gains in the USDJPY pair.

Fundamentally today, despite the rise in yields, the data was weaker with construction spending coming in at -0.1% versus +0.2% expected. The ISM manufacturing index was also lower-than-expected of 48.5 versus 49.1 expected. Moreover the prices paid and employment components were weaker:

- Prices paid 52.1 versus 57.0 prior

- Employment fell below the 50.0 expansion level to 49.3 versus 51.1 last month

The US jobs report will be released on Friday, a day after the July 4th holiday and the UK election.

Despite the rising yields, the NASDAQ index did trade and close at a new record high today. The S&P and Dow Industrial Average average also rose modestly. The small-cap Russell 2000 did not fare as well as it reacted to the higher rate and the steeper yield curve.

The final numbers to start the 2H of the year showed:

- Dow Industrial Average average, +0.13%.

- S&P index +0.27%.

- NASDAQ index +0.83%.

- Russell 2000-0.86%

In other markets:

- Crude oil rose 2.33%

- Gold rose 0.22%

- Silver rose 1.06%

- Bitcoin was up 0.86% from Sunday’s levels

This article was written by Greg Michalowski at www.forexlive.com.

Source link