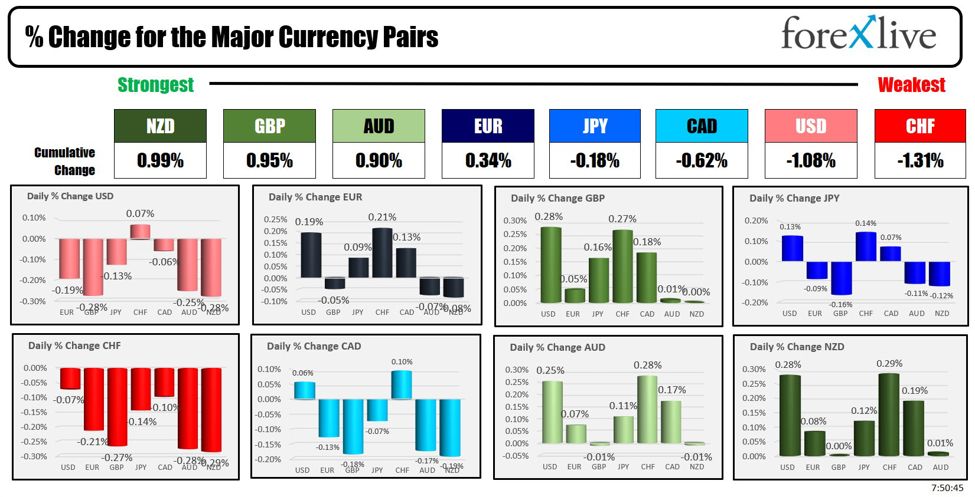

TGIF. As the North American session begins, the NZD is the strongest and the CHF is the weakest.

China’s economy grew at a slower pace in the third quarter, with GDP expanding by 4.6% year-on-year, down from 4.7% in the previous quarter and marking the lowest reading in 18 months. This slowdown highlights the challenges facing Beijing, as the growth rate remains below the government’s full-year target of 5%.

China has been rolling out various stimulus measures aimed at addressing persistent deflation, weak private consumption, and a prolonged property market downturn.

In other economic news from Japan and China:

- Japan National Core CPI y/y: 2.4% (forecast: 2.3%, previous: 2.8%)

- China New Home Prices m/m: -0.71% (previous: -0.73%)

- China Industrial Production y/y: 5.4% (forecast: 4.6%, previous: 4.5%). Better than expected.

- China Retail Sales y/y: 3.2% (forecast: 2.5%, previous: 2.1%). Better than expected

- China Unemployment Rate: 5.1% (forecast: 5.3%, previous: 5.3%). Stronger than expected

Following the release of the data, shares fell but later recovered after the People’s Bank of China introduced new lending programs to support share buybacks and equity purchases. The Shanghai composite index rose 2.91%, the CSI300 rose 3.62% and Hong Kongs Hang Seng surged 3.61%.

In central bank news, Bloomberg reported that the Bank of Japan is increasingly aware of the complexities surrounding the current economic outlook and sees little need for an immediate rate hike. While they are cautious about predicting future hikes, they are also mindful of achieving their 2% inflation target. However, they remain uncertain about the impact of global economic conditions, particularly those in the U.S., on Japan’s financial markets and overall economic stability. While the BoJ acknowledges ongoing financial market volatility and is concerned about inflation trends, the central bank will monitor conditions closely before making any further moves, waiting to assess broader economic signals and foreign exchange market pressure before acting.

Also a day after the ECB cut rates by 25 basis points, and ECBs Lagarde gave a sanguine view of the economy, some ECB governors wanted to drop the pledge to keep policy tight as inflation could be lower than anticipated just a few weeks ago.

Stocks are mixed in premarket trading helped by earnings. The Dow is lower, but the S&P and the Nasdaq indices are higher.

In earnings news after the close yesterday, Netflix and Intuitive Surgical reporting better than expected earnings and their shares are sharply higher. However, today, P&G and Amex earnings released today were mixed (helping to weaken the Dow):

Netflix Inc (NFLX) Q3 2024

-

EPS: 5.40 (exp. 5.12) BEAT

-

Revenue: 9.82bln (exp. 9.76bln) BEAT

Q4 Guidance:

- Revenue: $10.13 billion (BEAT expectations of $10.05 billion)

- EPS: $4.23 (BEAT expectations of $3.90)

- Operating margin: 22% (MET expectations of 21.2%)

FY25 Guidance:

- Revenue: $43-44 billion (MET expectations of $43.4 billion)

- Operating margin: 28% (MET expectations of 27.9%)

Shares of Netflix are trading up $43.40 or 6.31% at $731.10

Intuitive Surgical Inc (ISRG) Q3 2024

-

EPS: 1.84 (exp. 1.64) BEAT

-

Revenue: 2.04bln (exp. 2.01bln) BEAT

Shares of Intuitive Surgical are trading up $30.27 or 6.39% at $504.00

In earnings released this morning:

American Express Co (AXP) Q3 2024:

- EPS: $3.49 (expected $3.28) → BEAT

- Revenue: $16.64 billion (expected $16.67 billion) → MISS

American Express shares are trading down -1.15%

Procter & Gamble Co (PG) Q1 2025:

- EPS: $1.93 (expected $1.90) → BEAT

- Revenue: $21.7 billion (expected $21.96 billion) → MISS

P&G shares are higher by 0.51%

IN the US and Canada today, the economic calendar is fairly light:

- 8:30 AM ET Building Permits: Forecast 1.46M versus 1.48 million last month

- 8:30 AM ET Housing Starts: Forecast 1.35M versus previous 1.356M

- 12:10 PM ET FOMC Member Waller Speaks:

- 4 PM ET Federal Budget Balance: Forecast less $61.00 billion versus $-380 billion last month

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down -$0.86 or -1.25% at $69.75. At this time yesterday, the price was at $70.39. Hamas leader Yahya Sinwar was killed in Gaza. Sinwar was an architect of the concert attack on October 7, 2023

- Gold is trading to another record high and is up $17.41 or 0.65% at $2709.10. At this time yesterday, the price was $2680.93

- Silver is trading up $0.40 or 1.31% at $32.07. At this time yesterday, the price is at $31.75

- Bitcoin is trading higher at $67,803. At this time yesterday, the price was at $66,909

- Ethereum is trading at $2624.90. At this time yesterday, the price was at $2600.90

In the premarket, the snapshot of the major indices mixed with the Dow suffereing from P&G and Amex. The Nasdaq is being supported by Netflix after their earnings and a rebound in Chinese stocks after their actions today:

- Dow Industrial Average futures are implying a decline of -57 points. Yesterday, the index rose 161.35 or 0.37% at 43239.05

- S&P futures are implying a gain of 12.50 points points. Yesterday, the index fell -1.00 points ori -0.02% at 5841.47

- Nasdaq futures are implying a gain of 114 points. Yesterday, the index rose 6.53 points or 0.04% at 18373.61

Yesterday, the small-cap Russell 2000 fell -5.82 points or -0.25% at 2280.85

European stock indices are trading mixed:

- German DAX, +0.33%

- France CAC, +0.68%

- UK FTSE 100, -0.25%

- Spain’s Ibex, -0.03%

- Italy’s FTSE MIB, +0.33% (delayed by 10 minutes)

Shares in Asian Pacific session shares were mostly lower:

- Japan’s Nikkei 225, +0.18%

- China’s Shanghai Composite Index, +2.91%

- Hong Kong’s Hang Seng index, +3.61%

- Australia S&P/ASX index, -0.87%

Looking at the US debt market, yields are trading modestly higher

- 2-year yield 3.980%, -0.7 basis points. At this time yesterday, the yield was at 3.946%

- 5-year yield 3.911%, +0.4 basis points. At this time yesterday, the yield was at 3.856%

- 10-year yield 4.108%, +1.2 basis points. At this time yesterday, the yield was at 4.031%

- 30-year yield open 4.410%, +1.7 basis points. At this time yesterday, the yield was at 4.317%

Looking at the treasury yield curve close steeper on Friday. At the close

- The 2-10 year spread is at +12.8 basis points. At this time Friday morning, the yield spread was +8.7 basis points.

- The 2-30 year spread is at +43.2 basis points. At this time Friday morning, the yield spread was +37.2 basis points.

The benchmark 10-year yields are mixed/mostly lower:

This article was written by Greg Michalowski at www.forexlive.com.

Source link